")

")

Amylyx Pharmaceuticals, Inc. (NASDAQ:AMLX) is a biotechnology company based in Cambridge, Massachusetts. AMLX’s product AMX0035 is called Relyvrio in the US and Albrioza in Canada. This medication aims to treat neurodegenerative diseases such as ALS, PSP, and Wolfram syndrome, combating the death of motor neurons. AMLX’s public IPO was in January 2022. In September 2022, the FDA approved its AMX0035 drug for commercialization as ALS therapy while AMLX continues with the Phase III Phoenix clinical trials. Its results are expected in mid-2024. Approximately 3,900 patients are using the medication in the US, and the usage is expected to grow to 10,000 people at any given time. This, combined with AMLX’s inexpensive valuation, leads me to rate it a “strong buy” at these levels, as it appears simply too cheap to pass up.

Business Overview

Amylyx is a commercial-stage biotechnology company based in Cambridge, Massachusetts. AMLX works in reducing neuronal cell death and generates revenues mainly through its start product, Relyvrio. As such, this cutting-edge biotech company specializes in developing treatment options for patients with neurodegenerative diseases. The company was founded in 2013 by two undergraduate students at Brown University, proposing taurursodiol and sodium phenylbutyrate to safeguard neurons. They call the drug AMX0035. After they achieved satisfactory results, the ALS Association granted them $2.2 million to start clinical trials. Years later, in January 2022, AMLX had its IPO.

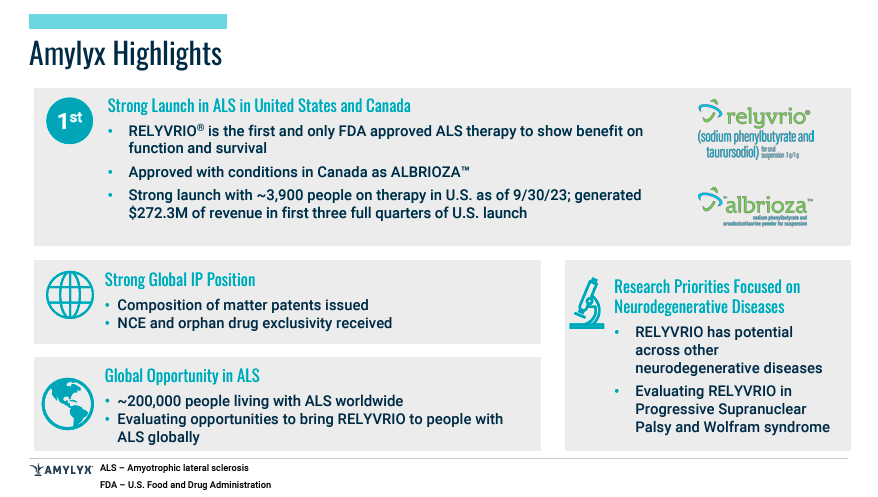

In September 2022, the FDA approved Relyvrio to treat patients with amyotrophic lateral sclerosis (ALS), formerly known as Lou Gehrig’s disease. This neurological disorder causes the death of the motor neurons that control voluntary muscle movement and breathing. ALS currently has no cure. The FDA granted Relyvrio a Priority Review and Orphan Drug designation to provide incentives to develop medicines for rare diseases. This allows this drug to be marketed based on this early effectiveness evidence and continue clinical trials to confirm the drug’s efficacy and safety.

Source: Amylyx Pharmaceuticals Corporate Presentation November 2023

AMX0035 and Neurodegenerative Disease Management

Relyvrio is an oral therapy, and its efficacy was demonstrated in the Centaur trial with 137 adult patients encompassing a 6-month randomized placebo-controlled phase and an open-label extension (OLE) long-term follow-up phase. The patients treated with Relyvrio experienced a slower decline in daily functioning and longer survival than those receiving a placebo. Accordingly, the European Medicines Agency [EMA] reviewed the marketing application for AMX0035 for ALS treatment and other neurodegenerative diseases. Yet, unfortunately, for AMLX, the EMA rejected the conditional approval due to concerns related to the Phase II results. Additionally, the Committee for Medicinal Products for Human Use ((CHMP)) of the EMA confirmed its initial negative opinion adopted in June 2023 for AMX0035 after a re-examination process. Although the silver lining is that if Phoenix’s results are satisfactory, AMLX plans to retry for approval in the EU.

