2026-04-03")

")

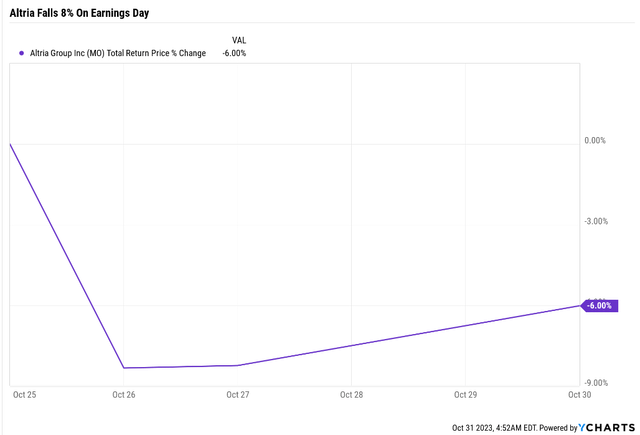

During earnings season, when stocks miss, they can be punished severely.

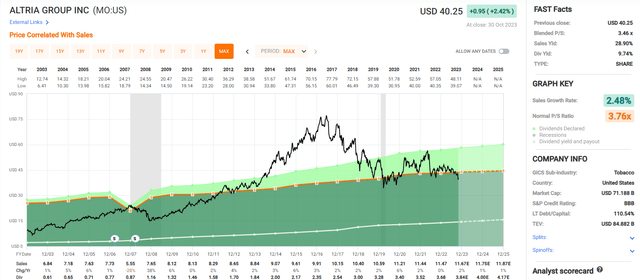

Ycharts

Altria Group (NYSE:MO) fell 8.3% on Q3 earnings day after missing both on revenue and earnings. Bearish analysts like this came out using the poor results to make extreme extrapolations.

- Altria: Its 10% Yield Is Not As Attractive As You Think.

Extrapolations that go as far as to claim that Altria should be considered no more than an oil trust on its way to zero, and thus, paying more than $32.5 for the stock is likely a bad investment.

- 6.5X forward earnings and 12.3% forward yield at those prices.

Articles like this make some valid points and point out some troubling trends.

So let’s review why the market dumped on Altria so hard on Thursday and what it means for this beloved almost 10% yielding dividend king.

Let me show you the good, the bad, the ugly, and the bottom line about Altria’s earnings to show you why, at a 10% yield, it’s the best time in 20 years to buy the greatest-performing stock in history.

The Good: The Dividend Is Still Safe And Growing Steadily

Altria

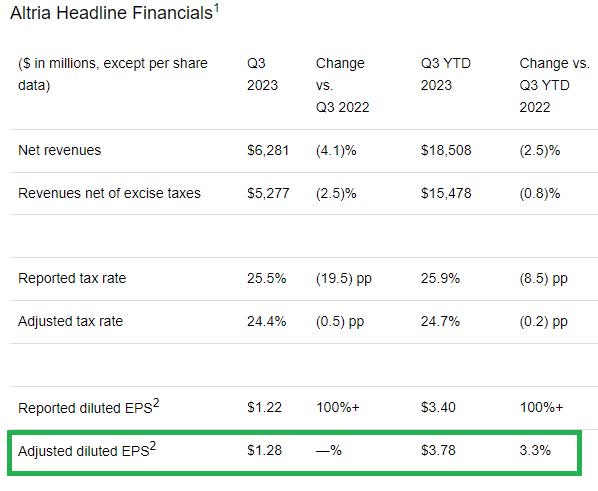

MO missed on the top and bottom lines, but not by much, and adjusted earnings were flat for the quarter and YTD, up 3.3%.

So MO didn’t fall 8% because earnings fell off a cliff.

What about the dividend? That wasn’t cut, but maybe management said something about the dividend that might hint at a future cut?

Turning to capital allocation. We continue to return significant cash to shareholders. In the third quarter, we paid approximately $1.6 billion in dividends and raised our dividend by 4.3% in August, in line with our new progressive dividend goal. This increase marked our 58th increase in the last 54 years, and we repurchased 5.9 million shares for $260 million.” – CFO, Q3 earnings call.

Nope, MO remains as committed as ever to its dividend king status.

OK, but maybe something in the report has analysts expecting a cut in the future? Maybe management is lying?

FactSet Research Terminal

After the earnings came out and analysts updated their models, there is no expectation of a dividend cut—just 3.4% income growth through 2027.

That’s in line with the new consensus growth rate of 3.6%.

FactSet Research Terminal

The long-term growth consensus has decreased from 4.6% (management guidance 4% to 6%) to 3.6%.

