")

")

Investment Thesis

DocuSign (NASDAQ:DOCU) is about to report its fiscal Q3 2024 results in a few weeks. And admittedly I don’t expect much in terms of fireworks, but I do believe that sentiment has sufficiently washed out that this stock is now a more attractive buy.

As you’ll see, its financials do not inspire much confidence, but I suspect we may start to see its large $300K annualized accounts start to flat line or perhaps even start to deliver negative y/y growth rates.

In essence, DOCU has completely fallen out of favor with investors. So while it must be said the stock evidently has hairs on it, I am actually more bullish than I’ve been for a while. Why?

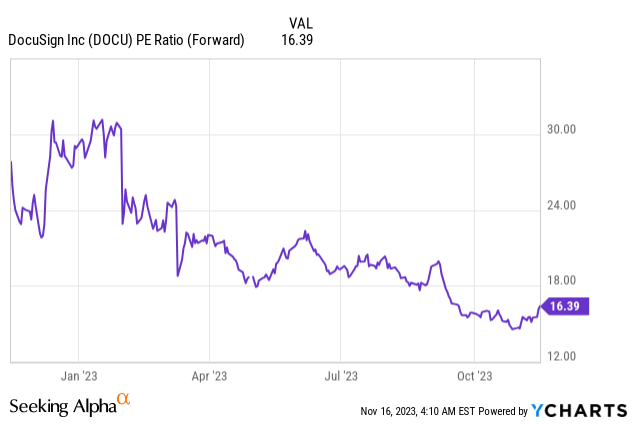

Because the stock is priced at 16x forward EPS. Nobody is expecting a lot from this company. But if it continues to tick along over time, from this point, it could still return a fair return, provided its multiple doesn’t compress more.

To put it succinctly, I believe that this stock will probably return around 15% to 25% over the next twelve months.

Quick Recap,

In my previous analysis on 10 August before Q2 2023 results were out, I said,

“DocuSign has seen investor sentiment wash out, leaving the stock much more attractively priced. This is not a clear-cut buy recommendation, as there are still some considerations that weigh on the stock.

But taking everything into account, I weigh up the fact that investors’ expectations for DocuSign are much lower now than they were a few years ago, even though its value proposition continues to expand, albeit slowly.”

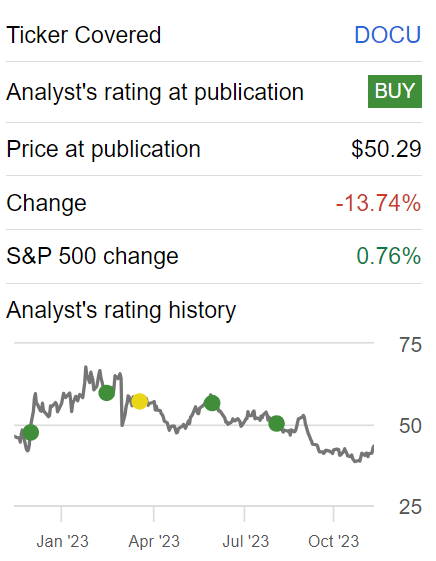

I put out a tepid buy rating on the stock, and as you can see below the stock has trended lower.

Author’s work on DOCU

Nonetheless, I remain tepidly bullish on this stock. After all, this is a very mixed thesis, where the only aspect that has going for it, is that anyone that wanted out of DocuSign has most likely already capitulated.

In other words, the update to this analysis is that as we head into DocuSign’s Q3 2024 results on 7 December, investment sentiment has fully washed out and is likely to have bottomed out.

DocuSign’s Near-Term Prospects

Recall, that DocuSign has spent several years striving to move its narrative away from it being a pure-play eSignature business.

Instead, DocuSign states that it is concentrating on the agreement management layer, aiming to simplify the customer experience.

The introduction of features like Liveness Detection for ID Verification demonstrates a commitment to security and efficiency in agreement processes. This technology uses biometric checks to prevent identity spoofing, contributing to more accurate verification without the signee being present.

Web Forms and DocuSign Monitor are additional components of DocuSign’s strategy to automate and streamline agreement processes. DocuSign Monitor, on the other hand, provides a comprehensive view of user activity for both Contract Lifecycle Management and eSignature, enhancing security and risk management.

DocuSign’s emphasis on expanding its Contract Lifecycle Management offering is noteworthy. The company recognizes the potential in transforming how organizations automate end-to-end agreement processes.

Now, let’s unpack a few noteworthy bearish trends.

DOCU revenue growth rates

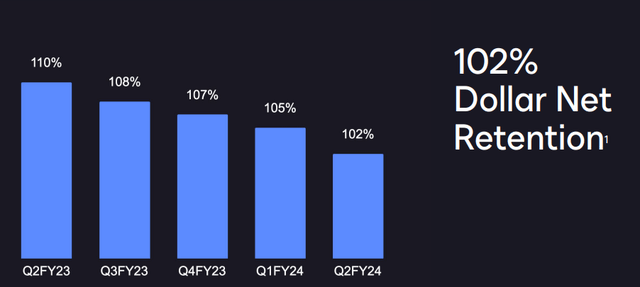

A picture is worth a thousand words. Not only are we looking at several consistent quarters of a decrease in net dollar retention, but the outlook for fiscal Q3 2024 is guided for further compression.