Nevertheless, in Q1 2023, AMLX made the commercial launch of this drug under the name Relyvrio in the US and Albrioza in Canada for people with ALS. Relyvrio was initially priced below the latest FDA-approved product available to ALS patients, making it price competitive over its FDA-approved competitor, Radicava. In particular, this pricing move is noteworthy because it showcases the company’s genuine focus on delivering its cutting-edge research at competitive prices instead of price gauging desperate patients. In fact, AMLX also educates the public to drive awareness and help patients gain quick access to therapy, making it an overall driving force to help those affected by ALS.

R&D Status and Prospects

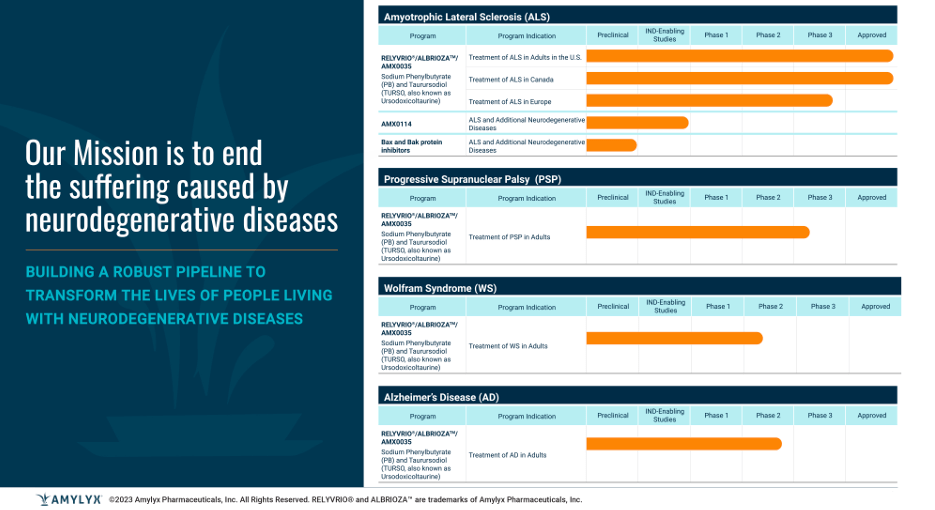

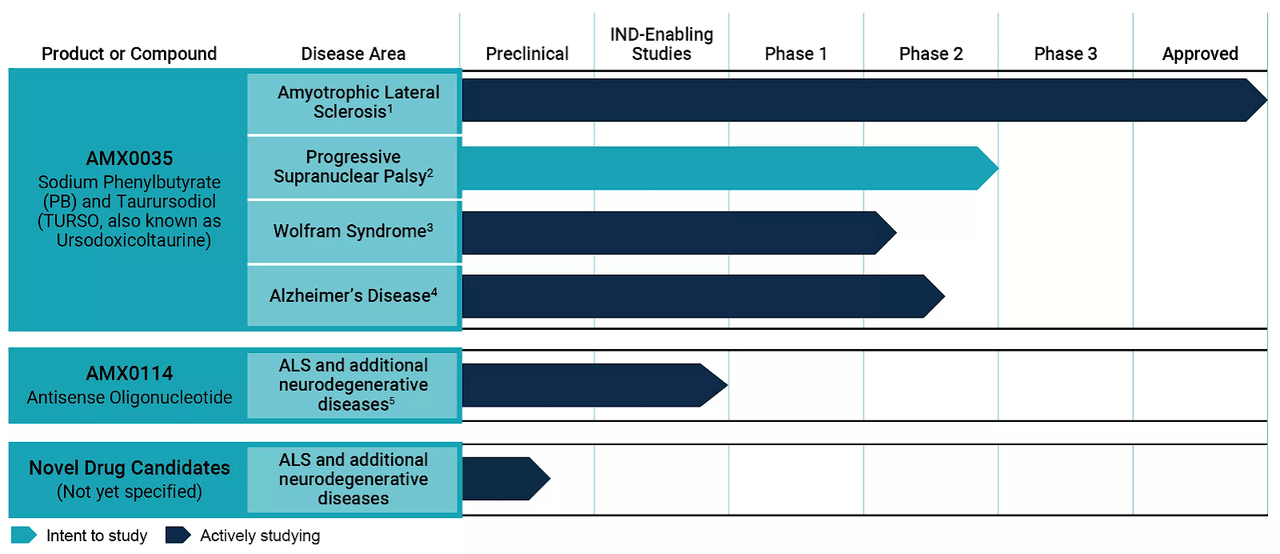

Currently, AMLX’s Phase III PHOENIX trial evaluates AMX0035’s safety and effectiveness. This study is underway at over 65 sites and 11 US and European countries, with results expected in mid-2024. In theory, after PHOENIX’s Phase III, EMA approval should get within grasp, making it a huge milestone for AMLX and ALS treatment. This is because PHOENIX is a broader clinical trial that tests Relyvrio’s overall efficacy, so it could potentially pave the way for Relyvrio’s future as a “gold standard” for ALS treatment.

Furthermore, AMLX is working in parallel with a phase III Orion clinical trial for AMX0035 to be initiated at the end of 2023 for Progressive Supranuclear Palsy (PSP) treatment. PSP is another neurological disease. The trial will enroll 600 patients from the