(NASDAQ:MU)")

")

")

Palo Alto Networks (NASDAQ:PANW) is proving itself to be the perfect package. During a period in which the tough macro environment has disrupted growth engines across the tech sector, PANW has benefitted both from cybersecurity tailwinds as well as from having a wide product portfolio. Customers are increasingly looking to consolidate their cybersecurity products, making PANW a potential beneficiary of the consolidation trend. PANW maintains a net cash balance sheet and has completed a full year of GAAP profitability. Management has guided for several more years of aggressive top-line growth to go alongside long term margin expansion. I reiterate my buy rating for this cybersecurity winner.

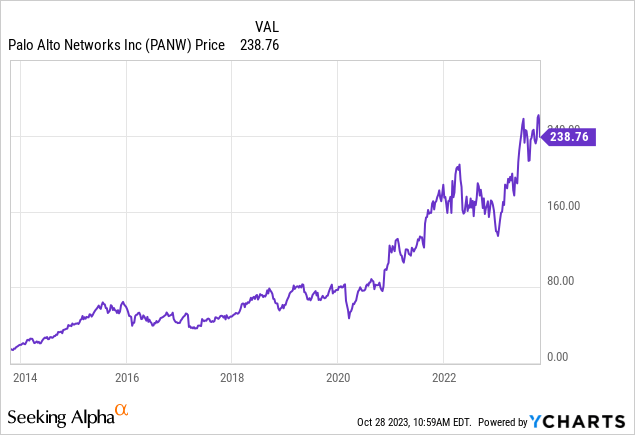

PANW Stock Price

There aren’t many tech stocks that still trade within inches of all time highs, putting PANW in rarified territory. The company has delivered strongly in spite of rising interest rates and fears of a recession, and I expect this strong performance to culminate in long term multiple expansion.

I last covered PANW in May where I rated the stock a buy on its strong balance between growth and profitability. The stock has jumped 20% since then, but I remain bullish given the reasonable valuation and margin expansion ahead.

