2026-04-10")

")

Hudson Pacific Properties, Inc. (NYSE:HPP) is in focus today as we dial on the real estate investment trust’s (“REIT’s”) prospects after its more than 40% year-over-year drawdown.

As an office REIT, Hudson Pacific has been in the firing line due to the “work from home” phenomenon. Moreover, the company’s other segment, which invests in production studios and sound stages, possesses numerous talking points as to its feasibility, but its utility as a diversification tool remains in question.

Without further ado, let’s move ahead to the core of today’s analysis.

Starting With Its Valuation and Dividend Metrics

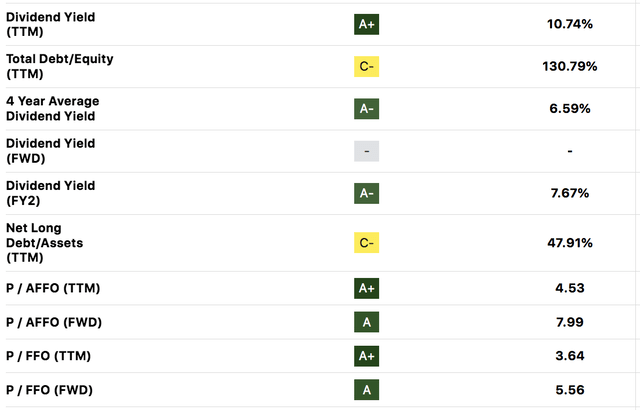

As illustrated in the diagram at the bottom of the section, Hudson Properties’ valuation and dividend metrics are exceptionally well placed after the REIT’s latest drawdown.

To run through a few of them, the REIT’s price-to-funds from operations is at a 64.55% sector discount, while its price-to-rent ratio is at an 81.51% sector discount. Moreover, Hudson Properties’ dividend yield of 10.74% is arguably ranked among the best in class.

However, looking at the aforementioned metrics in isolation is extremely dangerous, as they do not reflect the prospects embedded within the REIT. In our view, Hudson Properties is stuck with significant fundamental challenges that could lead many investors into a value trap.

Let’s move on to the next section to diverge from an isolated analysis of Hudson Properties’ key metrics.

Seeking Alpha

Fundamental Analysis

Portfolio

Office

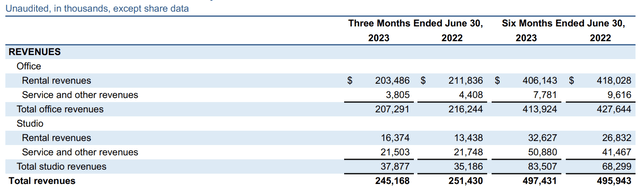

Hudson Pacific Properties derives about 84.5% of its revenues from its office segment, which primarily generates its inflows from lease terms.

Hudson Pacific

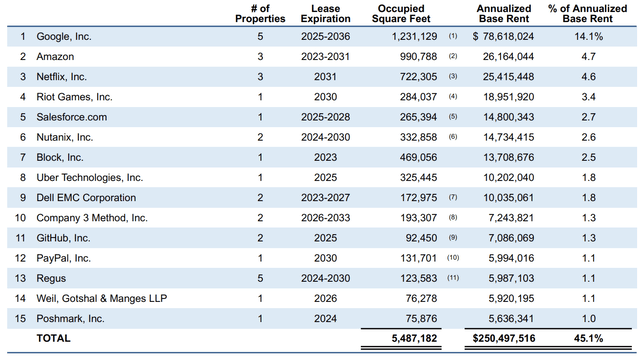

On the plus side, Hudson Pacific’s portfolio has low concentration risk as its top 15 tenants comprise only 45.1% of its portfolio’s base rent. On top of that, high-caliber tenants such as Google (GOOG), Amazon (AMZN), Netflix (NFLX), and Salesforce (CRM) rent from Hudson Pacific on long-dated lease terms.