With the new yield, the long-term total return potential is now 13.4%, the same as before earnings came out.

OK, anyone buying today has the same return potential, just more income-based.

But what about if you bought MO before earnings? You still got it at a 9% yield, and that’s 12% to 13% long-term return potential or Nasdaq-like 12.5% base-case.

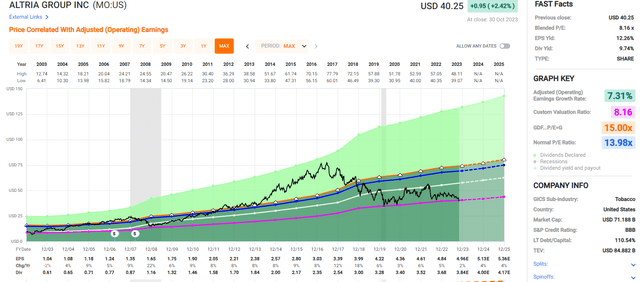

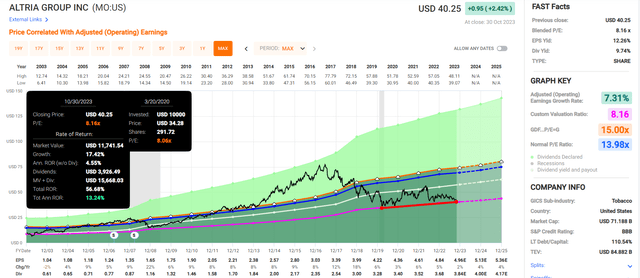

Fundamentals Summary

- yield: 9.7%

- dividend safety: 100% very safe (1% dividend cut risk) – negative outlook

- overall quality: 98% very low-risk Ultra SWAN dividend aristocrat

- credit rating: BBB positive outlook (7.5% 30-year bankruptcy risk)

- long-term growth consensus: 3.6%

- long-term total return potential: 13.3% vs 10.2% S&P 500

- current price: $40.25

- fair value: $61.15

- discount to fair value: 34% discount (potential Ultra Value Buy) vs 1% overvaluation on S&P

- 10-year valuation boost: 4.2% annually

- 10-year consensus total return potential: 9.7% yield + 3.6% growth + 4.2% valuation boost = 17.5% vs 10.1% S&P

- 10-year consensus total return potential: = 402% vs 160% S&P 500.

Altria could potentially turn $1 into $5 in the next decade thanks to the

FAST Graphs, FactSet

MO is now so cheap that its consensus two-year return potential is 110% or 5.5X more than the S&P 500.

That’s Joel Greenblatt’s 42% annual return potential if MO grows as the new expected 2% in 2023, 4% in 2024, and 4% in 2025.

The Bad: Cracks Are Starting To Show In Altria’s Transition Plan

For over 50 years, cigarette volumes have fallen annually with a single exception.

- A small increase in the Pandemic when everyone was stuck at home, and people smoked more.

Tobacco companies were able to raise their prices above the rate of volume declines, and people paid it because cigarettes are addictive.

Sales grew at a steady 2% to 3% annual rate even though the volume of cigarettes was falling.

Earnings, through cost-cutting and buybacks, grew much faster, in the case of MO, about 8% annually over the last two decades.

Management is guiding for about 5% long-term growth under the smoke-free transition plan that all tobacco companies have adopted.

In the future, there will be no cigarettes and possibly no tobacco at all (chew) but just vaping, heat sticks, and oral nicotine pouches, the so-called “reduced risk” products or RRPs.

- also possibly cannabis, according to MO and British American Tobacco p.l.c. (BTI).

The future of big tobacco is in big nicotine, which is still very much a growth industry.

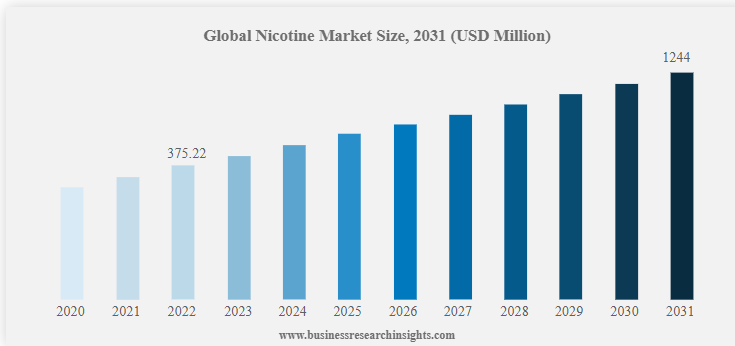

Business research insights

Global nicotine is a nearly $400 billion industry (about 0.35% of the global economy) growing at 13% annually.