PANW Stock Key Metrics

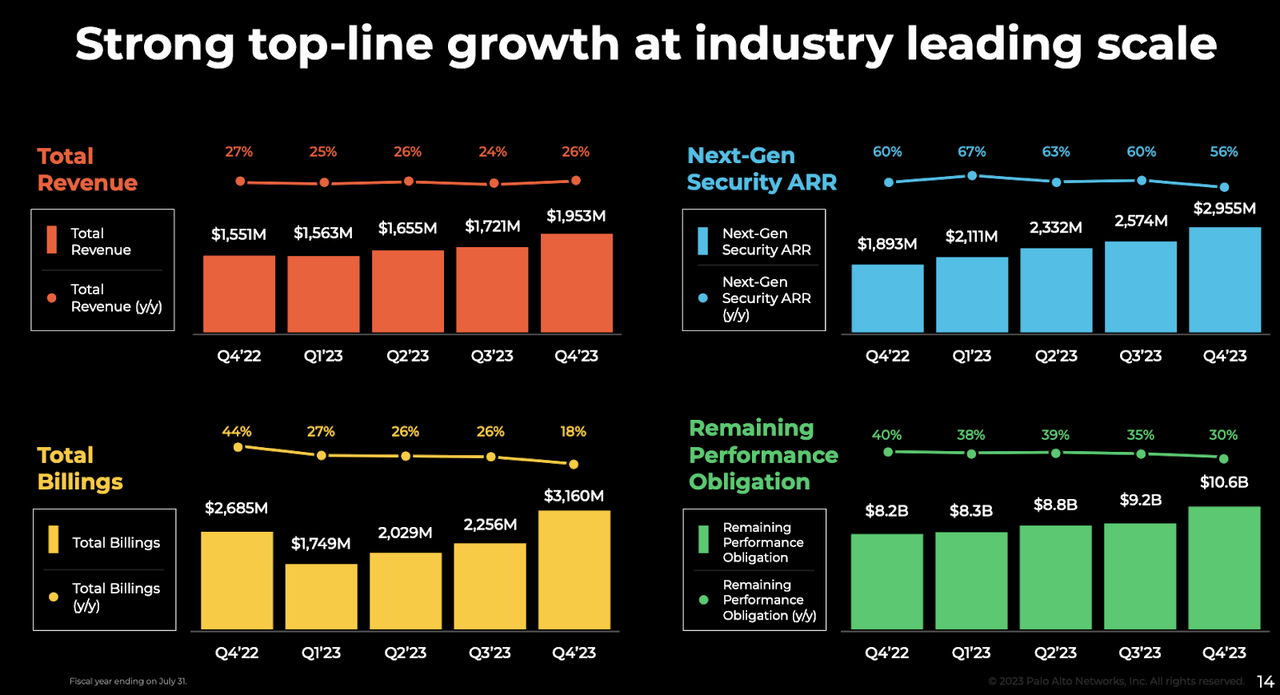

In its most recent quarter, PANW delivered impressive growth, with revenue growth remaining resilient at 26% YoY. That growth was powered by its next-gen security portfolio, with next-gen security ARR growing 56%. Remaining performance obligations (‘RPOs’) grew by 30% YoY. Peers have often seen customers seek shorter deal terms, making that RPO growth rate very impressive.

FY23 Q4 Presentation

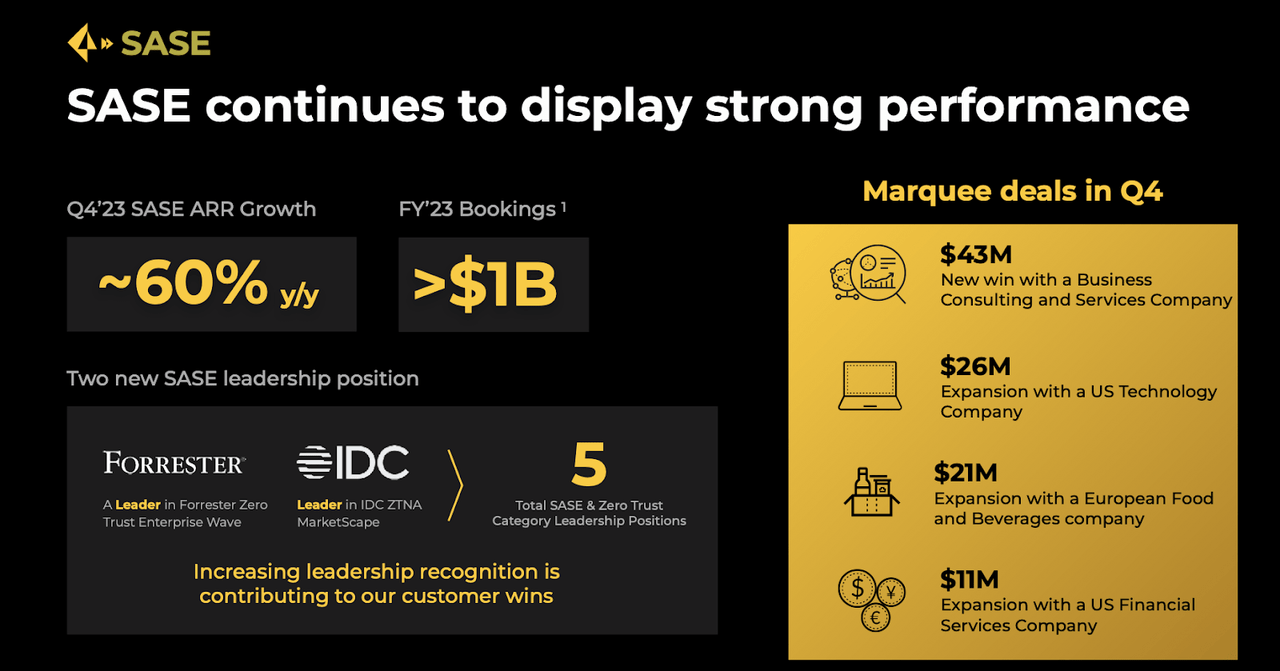

PANW highlighted strength seen in its secure access service edge (‘SASE’) offerings, with SASE ARR growing 60% YoY in the quarter.