Top 15 Office Tenants (Hudson Pacific)

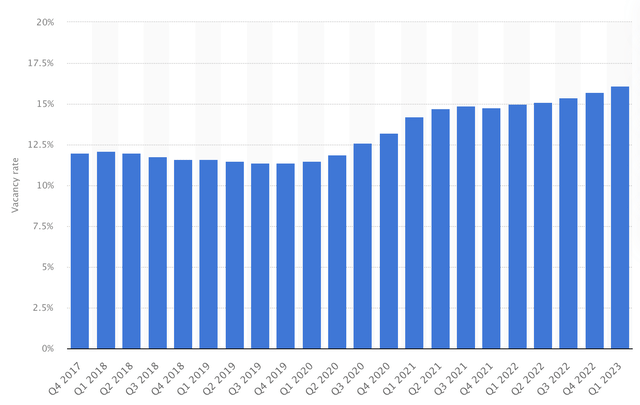

Nevertheless, general office occupancy in the U.S. is dropping steeply despite the rise of concepts such as communal office space and virtual office addresses. This raises the possibility that property values and rental escalations will grow slower than before the pandemic (or even drop).

Office vacancies continue to mount (Statista)

Hudson Pacific’s office portfolio is running on 85.2% occupancy, which illustrates the regime change experienced in office lettings.

We sincerely doubt that these numbers will pick up in the near future. Although employee headcount might eventually rise at some of the REIT’s tenants, we believe that work-from-home and other factors, such as company employee offshoring, will upend long-term valuations, leading to forced-upon dispositions.

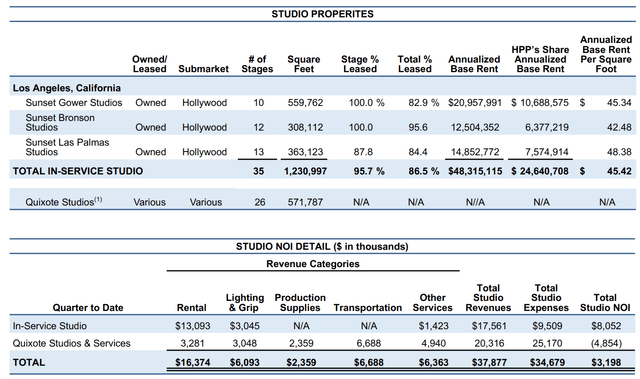

Studios

To our knowledge, Hudson Pacific’s pipeline of office sales is currently at $100 million, and the company recently stated that more will follow as it is actively working on dispositions.

Logically, one would say that the proceeds from dispositions will be utilized for studio acquisitions. Since the pandemic, Hudson Pacific has struggled to commit capital to new developments and recently affirmed its stance on stabilizing the business before engaging in capital commitments.

Nevertheless, an influx of capital could lead to acquisitions, which might complement its nearly finished Sunset Glenoaks Studio in Los Angeles in the coming years.

Studios (Hudson Pacific)

A pivot into a more studio-centric business model essentially means that Hudson Pacific will likely provide investors with diversified returns, concurrently luring in a new investor base; however, challenges exist.

First, reallocating capital will be cumbersome, as the studios provide a lower base rent per square meter than Hudson Pacific’s offices. Moreover, the acquired properties must be redeveloped into studios, potentially leading to delay costs on invested capital.

Another consideration is the thin net operating income margin of 19.5% (Computed as NOI/Total Rental). I could not find the studio asset base value. As such, I wasn’t able to compute the capitalization rate. However, I do not expect the studio business to deliver stellar going-in cap rates, given its slightly underwhelming total leased percentage and thin net operating income margin.

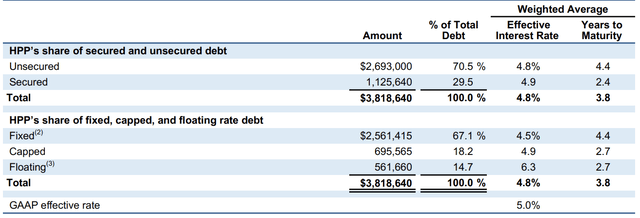

Capital Structure

Hudson Pacific’s weighted average cost of debt is 5%, with most of its obligations maturing by year-end 2026.

Hudson Pacific

Although it can refinance at lower rates when interest rates eventually curtail, and even though it hedges interest rate risk with derivatives, Hudson Pacific’s capital structure is faced with numerous headwinds.

