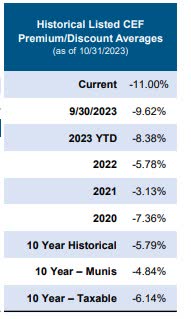

I tend to be quite interested in closed-end funds at the end of the calendar year. It is a time when there are many funds with deep discounts on net asset value. This year, the picking is particularly rich. I’ve been going over many funds. This particular one, XAI Octagon Floating Rate & Alternative Income Term Trust (NYSE:XFLT), isn’t a top favorite. Yet, I figured there is value in that perspective as well. Before I get into this specific fund, I wanted to highlight some data that this fund manager made available. The firm puts out data showing the historical discounts that closed-end funds trade at. It varies throughout the year, but the current 11% discount stands out going back to 2020.

CEF discount to NAV (xainvestments.com)

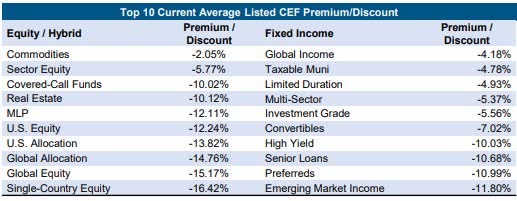

There are big differences between categories of funds, which the manager also laid out for us. On the equity side, I guess the discounts are deeper than usual, but from experience, these categories tend to trade at deep discounts. I think real estate may be particularly deeply discounted, but that may be due to the real challenges commercial real estate faces and the fast change in interest rates.

CEF segment discounts (xainvestments.com)

On the fixed income, emerging market income trades at the deepest discount, which isn’t unusual. The discount on limited duration, convertibles, and senior yields seems attractive from a top-down perspective. I’m surprised munis don’t trade at deeper discounts according to their data because I recently wrote up one trading at a 13.88% discount. I guess this is due to major regional differences. Anyway, the closed-end fund universe looks quite attractive, and I’ll continue reviewing as many funds as I can while it lasts.

To get into XAI Octagon FR & Alt Income Term Trust specifically, it is a fund that wants to offer a total return emphasizing income generation. A prevalent goal in this space that Octagon wants to achieve is investing in floating-rate credit instruments and other private credit. It has a market cap of around $261 million and $408 million in assets.

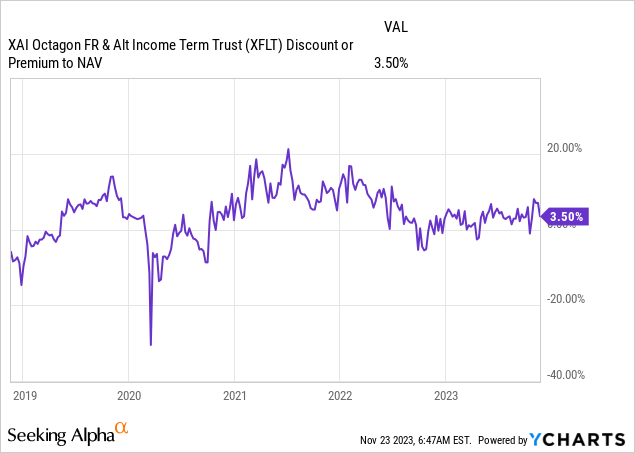

A big problem is that the fund is trading at a premium to net asset value:

It is unusual, but the fund has managed to maintain its premium for a long time. It is trading very close to its average premium. The only time XFLT briefly flipped to a discount was in March 2020, as COVID fears materialized in almost all markets. The premium to NAV is probably explained because the fund has a distribution rate of 14.68% on NAV. It achieves this through an effective leverage percent of 41.40%.

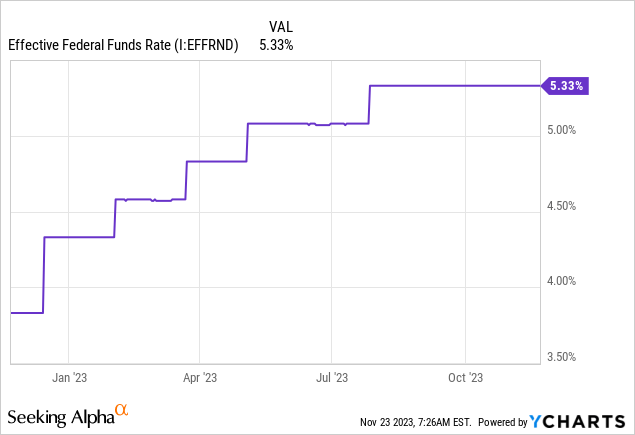

It has done well in the past year as interest rates have surged. That makes sense because it partly borrows at a fixed rate through the preferreds it has outstanding (borrowing at around 6%) while its portfolio includes mostly floating rate exposure, meaning that it has benefitted greatly from the rising rate environment.

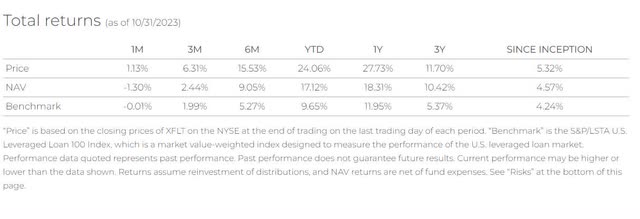

Total returns XFLT (xainvestments.com)

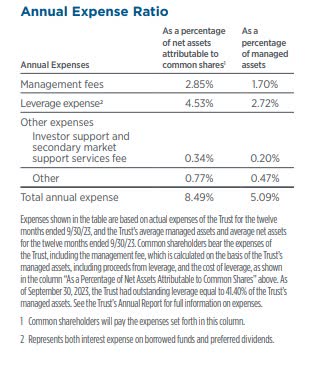

The second thing that puzzles me about this fund is the management fees. These are 1.70% of all assets under management.