FY23 Q4 Presentation

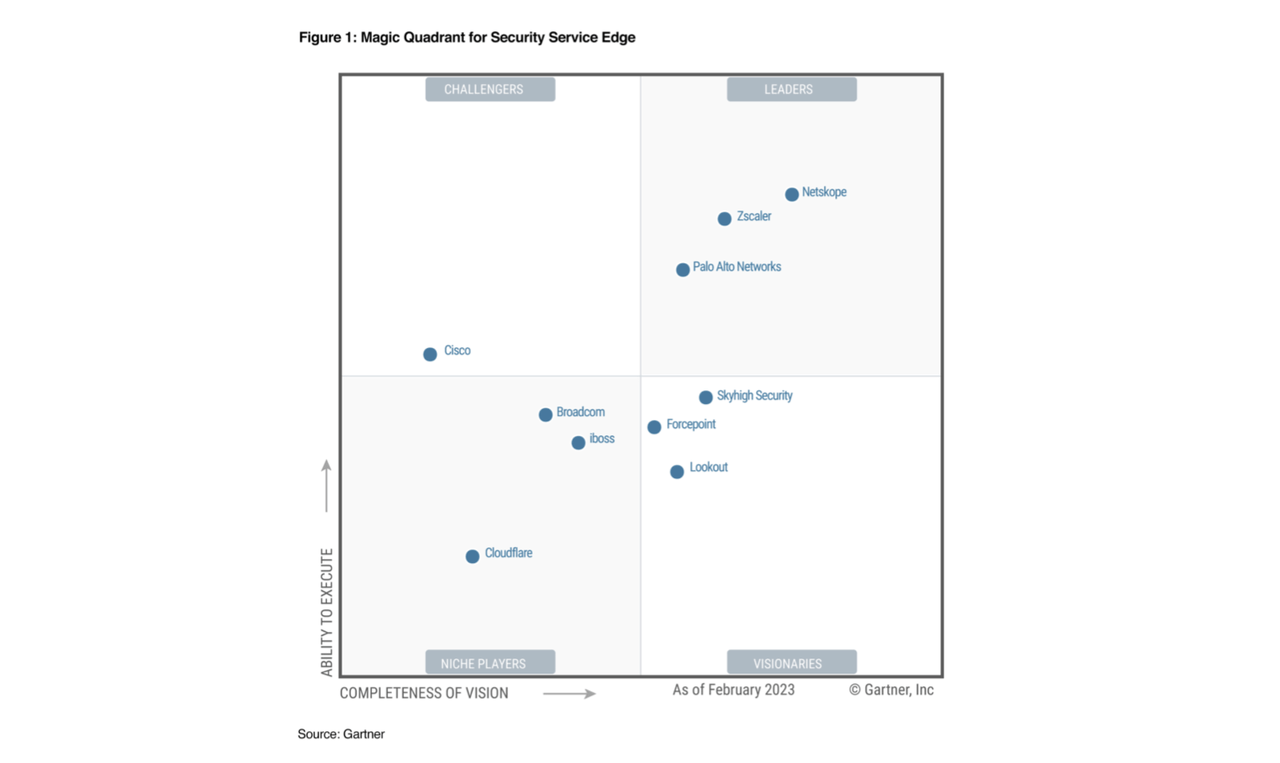

Tech investors might recognize that category – Zscaler (ZS) is often considered a top competitor in this space.