By 2032, Business Research Insights thinks global nicotine will be a more than $1.2 trillion industry.

Before you get too excited about those forecasts, be aware that about 50% of those projected sales are in China, and China doesn’t allow foreign tobacco companies.

Outside of China, 4% to 5% is the growth rate of global nicotine.

How about the U.S.?

In 2021, U.S. nicotine sales were $85 billion, and by 2027, they are expected to reach $111 billion.

- 4.6% annually

- same rate as globally (outside of China).

OK, but that’s fantastic news for Altria; it’s not a dying industry, it’s a steadily growing one like alcohol.

No one worries that BUD is going bust anytime soon, so Altria needs to get through the transition to selling RRPs, and everything will be great!

But here is where things get a bit tricky for Altria.

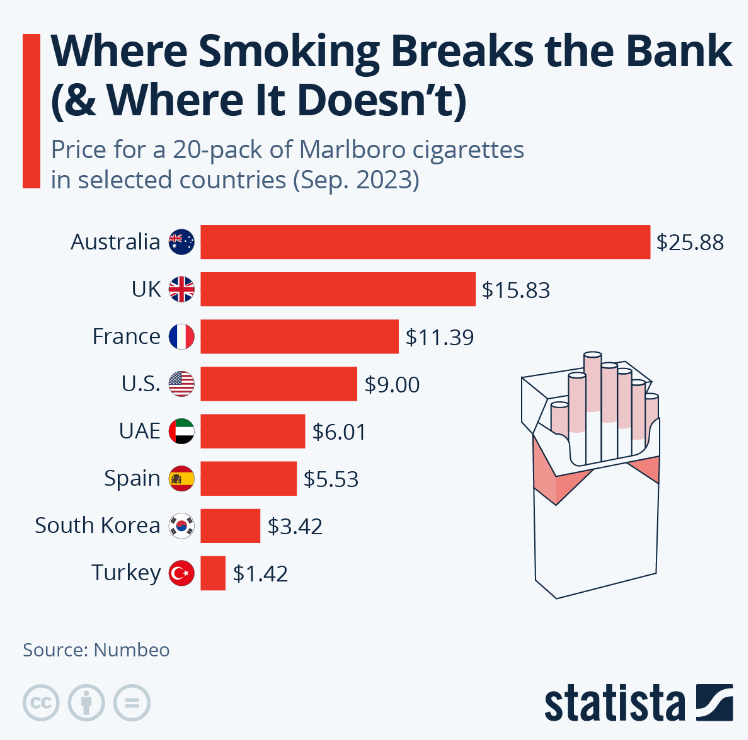

Cigarettes are expensive, averaging $9 per pack in the U.S. That’s the 4th most expensive country in the world.

Statista

Morningstar has been researching decline rates in various countries and estimates that U.S. tobacco companies have about 20 years before they won’t be able to raise prices enough to offset volume declines.

Altria is confident that 20 years is enough to pull a Philip Morris and get to a smoke-free future dividend growth streak intact.

Assuming, of course, that Morningstar’s model assumptions hold true.

Our base case is predicated on the assumption of a continued decline in cigarette volume at an annual rate of 5%, offset by continued strong pricing. The implication of this assumption is that the decline rate fades significantly from its current elevated level in the high-single digits and low-double digits in some recent quarters. We believe the decline rate will revert to a level closer to its historical mean when the ban on vaping flavors is effectively implemented and inflationary pressures on the consumer ease. The net effect is a five-year revenue compound annual growth rate of 1.5%, fading throughout our forecast period.” – Morningstar (emphasis added).

