")

")

Introduction

In the high-stakes arena of aerospace manufacturing, Spirit AeroSystems (NYSE:SPR) stands as a case study in navigating complex financial and operational challenges. As we dissect Spirit AeroSystems’ financial statements, a picture of a company at a crossroads emerges. The erosion of gross profit margins, a balance sheet reflecting a precarious blend of liquidity and substantial debt, and a stock performance echoing investor skepticism, all paint a picture of a company in dire need of strategic recalibration. This analysis aims to unpack the layers of Spirit AeroSystems’ financial situation, providing insight into the challenges it faces and the potential pathways it might explore to navigate through this turbulent phase. In doing so, we will also offer a perspective on investment strategies in the context of Spirit AeroSystems’ current market position, evaluating the potential risks and opportunities that lie ahead for this key player in the aerospace sector. We believe that SPR needs a large operational revamp and due to that we do not see any risk-adjusted upside for equity holders in the next 12-24 months. We place a rating of ‘Sell’ and a Price Target of $18.

Navigating Financial Turbulence: A Closer Look

Spirit AeroSystems’ financial journey is akin to navigating a storm. The revenue of $1.43 billion, while substantial, is overshadowed by an even higher cost of revenue at $1.49 billion. This imbalance has led to a notable net loss of $204 million, painting a picture of operational and financial inefficiency. The negative EPS of -$1.94, albeit a slight improvement from the previous quarter’s -$1.96, is a stark reminder of the company’s struggles with profitability. This continuous trend of losses raises red flags about the company’s operational model, cost management, and market adaptability.

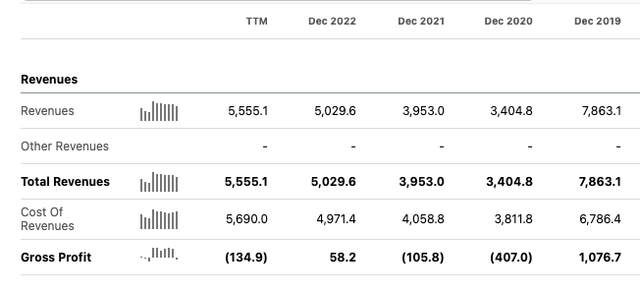

Gross Profit SPR (Seeking Alpha)

SPR’s income statements reveals that the company is grappling with a narrowing gross profit margin. This issue stems primarily from the escalating costs of goods sold (COGS), which are outpacing revenue growth. In a sector like aerospace, where production and material costs can be high, such a trend is particularly concerning. This imbalance between revenues and COGS suggests inefficiencies in SPR’s production process or perhaps rising costs of materials and labor that the company has been unable to offset through its pricing strategies. Add in labor issues and quality issues the operational challenges that SPR currently faces are indeed formidable. Consequently, this erosion of gross profit margin puts additional pressure on the company’s overall financial health, limiting its ability to invest in growth opportunities or manage its existing debt load effectively. Addressing these gross profit challenges is crucial for SPR, as it seeks to stabilize its financial position and reassure investors of its potential for sustainable profitability in the highly competitive and capital-intensive aerospace industry.

The Dichotomy of the Balance Sheet: Delving Deeper

The balance sheet of Spirit AeroSystems is a juxtaposition of strength and vulnerability. On one hand, the company’s liquidity, marked by its $374 million in cash and equivalents, provides a cushion against short-term financial pressures. This liquidity is crucial in enabling the company to manage its day-to-day operations without the immediate threat of cash flow insolvency.

However, the other side of the ledger presents a worrying scenario. The company’s total debt stands at an alarming $3.97 billion, with net debt of $3.59 billion. This high level of indebtedness not only puts pressure on the company’s future cash flows but also raises questions about its long-term financial sustainability. The negative total equity of -$855 million is a further indicator of past struggles and accumulated losses. This negative equity suggests that the company has been eroding its value, potentially diluting shareholder confidence and making it challenging to attract new investment.

This dichotomy in the balance sheet reflects a critical balancing act for the management. On one hand, there is a need to maintain sufficient liquidity to ensure operational continuity. On the other, the company must address its substantial debt and negative equity to restore financial health and investor confidence.

To address its financial needs, Spirit AeroSystems intends to generate $200 million through the sale of its Class A common stock and an additional $200 million via convertible debt, set to mature on November 1, 2028. This decision underscores the company’s reliance on equity financing in the wake of its recent struggles.

Expanding on Stock Performance and Investor Sentiment

Google

The stock performance of Spirit AeroSystems serves as a direct reflection of investor sentiment and market confidence in the company’s future. The significant decline in its share price to $26.35, a 14% drop YTD, is a clear indicator of the market’s apprehension. With a low of ~$15 range the news of a new Boeing contract is the only that has propelled them out of their 50% drop earlier in the year. This decline is not just a reaction to the company’s financial struggles, as outlined in its earnings reports, but also a broader reflection of uncertainties within the aerospace industry. Investors are seemingly wary of SPR’s ability to effectively manage its operational and financial challenges, such as high costs and substantial debt, in an industry known for its volatility and cyclicality.

This skepticism is further fueled by broader market trends and external economic factors that influence the aerospace sector, including fluctuating demand for air travel, shifts in defense spending, and the impact of global economic conditions.

Conclusion

Spirit AeroSystems’ journey through its current financial and operational storm is one that demands careful scrutiny from investors. The company’s struggles to achieve profitability, alongside its reliance on equity dilution and external fundraising to stay afloat, are red flags. These issues are compounded by management instability, further clouding the company’s future. Spirit’s vital role in the U.S. aerospace industry suggests it might not fail outright, but this alone does not guarantee a positive outlook for potential investors.

The company’s financial statements reveal deep-rooted challenges. The consistent inability to generate a substantial gross profit since 2019, which cannot be entirely attributed to the COVID-19 pandemic, indicates systemic issues in its operational model. Even with new contracts, the lack of significant gross profit points to inefficiencies that need addressing for any meaningful financial turnaround.

Moving forward, Spirit AeroSystems would need to embark on a rigorous path of restructuring and strategic realignment to regain investor confidence and financial stability. This would likely involve a thorough overhaul of its operational processes to address inefficiencies, a strategic approach to debt management, and possibly a reshaping of its management team to bring in fresh perspectives and stability.

We assign a ‘Sell’ rating to Spirit AeroSystems stock with a target price of $18. Currently, several potential catalysts could influence SPR’s market performance. These include securing new contracts, shifts in management, the impact of equity dilution, improvements in gross margins, and a path to profitability. However, given the company’s ongoing challenges, we anticipate that Spirit’s stock will likely experience lateral movement in the market for the foreseeable future.

Our strategy involves selling cash-covered Puts at approximately the $18 level over the next few quarters. This approach reflects a cautious stance, allowing us to capitalize on the company’s current market position while waiting for signs of substantial improvement. We believe this method is prudent until SPR demonstrates a concrete recovery, both financially and operationally. Only with clear evidence of Spirit AeroSystems regaining a stable foundation in these areas would we reconsider our position and outlook on the stock.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")