Fees XFLT (xainvestments.com)

Borrowing costs are 4.53% as a percentage of net assets. The company has ~$250 million in net assets. That means its borrowing costs were roughly $11.3 million. It borrowed roughly $135 million through preferreds, convertibles, and a credit facility. The average interest rate it has been paying over the past year should be ~8.3%. It should be slightly higher now as interest rates marched upward throughout the year:

The fund is paying 6% on its preferred shares, which has been advantageous. It used to pay only 2.97% on its credit agreement in 2022:

Assumes Indebtedness under the Credit Agreement in an amount equal to $110,650,000 at an annual interest rate to the Trust as of July 1, 2022 of 2.97%. The costs associated with such Indebtedness are borne entirely by Common Shareholders.

I’m not sure what the rate is now, but I’m guessing it is more like ~9%+. The preferred and the converts are holding down their average interest costs, but the credit facility is its largest source of leverage and is driving up its average borrowing costs.

I have no doubt part of the performance here is due to management skills. The portfolio looks very interesting. However, sustaining a distribution rate of ~14% seems hard while charging 1.7% on all assets. Currently, returns on the assets have to overcome interest expenses of ~5%, a management fee of 1.7%, and a distribution rate of 14%. It adds up to 20.7% in returns required for the distributions to be sustainable.

Morningstar calculated the weighted coupon at 11.66%. According to the manager, the average issue in the portfolio is trading at 85% of par, with a maturity of 7.41 years. For convenience’s sake, let’s say the yield to maturity is around 14%. I guess the shortfall of 6% annually would have to be made up through management alpha. I don’t think that’s very realistic. For this reason, I think distributions shouldn’t be viewed as sustainable.

However, there are additional challenges because the outstanding preferreds with a coupon of 6.5% mature in 2026. I’m not convinced the preferreds will be able to get refinanced at that rate again. The fund has a termination date in December 2029 (extensions of 1.5 years are possible). That means the premium to NAV will disappear if it is still present.

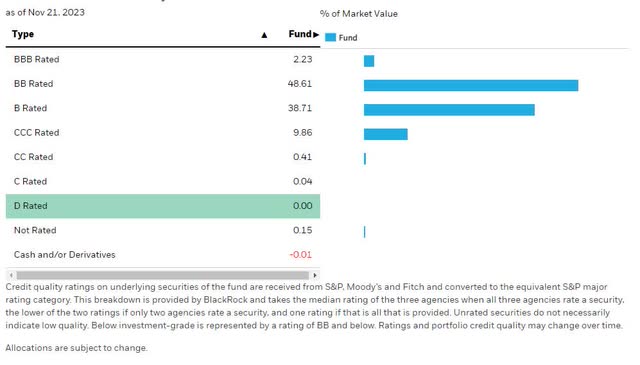

The most important thing is that I’ve assumed no defaults. Meanwhile, the iShares iBoxx $ High Yield Corporate Bond ETF has an average yield to maturity of 8.52%. I think it is probably overvalued, but the yield difference is likely due to a higher risk appetite. This is the credit overview of HYG:

HYG portfolio credit rating (iShares)

Again, no doubt management can generate alpha over HYG, but I do think the XFLT portfolio has a riskier composition:

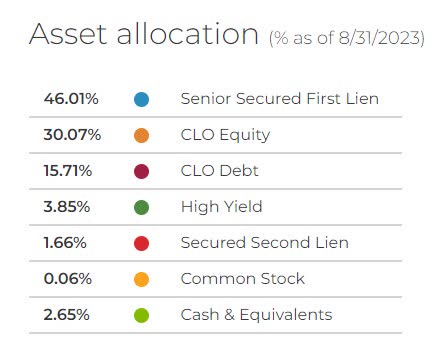

Asset allocation XFLT (xainvestments.com)

A CLO is a pool of leveraged loans (i.e., loans given to companies with high levels of debt) and then issues securities. CLO equity tranches are the riskiest. CLO debt is a riskier category than high-yield as well. The Senior Secured First Lien category is still generating high yields from less than well-capitalized borrowers, but if there are defaults, these should hold up much better.

A few final things I want to mention is that I’m not entirely convinced it is worth borrowing at ~9% to invest at ~14%. Yes, you’re picking up a large yield differential, but to me, it looks precarious. Exposure to floating rates has been a great trade over the past year. However, if it is high for longer, as the Fed is communicating right now (which is being discounted by the treasury markets), this will increasingly lead to defaults ticking up. So far, default rates have been meager, but that will not necessarily remain true.

Defaults have the nasty habit of clustering, i.e., companies are simultaneously paying their obligations or defaulting. The defaults tend to go up during slow economic or recessionary periods. Defaults on high-yield debt were 4% in 2008 and 14% by the end of 2009. Interest rate hikes often precede recessions. If the Fed increases rates further, things get increasingly perilous. Sure, you’re getting a higher yield, but ultimately, this is capped by the diminishing capacity of the borrower to pay. Current default rates are around 2.5%-2.8%, and all major rating agencies expect the rate to increase by 30% or more next year.

To summarize, the landscape of closed-end funds looks beautiful right now. Different types of funds trade at different discounts to their net asset value. XAI Octagon FR & Alt Income stands out as a fund trading at a premium to NAV. It has a great track record, and the portfolio looks interesting and differentiated. I do have concerns the distributions could be unsustainable at the current level. If rates continue to go up, it increases costs, but I’d expect it to increase defaults, and the ability to increase interest income may lag. There are many attractive closed-end funds right now, and I think I can find better spots than this one.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")