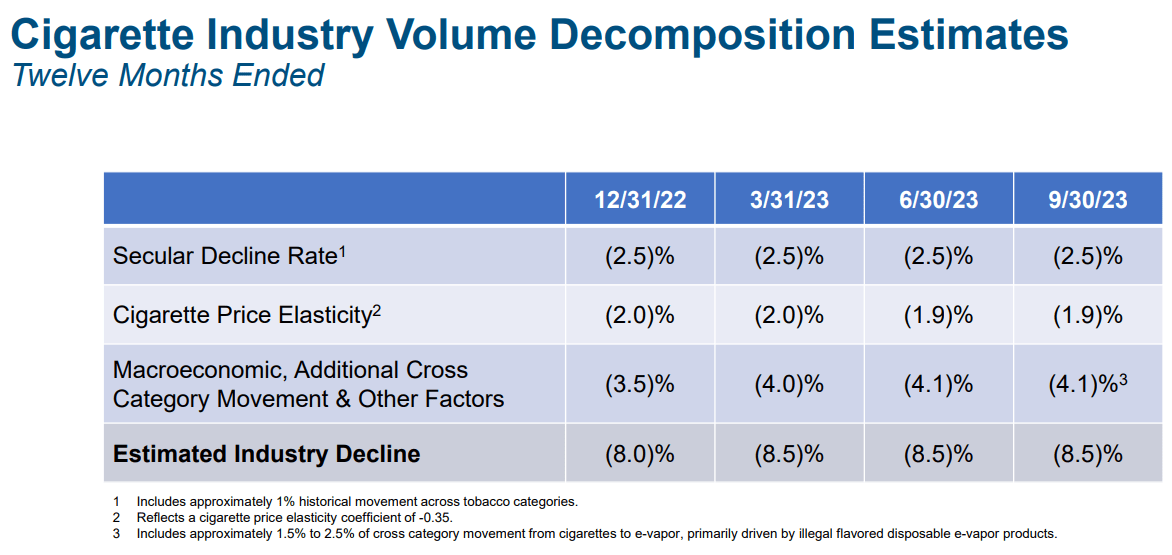

5% is the volume decline rate pre-pandemic and double that Altria uses in its model.

Altria

Note how, thanks to high inflation and cannibalization from RRPs, the industry’s decline rate has accelerated to 8.5%.

Altria

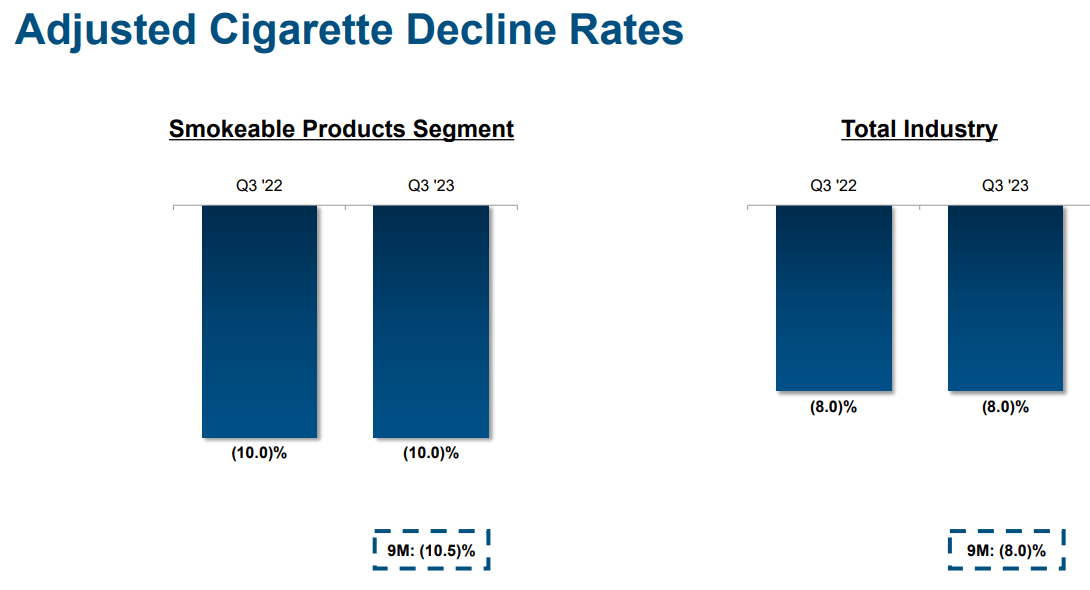

Altria, as a premium brand, has seen its volume decline rate accelerate to 10.5% YTD, the highest level ever.

Now, this is pretty scary, of course, because it led to something Altria hasn’t seen in decades.

Altria

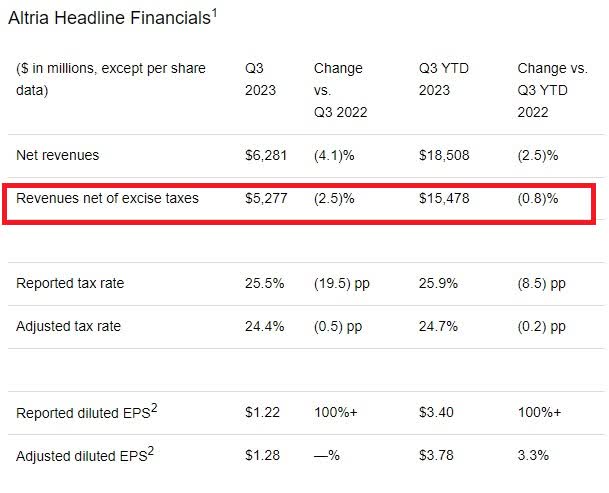

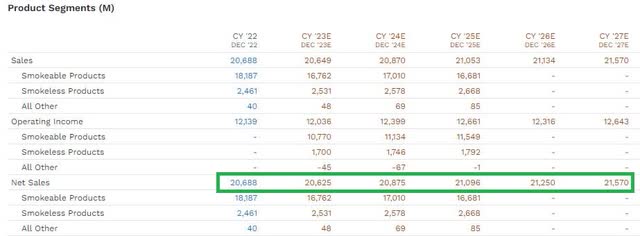

Altria is currently reporting a 1% decline in revenue for YTD.