Gartner

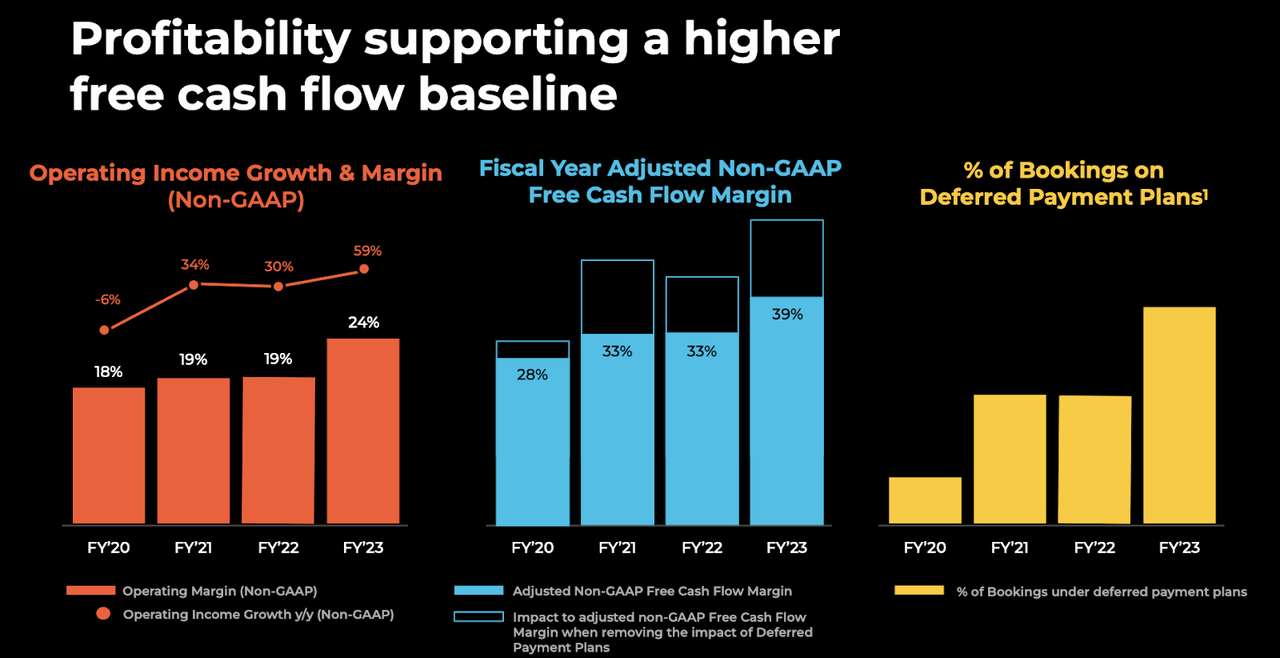

PANW is a favorite among growth investors not only due to its secular revenue growth but also its strong profitability. PANW delivered 600 bps of non-GAAP operating margin and free cash flow margin expansion in the past fiscal year, and this came in spite of more customers seeking deferred payment plans (in response to the tough macro environment). I note that PANW delivered $227.7 million in GAAP net income in the quarter, representing its 5th consecutive quarter of GAAP profitability.

FY23 Q4 Presentation

PANW ended the quarter with $5.4 billion of cash versus $2 billion of debt. Together with the strong free cash flow generation, the company maintains a pristine balance sheet.

Looking ahead, management has guided for the first quarter to see up to 18% YoY revenue growth to $1.85 billion and 19% YoY billings growth to $2.08 billion. Earnings are expected to grow 41% YoY to $1.17 per share. Consensus estimates see PANW coming just short of these targets at $1.84 billion in revenue and $1.16 in non-GAAP EPS. Given the strong performance in billings and RPOs, I find it likely that PANW outperforms these expectations.

