Q4 2025 Earnings Call Transcript")

")

Intel (NASDAQ:INTC) is expected to report third quarter results after the close of trading on Thursday, Oct. 26. Analysts forecast it to be a horrible quarter for the company, with earnings expected to drop by 64% while revenue drops by almost 12%.

Still, the stock has had a big move higher since February in hopes that the business will turn around in the fourth quarter. However, more recently, shares have come under pressure as Nvidia (NVDA) announced its plans to make ARM-based PC CPUs.

The recent move lower in the stock has an options trader betting the declines aren’t over, and the stock has more to fall. Based on technical analysis, it could be as much as 8% from its current price of around $33.50.

Weak Result Expected

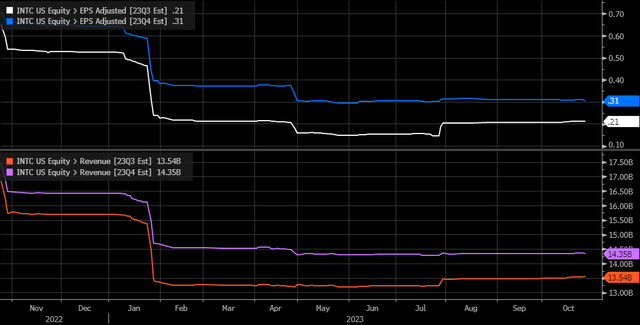

Earnings in the third quarter are expected to be pretty bad, at just $0.21 per share, down from $0.59 last year, while revenue is expected to fall to $13.5 billion, down from $15.3 billion. Additionally, adjusted gross margins are forecast to fall to 43.1% from 45.9%.

Growth is expected to improve next quarter, and that’s why the stock has rallied as investors hope that the worst is the company. Analysts forecast that Intel will earn $0.31 per share, up from $0.10 in the fourth quarter of 2022, while revenue jumps to $14.3 billion from $14.0 billion, as adjusted gross margin expands to 44.2%.

Meanwhile, the data center and AI are expected to see revenue slip 7.4% to $3.941 billion, while client computing is forecast to drop by 9.2% to $7.39 billion. Given all the hype around AI and data center growth, a miss in that one line item could send share lower by itself.

Bloomberg

Hopes For Better Times To Come

The hope of stronger growth has seen the stock rise mainly due to P/E multiple expansion, with the ratio rising to almost 21. That’s well above the historical range since 2010 of between 10 to 14. If the stock were traded back to 14 times 2024 earnings estimates, it would be worth just $23.80.

Bloomberg

This P/E expansion is due to the very large earnings growth that’s expected, going from $0.55 this year to $1.70 in 2024, then $2.15 in 2025. The growth in earnings is expected to be fueled by revenue, which is forecast to rise to $58.7 billion in 2024 from $52.52 billion in 2023 and to $63.5 billion in 2025. But there’s also expected to be a lot of gross margin expansion, rising to 46.2% in 2024 from 41.6% in 2023 and then 51.1% in 2025. Even with all the margin expansion, off the lows, margins will remain well below the levels witnessed between 2010 and 2019 when it was at 60% or higher.

Bloomberg

Options Traders Not Optimistic

Still, options traders do not appear to be believers, betting that Intel’s stock is likely to see lower prices in the weeks ahead. Whether it’s because they are betting that other companies will start taking market share from Intel or analysts’ forecasts for future earnings growth and margin expansion are too rosy, given the broader equity market infatuation with AI and data center growth, options traders could simply be betting on a line item miss.

Whatever the case, the options bets on Intel are turning bearish. On October 24, the open interest for the November 17 $35 puts rose by almost 11,700 contracts. The data from Trade Alert shows that 9,000 put contracts traded on the ASK for $1.75 per contract. This would imply that the trader thinks the value of the stock will be $33.25 or less if holding the options until the expiration date.

But there’s more because on October 24, the open interest for January 19, 2024, $40 calls increased by almost 20,000 contracts. The data here shows that these calls were traded on the BID for $0.93 per contract, suggesting that these calls were sold. This is a bet that Intel stays below $40 by the middle of January.

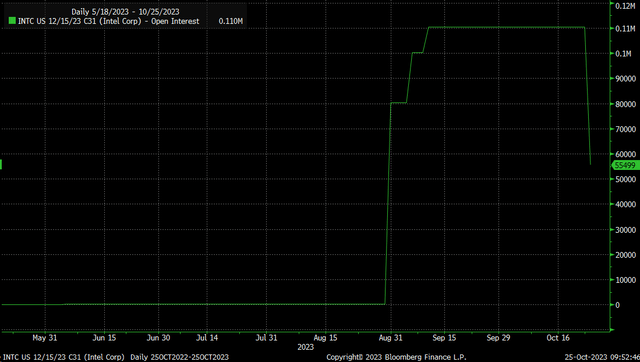

Also, worth noting is that on October 25, the open interest for December 15, 2023, $31 calls fell by almost 55,000 contracts. The data shows the calls were sold on the bid for $4.45 per contract. There had been a large buyer of these calls on August 31, 2023, with a block of 80,000 contracts trading for $5.45 per contract. This would suggest that the trade sees no upside in Intel at current levels and is selling his calls at a loss.

Bloomberg

Momentum Turns Bearish

The technical chart for Intel does not look strong and shows that momentum has turned bearish on the relative strength index. Additionally, the stock is trading at the lower bound of a triangle pattern, and a break of the lower bound around $33.50 could result in the stock falling all the way back to $30.90, a drop of around 8%. Meanwhile, a move higher in the stock is likely limited to the upper bound of the triangle around $35.75.

TradingView

Intel’s shares have certainly seen a big move higher, and if the company can deliver better-than-expected growth and provide guidance better than expected, then shares could see a decent rebound. However, a miss on cloud and AI revenue could mean the shares fall sharply, especially given how much the PE ratio has expanded in recent months because this stock is not cheap, even when factoring in all future growth estimates.

Read the full article here

Q4 2025 Earnings Call Transcript")

")

(NASDAQ:MU)")

")