How unusual is that?

Altria Never Has Negative Sales Growth

FAST Graphs, FactSet

Outside of 2007’s Kraft spinoff, Altria has consistently grown sales, or in the Pandemic, when supply chains were in chaos, reported flat sales.

FactSet Research

Through 2027, after a 0.3% sales decline in 2023, analysts (based on management’s new guidance) expect 0.8% sales growth through 2027.

Is that a lot lower than Morningstar’s 1.5%? Yes. Is it a heck of a lot lower than the 2.5% rate of the last 20 years? Sure.

Is it catastrophic? No.

Is it likely to happen? The bearish articles, like I referenced in the intro, say no, that the decline % will rise over time because the number of smokers left to pay MO’s premium prices is falling at a constant rate.

They sure look right in the short-term after three rough quarters.

However, here’s who disagrees with that argument.

- management

- 18 analysts who cover MO for a living and have the most advanced models of its business (developed over decades)

- credit rating agencies

- the bond market.

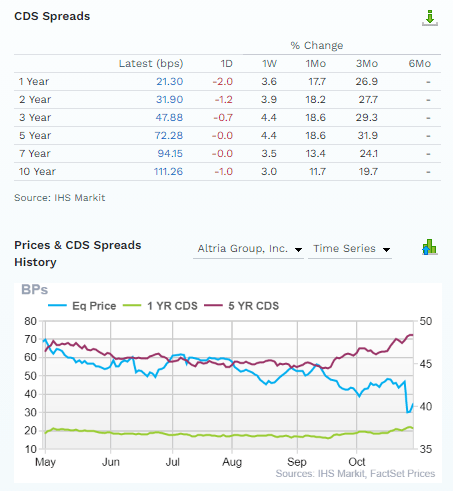

FactSet Research

The bond market agrees that MO’s fundamental risk is up after earnings. All of 3%.

In the last three months, the long-term risk is up 20%…to 1.1126% chance of bankruptcy within the next decade or 3.33% over the next 30 years.

- consistent with an A- credit rating.

S&P has MO as BBB with a positive outlook and a 33% chance of a rating upgrade within two years.

Could they all be wrong? Could the entire expert consensus, based on management guidance and their own internal Altria business models, be dead wrong, and the wheels are off the bus, and MO is headed to $32?

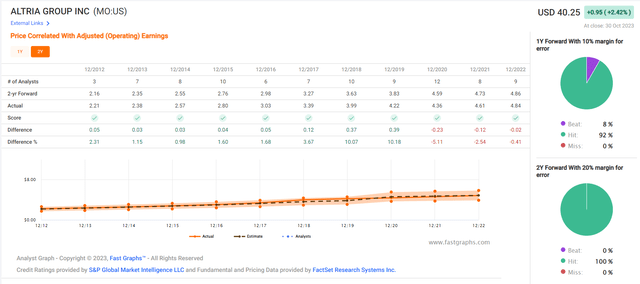

In the last 20 years, how often have one year earnings estimates missed by at least 10%? Never.

Fast Graphs, FactSet

How about 2-year forecasts missing by at least 20%? Never.

OK, but maybe MO missed every yearly forecast by 9%? Or every two years forecast by 19%?

Fast Graphs, FactSet

The biggest miss from MO in the last decade is a 5% earnings miss when its 2019 and 2020 EPS missed by 5% thanks to the Pandemic.

Other than that, this is a company with a stable business that management guidance and analyst models come within 1% or 2% of the final outcome…for 20 consecutive years.

So when someone tells you that management and analyst estimates are completely unreliable because this time is different? Be skeptical because they have no data to support their claims.

The Ugly: Altria’s RRP Portfolio Is Rather Weak

It doesn’t matter what MO does unless its making progress towards that smoke-free future that management says is the only salvation from steadily falling smoking rates.