Seeking Alpha

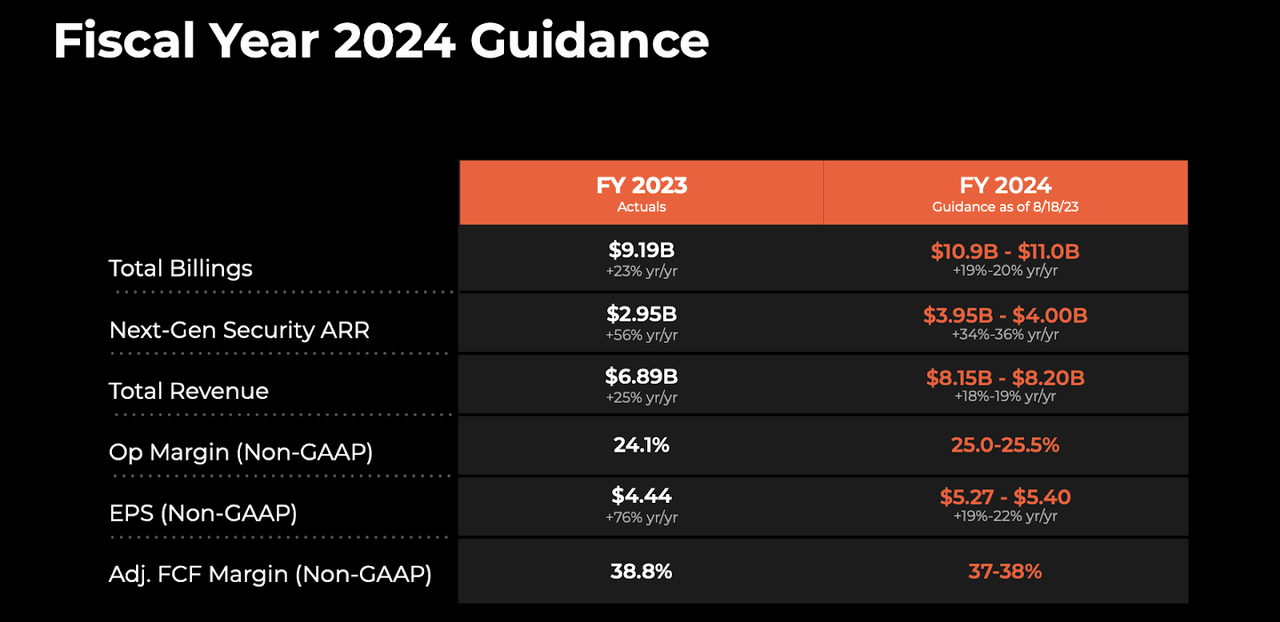

For the full year, management expects revenues to grow up to 19% YoY to $8.2 billion and billings to grow up to 20% YoY to $11 billion. Non-GAAP operating margin is expected to expand further to up to 25.5%.

FY23 Q4 Presentation

On the conference call, management answered questions from analysts regarding their strength relative to peers. PANW credited their strong fundamental performance as being due to offering a wide product portfolio, stating that customers are seeking to consolidate point products as it does not make sense (in their view) to have cybersecurity products that do not work together.

Is PANW Stock A Buy, Sell, or Hold?

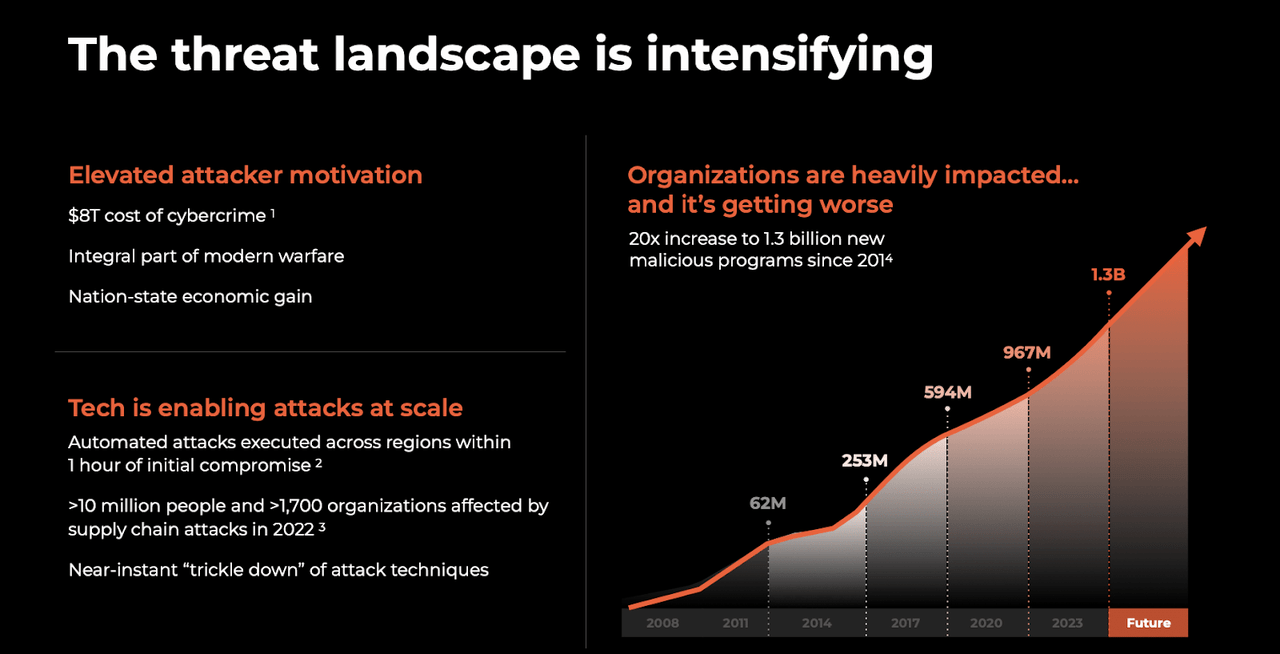

Cybersecurity is one of the few subsectors in tech and the overall market that has tailwinds for as long as the eye can see. The digitization of the world has only made cyberattacks more prevalent.

