2026-04-02")

")

BP (NYSE:BP) is one of the largest crude oil companies in the world. The company has a market cap of over $100 billion and recently reported disappointed earnings pushing down its share price. As we’ll see throughout this article, despite that weakness, BP remains an interesting investment opportunity.

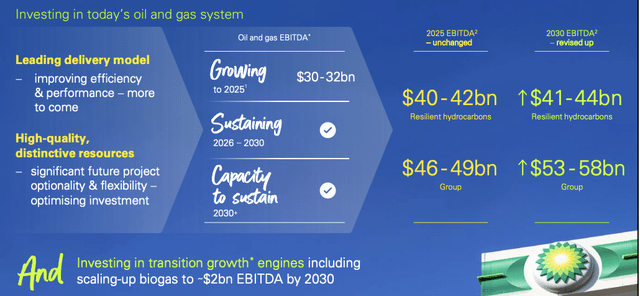

BP Value Growth

BP has continued to focus on long-term EBITDA growth and a strong asset portfolio.

BP Investor Presentation

The company expects hydrocarbons to form the core of its cash flow with group cash flow to increase. The company expects hydrocarbons to grow heavily by ~30% to 2025 with EBITDA of ~$41 billion. Total group earnings will be $47 billion, with the company’s new group businesses making up ~15% of its EBITDA.

By 2030, the company expects hydrocarbon growth to stop. However, they expect group income to grow towards $56 billion, making up almost 30% of group earnings. That’s some significant strength for the business, that will enable long-term shareholder returns.

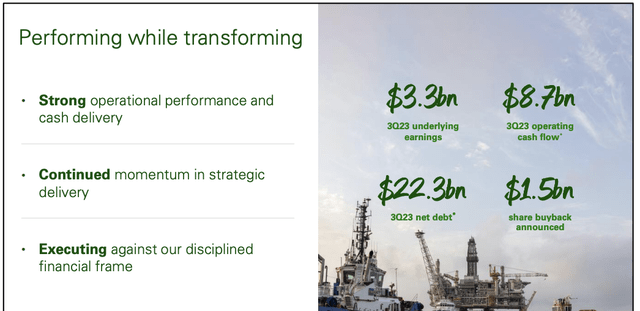

BP Continued Performance

The company has continued to perform incredibly well, with a strong portfolio of assets.

BP Investor Presentation

The company keeps net debt incredibly manageable. The current $22.3 billion net debt level is more than sustainable for the long run for the company. The company had $3.3 billion in underlying earnings in the most recent quarter, annualized into a single-digit P/E and almost $9 billion in operating cash flow, besides the company’s substantial capital expenditures.

The company announced $1.5 billion in share buybacks, which we expect to continue, given the company’s strong cash flow.

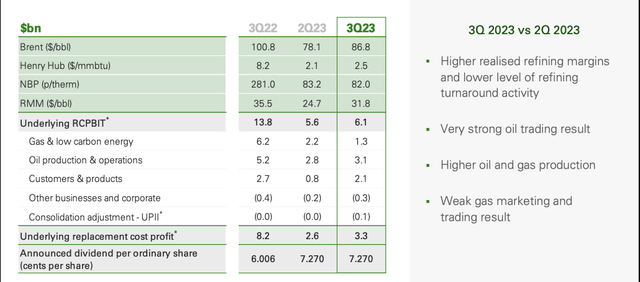

BP Investor Presentation

The company benefited from strong Brent crude prices in the quarter, especially over the prior quarter, along with strong natural gas prices. Oil trading in particular also performed very well for the company. The company’s underlying profit has gone down YoY especially as a result of lower natural gas prices, but its overall earnings versus its valuation remain incredibly strong.