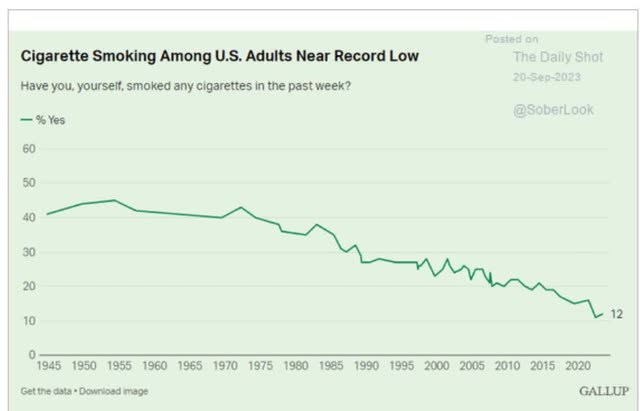

Daily Shot

The UK is considering effectively banning those of a certain age (14) from ever being able to start smoking legally.

Nothing so drastic has been proposed in the U.S., but the FDA is planning on eventually banning menthol, the #1 flavor of cigarettes.

British American estimates that the ban could go into effect as early as 2027.

The FDA doesn’t have the legal power to ban cigarettes, but it is planning to regulate the level of nicotine in cigarettes down to non-addictive levels.

It’s assumed that RRPs will be allowed to contain normal levels of nicotine, thus forcing smokers who want their nicotine fix to the lower cost and lower risk option.

The FDA has planned on a first draft of a proposal by May of 2023 but has yet to release it. The earliest such a ban might take effect is 2026, most likely after the menthol ban (2028 or later).

But it’s likely that by the end of this decade, the current nicotine landscape in the US will look very different.

Even if Altria had 10 to 20 years to milk its legacy cigarette business dry, the FDA might cut that to 10 years.

The State Of Altria’s RRP Transition

Altria

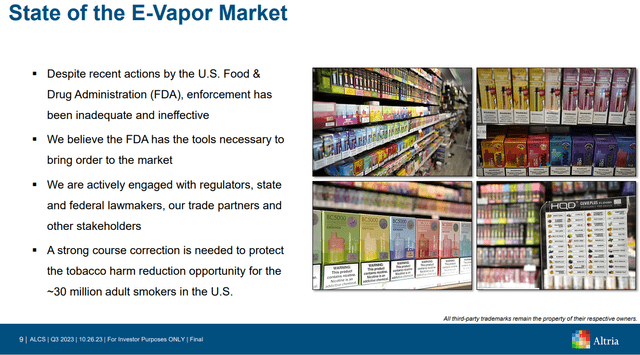

I wish management were not trying to make excuses or complain about how unfair the FDA is with its selective prosecution of the vaping industry.

Looking more broadly at the e-vapor category, the current state of the market is intolerable for both legitimate manufacturers and consumers. As we have noted repeatedly four months, the regulated market is being overrun by illegal flavored disposable e-vapor products made and distributed by companies violating virtually every rule and guidance FDA has issued since 2016. Regulation not enforced is indistinguishable from no regulation at all.” – Conference call.

Yes, it’s true that no vaping product is supposed to be legal without FDA approval. Pretty much everything in a vaping shop is illegal, but the FDA doesn’t care because it most likely thinks it’s preventing those younger people from switching to cigarettes.

What is Altria going to do in terms of vaping, heat sticks, and oral nicotine pouches? Let’s review the latest results.

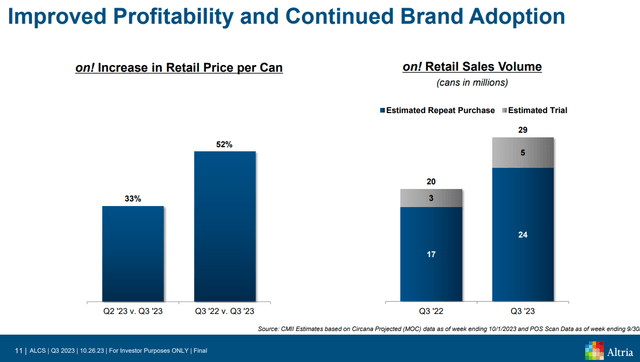

In the nicotine patch category, on! reported its first sequential volume decline, with a third-quarter volume of 28.7 million packs, down 4.3% over the second quarter but still up 36.7% year over year. Altria became less aggressive on pricing in the quarter, which will likely have a positive readthrough for Philip Morris International if Altria maintains that strategy.” – Morningstar.

MO is starting to experience some hiccups with on! The oral nicotine pouch that’s competing with Zyn (Philip Morris’s brand).

On! is still growing YOY, but for a new brand to experience a quarter of negative growth, even a modest one, is concerning. New product rollouts are easy to scale because you keep expanding distribution points.

Altria

The good news is that On!’s repeat rate is up from 65% to 83% in the last year, meaning 83% of people who try it buy it a second time.

