Q2 2026 Earnings Call Transcript")

")

The Walt Disney Company (NYSE:DIS) investors have received somewhat of a respite in October, even as the S&P 500 (SPX) (SPY) continues to struggle for traction. Accordingly, since my previous update in August, DIS has slightly outperformed SPX. While the extent of the outperformance isn’t significant, DIS’s price action has shown signs of life in October, as it recovered all its losses from the September hammering. As such, I believe it corroborates my thesis that significant pessimism has been reflected in DIS’s valuation.

Disney updated investors with recast financials yesterday (October 18) through a regulatory filing, providing critical insights into the health of its business segments, particularly its sports business. As such, the timely disclosures have arrived at an opportune time for potential ESPN partners to assess the growth drivers of its sports business as Disney looks to monetize its sports programming further.

As anticipated, ESPN remains a critical profitability driver for the company as it moves toward a streaming-focused future for its content and networks business. Accordingly, Disney’s sports segment posted revenue of $13.2B for the nine months ended 1 July 2023. It recorded an operating profit of $1.48B, resulting in an operating margin of 11.2%. As such, it’s significantly more profitable than its entertainment business segment. The entertainment segment posted an operating profit of $1.21B over the same period for an operating margin of 3.9%. However, investors should expect a much-improved performance for Disney’s entertainment business, as its direct-to-consumer or DTC business tracks toward profitability by the end of FY24.

Bloomberg Intelligence suggested the solid profitability of Disney’s sports business could make it “an attractive option for outside investors.” As such, it estimated a valuation of up to $22B for its sports business. Disney could undoubtedly do with some help as it looks to potentially integrate the one-third stake in Hulu that it doesn’t already own (currently owned by Comcast (CMCSA)). Based on the minimum valuation of $27.5B as part of the 2019 agreement, Disney is expected to pay Comcast at least $9.17B to secure full ownership.

Moreover, with Disney announcing its intention to invest $60B in its theme parks and related attractions over the next decade, the company must assure investors about its ability to sustain its free cash flow or FCF. The market has reacted positively to Disney’s recent price increase in its theme parks, demonstrating its pricing power. Notwithstanding the market optimism, it remains to be seen whether it could price out American families, leading to a loss of goodwill and consumer spending impact. However, given DIS’s battering over the past year, investors seemed confident that consumers might find it hard to obtain world-class substitutes from Disney’s offerings over time.

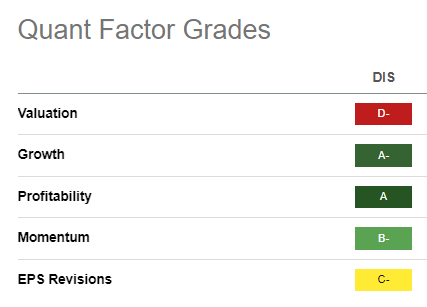

DIS Quant Grades (Seeking Alpha)

DIS is still priced for growth (“A” growth grade). As seen above, investors still expect robust execution from management to justify its “D-” valuation grade. As such, I believe investors should remain focused on the company’s ability to move with more urgency toward profitability in its DTC segment while attracting external partners in its sports business.

Moreover, DIS’s momentum has shown improvement, as indicated by its “B-” valuation grade. Despite that, I must highlight that DIS’s price action has seen substantial damage. As a result, investors must be patient for buyers to return with more aggression. Notwithstanding my near-term caution, high-conviction investors should still find Disney’s wide-moat business model attractive, underscored by its best-in-class “A” profitability grade.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here

Q2 2026 Earnings Call Transcript")

")

(NASDAQ:MU)")

")