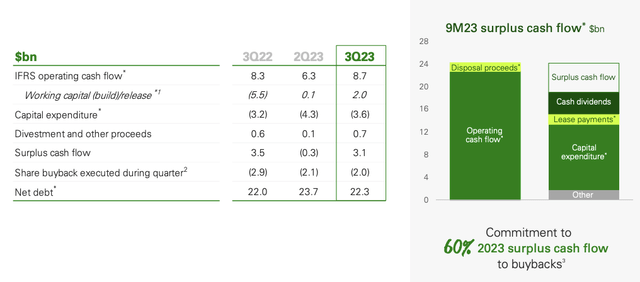

BP Balance Sheet

The company continues to maintain a strong balance sheet showing its asset strength.

BP Investor Presentation

The company earned $8.7 billion in operating cash flow in the most recent quarter. For the first 9 months, the company’s surplus operating cash flow has been $24 billion, and the company remains committed to spending 60% of the post-dividend surplus towards buybacks. Capital expenditures remain high, with annualized FCF at roughly $20 billion.

For a company with a market cap of $100 billion, this shows the valuation gap that European companies have with American ones, as the company continues to have a double-digit cash flow yield. The company continues to have an almost 5% dividend yield, and share buybacks remain strong, annualized at roughly 8%.

Net debt remains minimal and more than affordable, and with the company’s balance sheet, we expect strong long-term returns.

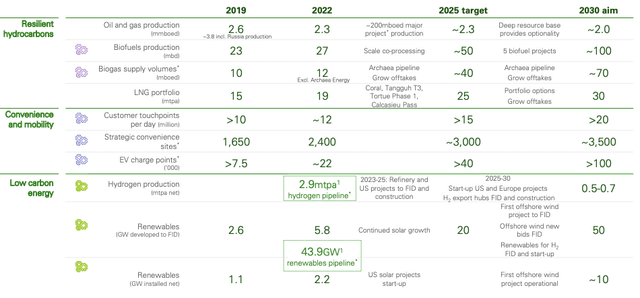

BP Financial Targets

The company’s financial targets show its focus on transitioning while demand for traditional fuels remains strong.

BP Investor Presentation

The company expects to almost quadruple biofuels production. At the same time, it’s planning to let oil and gas production decay. Just over 10% decay from 2.3 million barrels / day to 2.0 million barrels / day will have a noticeable cashflow impact. The company’s almost doubling in size of its LNG portfolio is a major strength.

Natural gas remains in incredibly high demand as a transition fuel, which helps the company. The company’s focus on low carbon energy is clear. The company is planning to quintuple EV charge points and build a hydrogen production business with noticeable size. Renewables, with the company’s pipeline, will be one of its largest businesses.

Acquisition Opportunity

BP maintains a strong business as it focuses on an energy transition. However, European energy companies consistently also have much lower margins than American ones. Combined with the recent two mega-acquisition deals that have been announced in America, we expect increased European consolidation.

BP, as one of the largest companies, is ripe to participate. Royal Dutch Shell, Equinor, etc. are all major companies that could participate, or another American energy company like ConocoPhillips could participate. Regardless, BP’s strong asset portfolio and the hefty competition in the market, mean we think it’ll soon be part of a large acquisition.

Thesis Risk

The largest risk to our thesis is two-fold.

The first is that the company is reorienting its portfolio towards renewable energy. The problem is renewable energy isn’t as complex or existing asset dependent as oil and gas and as a result, the margins are lower. That could hurt the company’s ability to continue driving long-term returns for interested shareholders.

The second is that the company is still dependent on crude oil prices in the meantime. Any substantial downturn in demand here could impact the strength of its cash flow and its ability to both fund a transitionary portfolio and manage to succeed in the long-term. Both of these risks are worth paying close attention to.

Conclusion

BP has a strong portfolio of assets. The company has profited heavily from higher oil and natural gas prices, however, it’s also been pushed by a commitment to decrease oil and natural gas production, which are more competitive and higher margin fuels. Despite that punishment, we expect BP to continue its performance.

The company continues to maintain strong cash flow from its core portfolio and repurchase shares. Those share repurchases are in the high single-digits, on top of its reasonable dividend, and incredibly profitable. The company’s overall financial strength here is key, and overall, BP is a valuable long-term investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

2026-04-02")

")

")