Firstly, Fitch affirmed its BBB- rating on the REIT’s debt earlier this year. Thus, even if interest rates drop, the fund’s credit risk remains an issue, which may result in higher-than-usual financing costs. Moreover, headwinds from sluggish office occupancy have added significant pressure, which is reflected by Hudson Pacific’s cost of equity.

Valuation

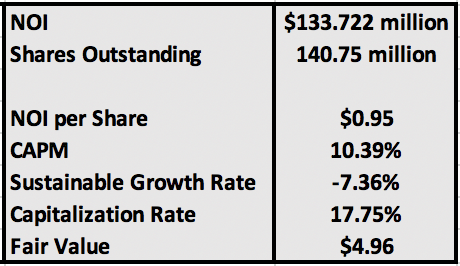

Gordon’s Growth Model – Model Output

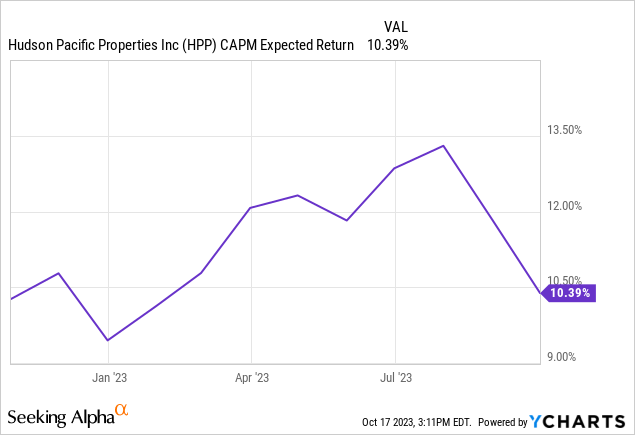

I rebased the earlier-mentioned valuation multiples by using an adjusted Gordon’s Growth Model to account for the REIT’s sustainable growth rate and equity risk premium.

The result implies that Hudson Properties is overvalued, with its fair value of $4.96 sitting below its market value of around $5.80 (at the time of writing this article).

Author’s Work

Although it is not a guaranteed method of ascertaining an asset’s fair value, the GGM suggests that the REIT’s price multiples might be slightly misleading.

Model Inputs

Here are the inputs I used for the model.

- I used the REIT’s financial statements to find the Net Operating Income while relying on Seeking Alpha’s data for the shares outstanding.

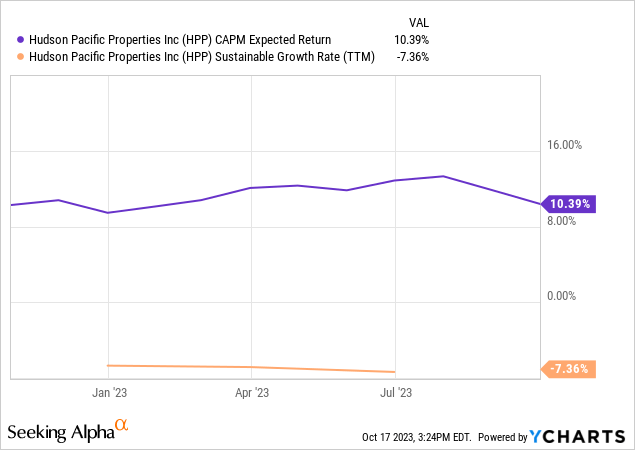

- The capitalization rate was determined by summing the REIT’s CAPM and sustainable growth rate.

Final Word

Our analysis shows that investors would be wise to critique Hudson Pacific’s alluring price multiples and dividend yield before investing in the REIT.

According to our valuation model and fundamental analysis, Hudson Pacific Properties, Inc. stock is slightly overvalued, stemming from broken growth. Much of the REIT’s growth concerns derive from ongoing regime changes in the office property arena. Moreover, Hudson Pacific’s studio portfolio may take time before reaching scale, which is pegging back the REIT’s valuation.

Despite our negative stance, we believe this REIT is best left alone instead of being sold short. Therefore, we assign a hold rating.

Read the full article here

2026-04-10")

")

(NASDAQ:MU)")

")