FY23 Q4 Presentation

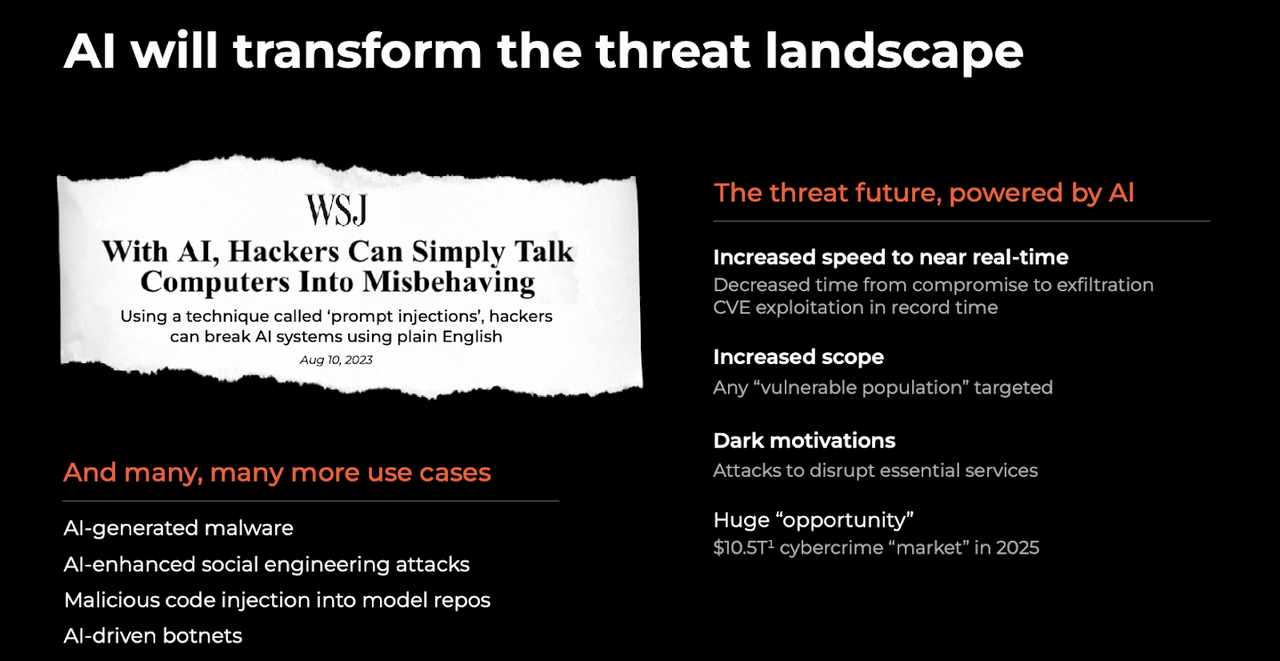

Generative AI may further increase the importance of cybersecurity due to having the potential to increase the complexity of cyberattacks.