Altria

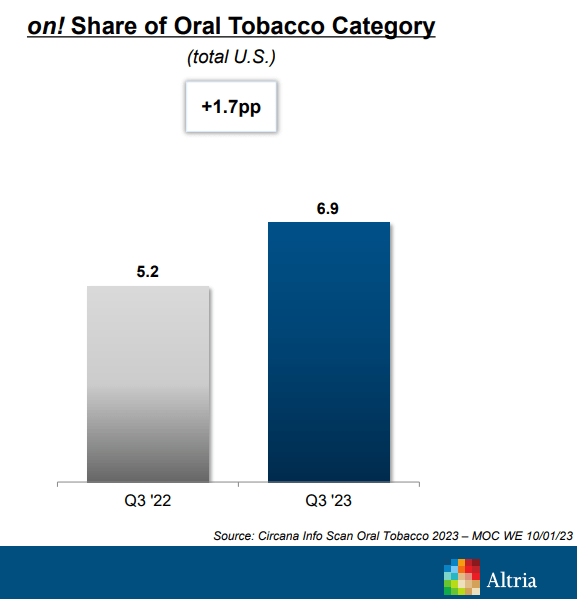

On! is gaining market share in oral tobacco. Remember, it competes not just with Zyn and Philip Morris but also its own brands like Copenhagen and Skoal.

Altria

Altria is planning different product lines to transition to a tobacco-free company.

MO plans a joint venture with Japan Tobacco in 2024 to launch heatsticks to compete with Philip Morris and iQos.

Eventually, it plans to try to create its own heatsticks, though that is likely a 2025 or 2026 plan.

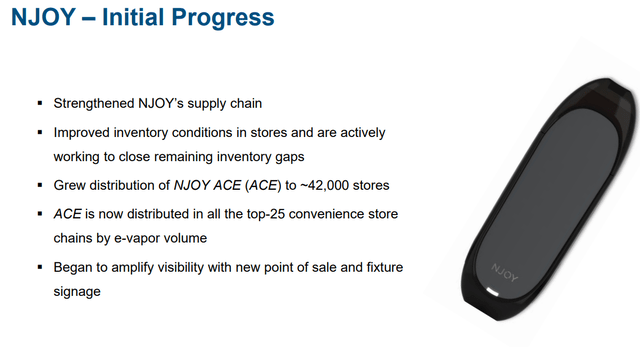

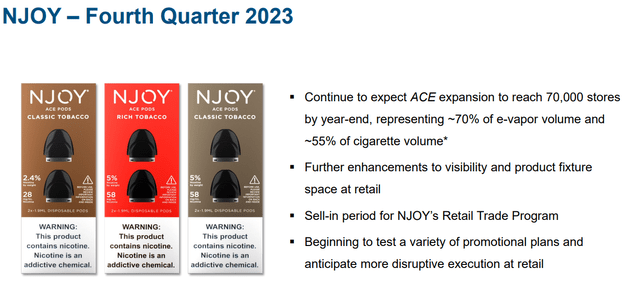

The biggest RRP platform it now has is NJOY, which it bought for $2.75 billion.

How big and bad a market player is NJOY?

I used to vape, and I had never heard of them.

Altria

The FDA has been at war with Juul for a while now, trying to ban it from shelves, and the same with BTI’s Vuse. Altria may have bought NJOY because it’s the only FDA-approved company, and thus, it thinks the government might finally start helping it in terms of vaping.

Altria

Altria is ramping out distribution for NJOY with big plans to make it the go-to vaping option. What kind of distribution channels does MO have?

Altria

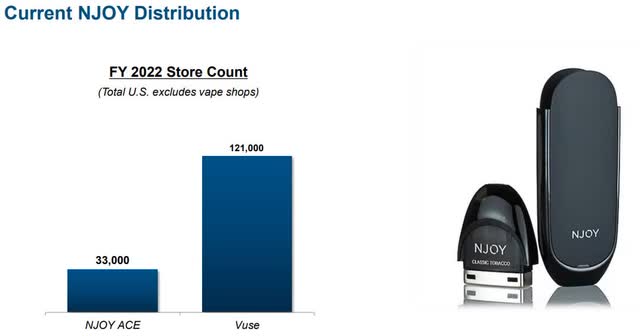

NJOY was in 33,000 stores when MO bought it and it expects to compete with Vuse.

In the last quarter its grown NJOY’s distribution channel by 9,000 stores.

- At this rate, 36,000 new stores within a year

- 109% YOY distribution sales growth.

Altria

MO’s actual plan calls for adding almost 40,000 stores within six months, which represents nearly 300% annualized distribution growth.