Since I suspect this net dollar retention figure includes a fair amount of price hikes, I believe the single biggest takeaway from this thesis is that DocuSign’s customer base is no longer rapidly growing as they don’t see enough value to adopt its platform; an argument that is supported in the following graphic.

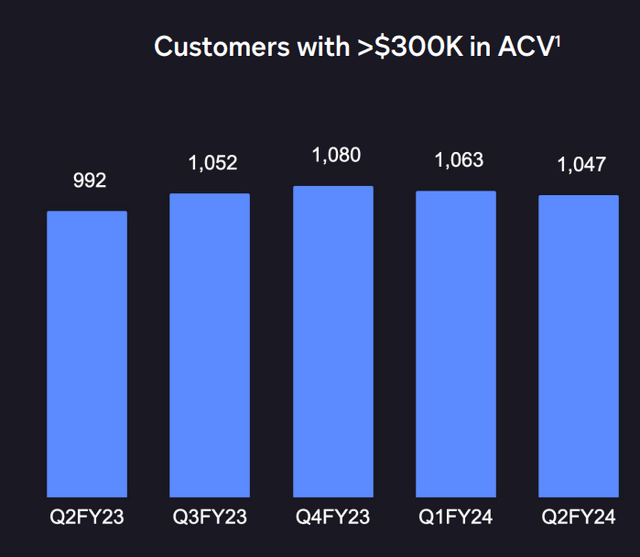

DOCU fiscal Q2 2024

We are probably eyeing up another quarter or so before DocuSign’s customers spending more than +$300K per year start to post negative y/y growth rates.

Altogether, this is hardly a bullish picture.

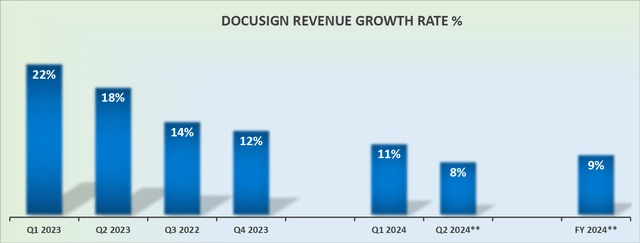

Revenue Growth Rates Have Fully Fizzled Out

DOCU revenue growth rates

Looking back, it now feels like a really long time ago when DocuSign was viewed as a growth company. Even as its comparables ease up, this company’s growth rates continue to decelerate.

This consideration, when combined with the fact that its customer adoption has started to meaningfully slow down, simply leaves a lot to be desired.

That being said, as I look out to fiscal 2025, as its comparables ease up, I trust that it will be easy to see a scenario where DocuSign could grow by around 10% on the top line.

DOCU Stock Valuation — What’s Fair Value?

This is where the bear case fails to gain traction. So far, I’ve described a mixed thesis. That being said, the stock is already priced at 16x this year’s EPS.

So unlike many of its tech peers, this business is in actuality fairly profitable. Investors are not asked to pay a lot to participate in this stock.

I believe that if the share price was around 20x forward P/E, I would make the case that this not a buy, but rather a hold.

Again, my thesis is not so much that I’m looking for a multiple expansion. My thesis argues that as long as DocuSign continues to grow at about double digits on the topline and it improves its cost structure ever-so-slightly, its EPS should most likely grow by around 10% to 15% over the next twelve months.

Hence, I believe that paying around 16x forward earnings for a business that’s growing its EPS at somewhere around 10% to 15% CAGR, is a very fair entry point.

SA Premium

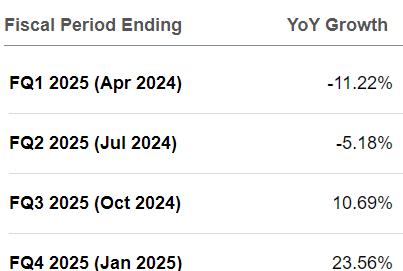

And yet, as you can see above, analysts find themselves highly bearish on the stock, projecting that DocuSign’s EPS continues to move into negative growth rates.

The Bottom Line

My analysis leads me to maintain a cautiously optimistic outlook on DocuSign.

Despite the evident challenges highlighted, including a slowdown in customer adoption and a dip in revenue growth rates, the stock’s current valuation at 16x forward EPS presents a compelling entry point.

Investors’ expectations for the company have markedly decreased in recent years, and while the road ahead may not be without hurdles, the subdued sentiment seems to be already priced into the stock.

The market’s skepticism, combined with the company’s strategic focus on agreement management and notable security enhancements, positions DocuSign as an intriguing investment opportunity for those willing to embrace a tempered perspective.

In conclusion, this is a stock for investors who are looking for a cheaply valued, slow and steady, well positioned digital-enabling business.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")