")

")

The EL Investment Thesis Appears To Be Underwhelming Here

Estée Lauder (NYSE:EL) is a company that requires no introduction to readers whom are familiar with skin care and make up products, attributed to its well-diversified globalized brands. The list includes the luxurious La Mer, the run-way favorite MAC, and the Jo Malone fragrances.

While the demand for these products have boomed in 2021 and 2022, the reverse is true now, with the uncertain macroeconomic outlook tightening discretionary spending and compressing its profit margins below the hyper-pandemic and pre-pandemic averages.

The same has been reflected in EL’s elevated inventories of $2.86B (-3.7% QoQ/ -4.9% YoY) in the latest quarter, compared to FY2019 levels of $2B (+24.2% YoY).

This implies impacted global consumer demand, worsened by the Chinese government’s crackdown on daigou (people who buy goods abroad to resell them in China to avoid taxes), ongoing conflict in Ukraine and Israel, and the volatile forex headwinds.

Perhaps this is why EL has reported a disappointing FQ1’24 earnings call, with revenues of $3.51B (-2.5% QoQ/ -10.5% YoY) and adj EPS of $0.11 (+57.1% QoQ/ -91.9% YoY).

Part of the profit headwinds is likely attributed to the impacted Average Selling Prices, as demonstrated by the consistently declining gross margins of 69.6% (+1.7 points QoQ/ -4.2 YoY), compared to its FY2019 levels of 77.4% (-1.9 points YoY).

To make matters worse, EL has lowered its FY2024 adj EPS guidance to $2.21 at the midpoint (-36.1% YoY), down drastically by -38.9% from its previous FY2024 midpoint guidance of $3.62 (+4.6% YoY).

This may be attributed to the poor FQ1’24 sales reported in the EMEA at $1.25B (inline QoQ/ -25.5% YoY) and APAC at $1.05B (-19.2% QoQ/ -7% YoY), with the Americas remaining stable at $1.2B (+12.1% QoQ/ +7.1% YoY).

With the Chinese economic recovery still uncertain and the brand’s eroding market share compared to L’Oréal, it seems that EL’s previous 2025 profit recovery plan may be delayed after all.

In addition, the management has made minimal efforts to optimize costs, as demonstrated by the stable operating costs of $2.33B in the latest quarter (-2.5% QoQ/ +4% YoY).

While EL has attempted to drive growth by acquiring Tom Ford in 2022, we believe the timing has not been ideal, attributed to the latter’s expensive valuation worth $2.8B and the elevated interest rate environment.

The latter has directly contributed to its deteriorating balance sheet, with a growing net debt of -$3.99B (-29.1% QoQ/ -83.8% YoY) and annualized net interest expenses of $216M (+17.3% QoQ/ +74.1% YoY) in the latest quarter.

As a result of the slowing sales growth, gross margin compression, and elevated expenses, it is unsurprising that EL’s prospects in the intermediate term are highly uncertain.

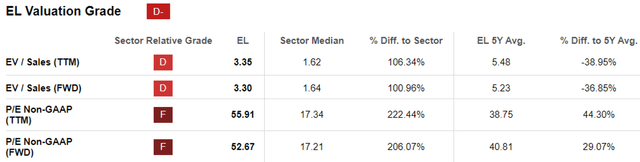

EL Valuations

Seeking Alpha

In addition, EL’s FWD EV/ Sales valuations of 3.30x and FWD P/E valuation of 52.67x appear to be massively inflated compared to its 1Y mean of 4.50x/ 41.29x, 3Y pre-pandemic mean of 3.64x/ 28.80x, and the sector median of 1.64x/ 17.21x, respectively.

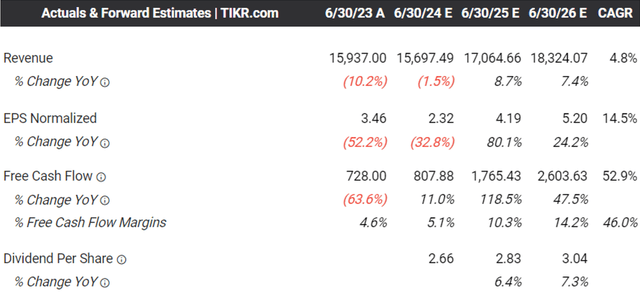

The Consensus Forward Estimates

Tikr Terminal

This may be attributed to the supposedly optimistic consensus forward estimates, with EL expected to generate a top and bottom line CAGR of +4.8% and +14.5% through FY2026, compared to its historical trend at a historical CAGR of +5.1% and +1.1% between FY2016 and FY2023, respectively.

Then again, we must highlight that the company has generated minimal profit growth over the past few years, with the consensus FY2026 revenue estimates of $18.32B and adj EPS estimates of $5.20 still underwhelming, when compared to its FY2019 revenues of $14.86B and adj EPS of $5.34.

Based on the EL management’s FY2024 adj EPS guidance of $2.21 at the midpoint and its normalized FWD P/E valuation of 28.80x, there appears to be a minimal margin of safety to our fair value of $63.64 as well.

While there seems to be a decent upside potential of +24.6% to our long-term price target of $149.76, based on the consensus FY2026 adj EPS estimates of $5.20, we believe that the stock’s investment thesis is not compelling enough here.

So, Is EL Stock A Buy, Sell, or Hold?

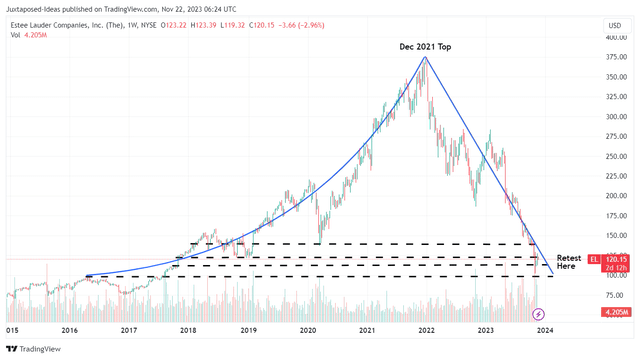

EL 10Y Stock Price

Trading View

For now, EL has already lost much of its pre-pandemic and hyper-pandemic gains, with the stock also plunging to its 2017 lows at the time of writing. Based on its lower lows and lower highs since the December 2021 top, we are unsure if there is a floor to this decline in the near term.

While some income oriented investors may be tempted by the expanded forward dividend yields of 2.16%, compared to the 4Y average of 0.91%, we believe that there are many better options out there now, such as the US Treasury Yields of between 4.42% and 5.43%.

Lastly, EL’s dividend investment thesis appears to be uncertain in the near-term, attributed to its impacted TTM Interest Coverage ratio of 3.95x, TTM Dividend Coverage ratio of 0.58%, and TTM Dividend Payout ratio of 120.55%, compared to the sector median of 7.54x, 1.81%, and 48.18%, respectively.

For now, the Fed expects a normalized economy only by 2026, implying that market sentiments surrounding the beauty company may still be pessimistic over the next few quarters, with bullish support unlikely to materialize yet.

As a result of the potential volatility, we prefer to prudently rate the EL stock as a Hold (Neutral) here.

Interested investors may be better off waiting until a floor is found. Even then, they must also temper their expectations since its reversal may take much longer than expected.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")