")

")

Investment Thesis

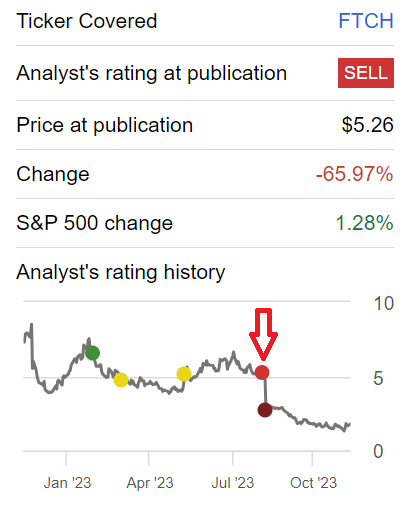

Farfetch (NYSE:FTCH) is about to report its Q3 2023 results on Wednesday, 29 November, premarket. And I argue that this stock is still a sell and that its problems will not go away, namely the issues pertaining to its balance sheet are only going to continue to get worse.

Even though the stock is already down more than 60% since I issued my previous sell rating, investors should not seek to double down on this stock.

Quick Recap,

In my previous analysis back in August, I said,

There are so many different blemishes in this report that I find it difficult to highlight anything positive.

For their part, Farfetch remains adamant that they are a growth business and that the issues they face are not specific to Farfetch.

Nevertheless, with full respect, I personally disagree. This stock is a sell.

[…] I also know that it’s much better to be upfront and deal with the situation now rather than later on, in a year’s time. The waters won’t calm. Farfetch is swimming against the tide while being anchored down by its balance sheet. I argue that it’s drifting towards “Far-fetched”ruptcy.

Author’s work on FTCH

With the benefit of hindsight, I was spot on to turn bearish on this stock. I made the case that this investment has too many hairs on it. And that rather than waiting to return to breakeven, investors would be better to salvage their capital and seek different investment opportunities.

Even though, I fully recognize that this is a very difficult investment decision to make that’s fully lathered with challenging emotional decisions.

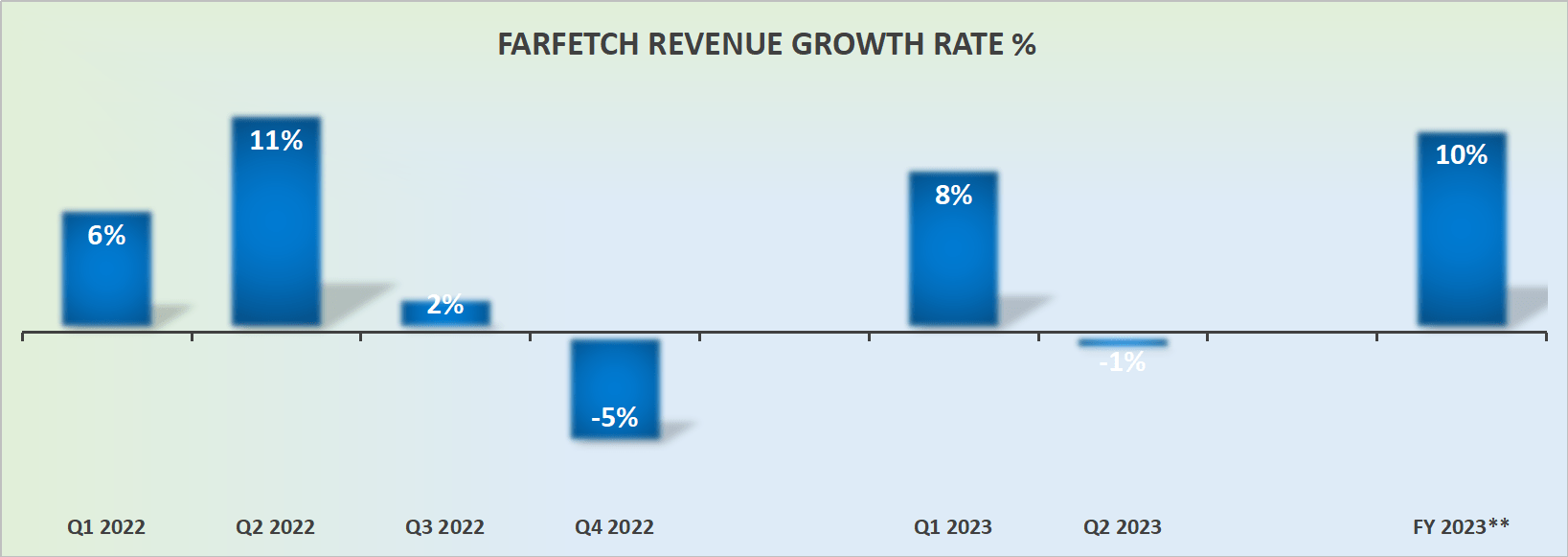

Revenue Growth Rates Outlook for H2 2023

FTCH revenue growth rates

Let me make something clear. Nobody debates that Q3 2023 will deliver some growth. The question is how much growth can we expect from Farfetch coming out of Q3 and into the all-important Q4 holiday season?