FY23 Q4 Presentation

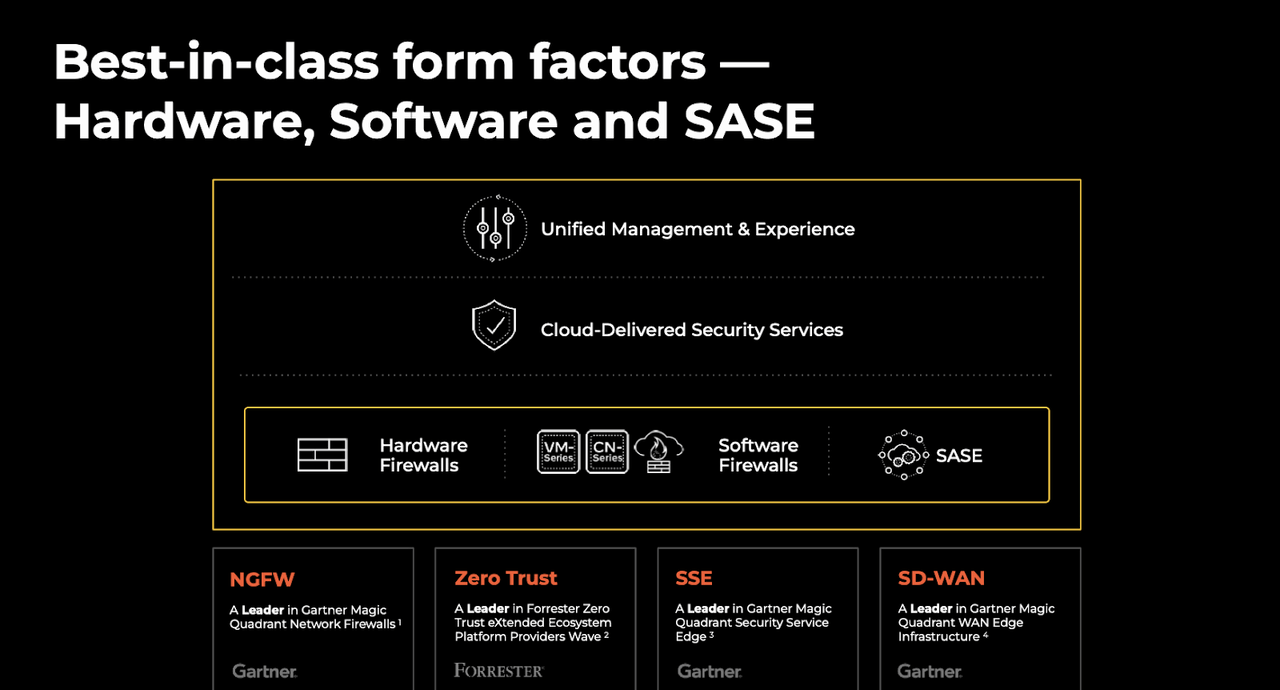

That all makes PANW “in the right place at the right time.” PANW offers a deep cybersecurity product offering highlighted by firewall protection.

FY23 Q4 Presentation

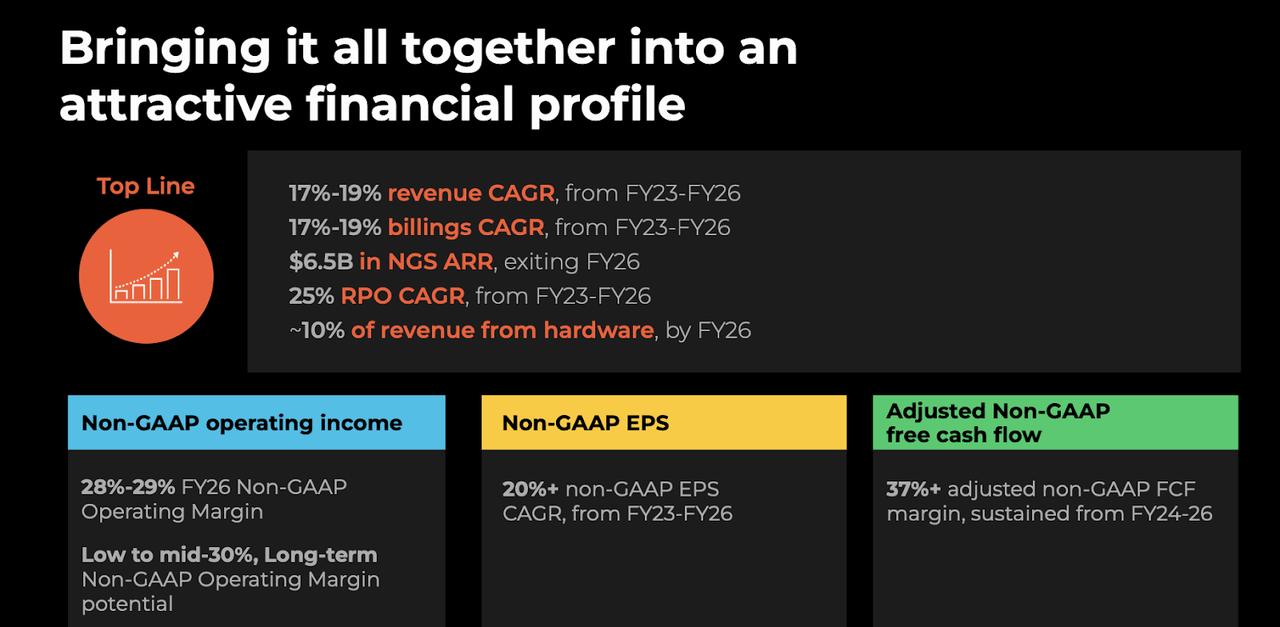

Management has issued medium-term guidance that calls for up to 19% annual revenue growth through 2026, with non-GAAP operating margins expanding to 29% as well.