Altria

MO is rolling out a new marketing campaign in 2024 for NJOY, and if it gains traction, I’m sure we’ll hear about it.

When starting with a 3% market share, doubling that to 6% within a year by increasing distribution channels by 4X should be easily attainable.

If you don’t hear management talking about NJOY next year, it means they don’t feel they have anything to brag about.

Before the acquisition, NJOY had a small-scale salesforce, which resulted in inventory volatility and significant distribution gaps at retail. Upon completing the NJOY transaction, we immediately unleashed our salesforce to focus on closing the inventory gaps in stores that already had distribution. We improved store inventory conditions and are actively working to close the remaining gaps at retail.” – Conference call.

Right now, MO has all the vaping advantages it should theoretically need.

It owns the #1 vaping product the FDA is not trying to shut down.

It has some very easy growth capacity by just increasing store distribution by 300%.

NJOY was often capacity-constrained, and now its now.

MO has an extensive sales staff to promote it.

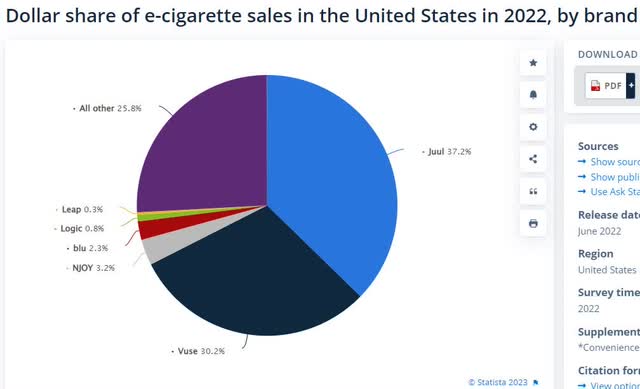

The most recent data, from March 2023, via the Nielson tobacco sales survey, showed NJOY to have a 3.7% market share.

- Juul 26.4%

- Vuse (BTI) 41%.

The Bottom Line: It’s The Best Time In 20 Years To Buy Altria

FAST Graphs, FactSet

Altria is trading at the lowest P/E since the Pandemic. The P/E is lower than in the Great Recession. You have to go back 20 years to 2003 to find it trading at anti-bubble valuations this good.

The Last Time Altria Was This Cheap: Pandemic

FAST Graphs, FactSet

In the Pandemic, investors paying 8X earnings for MO still enjoyed a 13% annualized total return even with the recent price crash and a bear market that just won’t quit.

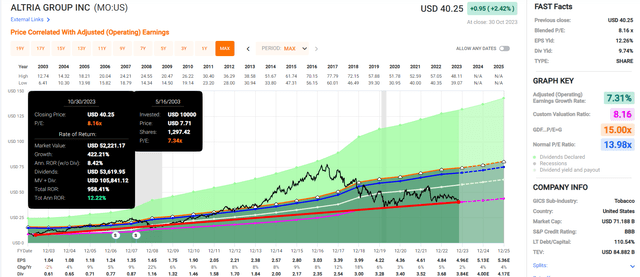

The Last Time Altria Was This Cheap: 2003

FAST Graphs, FactSet

If you buy MO at a sky-high yield like this, even modest growth and bear market pessimism aren’t going to stop you from earning a life-changing fortune over time.

If MO grows at 3.6% in the future, as analysts expect, and 5%, as management expects, then you’re looking at Nasdaq-like or better returns from here.

Despite all the struggles MO faces, the data is saying it’s an Ultra Value Buffett-style fat pitch right now, at the best P/E in 20 years.

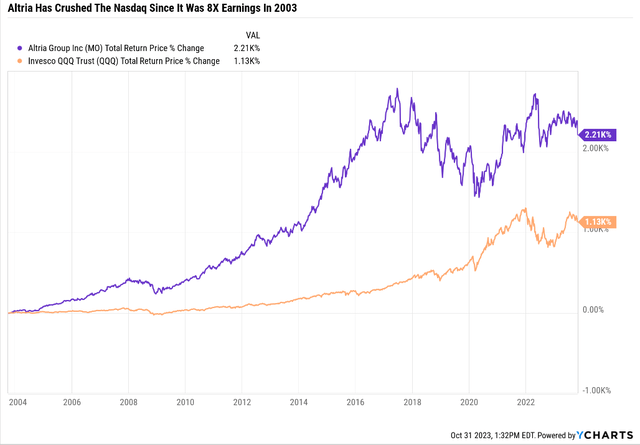

Ycharts

And just in case you think that you can’t beat the Nasdaq buying MO at a P/E of 8 over the long term, here’s the proof.

Read the full article here

2026-04-03")

")

")