Recall that Farfetch makes the bulk of its free cash flows in Q4, but even if its free cash flow isn’t particularly strong in Q4, what investors and stakeholders want to see is how much confidence can management exude during its earnings call that Q4 will be strong.

After all, Q4 of last year was negative, so the comparables will already be fairly easy. Consequently, for Farfetch to unofficially guide for Q4 to be up by double digits, meaning around 10% to 12% would not be a difficult feat.

But if this is the case, getting around 10% to 12% CAGR in Q4 would hardly position Farfetch as a growth business in the eyes of all stakeholders. Here, I’m not only referring to investors but also potential partnership brands as well as talented executives in the C-suite.

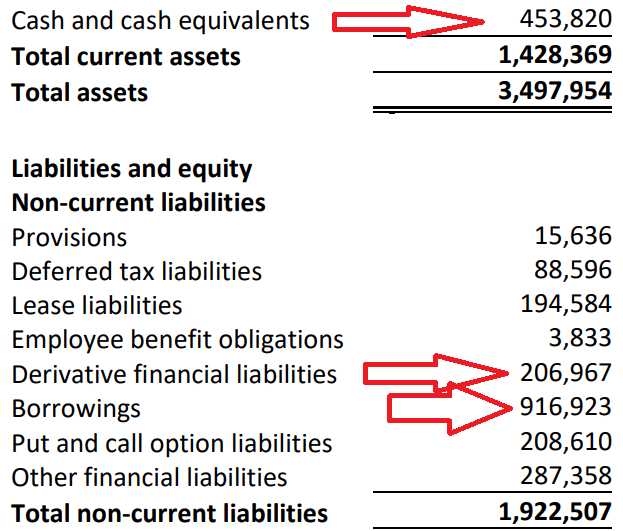

Focus on the Balance Sheet

FTCH Q2 2023 balance sheet

Above we see that Farfetch entered Q3 with $450 million of cash and approximately $1 billion of borrowing and financial derivatives. But we also know that after Q2 results, Farfetch drew down $200 million of debt, here’s the SEC filing stating this much.

On September 11, 2023, the Company borrowed the full $200.0 million Delayed Draw Term Loan.

What this means is that at the same time as the business’ growth prospects have dramatically slowed down, Farfetch is reaching to take on debt to bolster its balance sheet.

Therefore, when Q3 reports next week we should expect to see at least $600 million of cash on its balance sheet. While, at the same time, we’ll see that its debt outstanding will have increased by $200 million.

Why not a full $200 million increase in the cash position? Because part of the financial terms of the deal involved giving a discount on the debt. This means that for the interest rate on the debt to remain at a manageable 5%, Farfetch had to sell debt at a discount to motivate creditors to take the debt, but otherwise, the business would be operating with even more restrictive conditions.

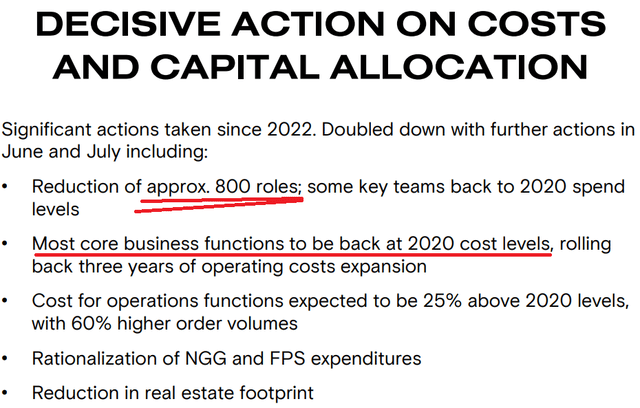

FTCH Q2 presentation

On top of leaning on its balance sheet to stay afloat, Farfetch is dramatically reducing its team, by cutting around 800 roles.

And finally, to put the last nail in the coffin, Farfetch can’t even raise more capital by diluting shareholders, as its share price has tumbled so precipitously as investors lack confidence in its overall prospects.

The Bottom Line

Farfetch presents a compelling case for investors to exercise caution and avoid this stock.

The persistent challenges surrounding its overleveraged balance sheet continue to worsen, with the company resorting to taking on additional debt despite evident signs of slowed growth.

The recent reduction in workforce and the inability to raise capital through share dilution due to a sharply declining stock price further underscore the precarious position Farfetch finds itself in.

The upcoming Q3 2023 results may reveal a temporary boost in cash reserves, but the simultaneous increase in debt raises concerns about the sustainability of its financial position.

The management’s optimistic outlook for the crucial Q4 holiday season needs to be met with skepticism, given the broader financial constraints.

In light of these factors, prudence dictates that investors steer clear of Farfetch, as the risks associated with its overleveraged financial structure outweigh any potential short-term gains.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")