FY23 Q4 Presentation

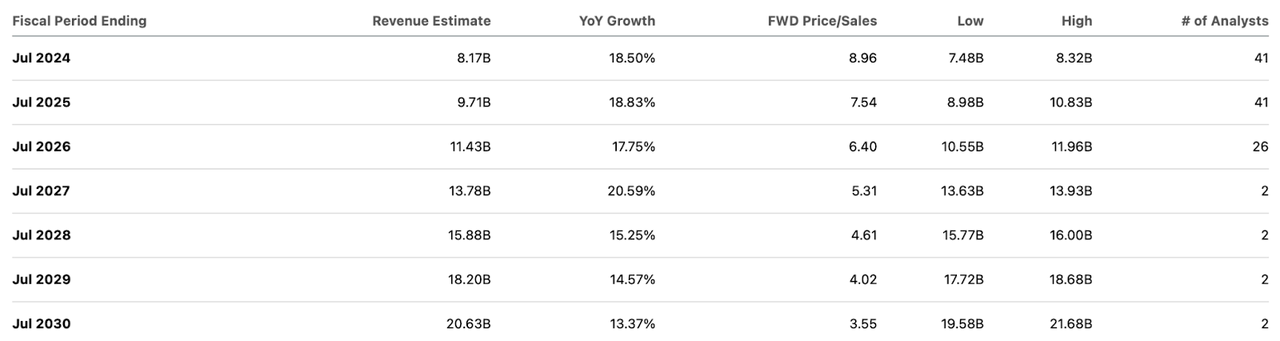

Consensus estimates have PANW growing revenues at around 18% through 2026, in-line with management guidance.

Seeking Alpha

Management also gave guidance for “low to mid-30%” long-term non-GAAP operating margins. Consensus estimates call for operating leverage, but not nearly to that extent.

Seeking Alpha

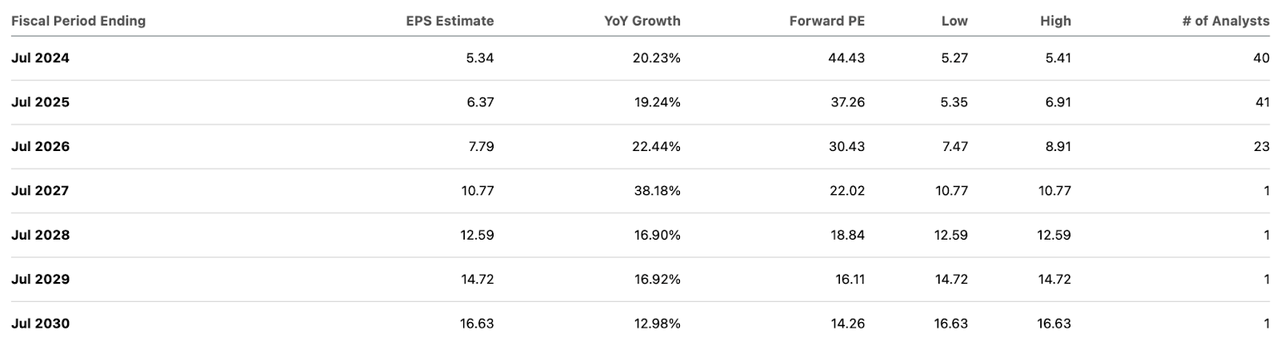

PANW is one of the big winners in the market and that typically leads to high expectations, but it looks like there’s a reasonable chance that the company manages to beat on expectations anyways. I previously modeled 28% long term net margins for the company. Based on management’s new long term guidance, I now use 32% as my new estimate. Together with 18% projected revenue growth and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see fair value hovering at around 8.6x sales. That implies solid forward upside between annual revenue growth and the earnings yield.

What are the key risks? I do not see material financial risk given the strong cash flow generation and net cash balance sheet. The company has the financial resources to survive any market downturn. Instead, the main risks stem from valuation and competition. If PANW were to disappoint on projected growth, then it may experience some multiple compression. The company’s GAAP profitability and strong balance sheet are likely to offer significant downside support, but in a market panic I could see the stock decline as much as 35% just to trade in-line with peers of a similar growth cohort. The company has benefitted from consolidation trends, but some may fear that having so many products may prevent PANW from investing as aggressively as more focused peers. It is possible that consolidation trends unwind though I note that PANW is still ranked highly among third-party vendors like Gartner in all of its product offerings.

I reiterate my buy rating for PANW stock as it offers an unbeatable blend of secular revenue growth and margin expansion.

Read the full article here

(NASDAQ:MU)")

")

2026-04-03")

")