US, Europe, and Japan to evaluate the efficacy and safety of the drug compared to placebo. AMLX is also researching the application of AMX0035 for Wolfram syndrome, a rare genetic condition that produces Diabetes Insipidus, Diabetes Mellitus, Optic Atrophy, and Deafness. AMLX expects results for the Phase II clinical trial in Wolfram syndrome in 2024. AMLX is also developing a new taste formulation of Relyvrio, planning to achieve in 2024 the IND filing and Phase 1 testing.

Source: Amylyx Pharmaceuticals Corporate Presentation November 2023

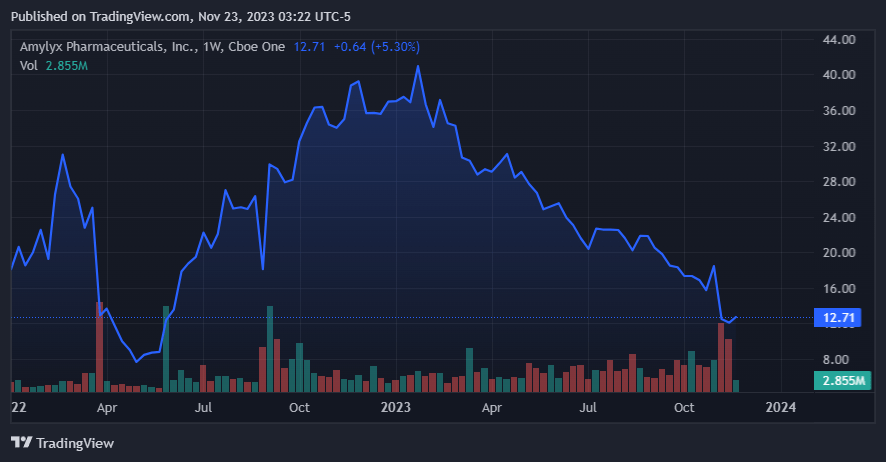

Interestingly, during AMLX’s latest Q3 2023 earnings call, executives commented about Relyvrio’s performance, highlighting that approximately 3,900 patients were using the medication in the US, and the company plans to extend it to other medical centers. AMLX expects Relyvrio’s usage to be expanded to at least 10,000 patients at any given time. This would be a 156.4% increase over the current use rate and should provide a favorable repeat revenue tailwind for AMLX for years to come. Additionally, this drug has generated $102.7 million in net product revenues for the quarter and $272.3 million since its launch in late 2022. Also, AMLX reported a net income of $20.9 million, marking its third consecutive quarter of profitability. Unfortunately, this was a notable 28.6% EPS miss, which caused the shares to drop from approximately $18.00 per share to the current $12.71 price tag.

Valuation Analysis

From a valuation analysis perspective, it’s vital to consider its product pipeline. It’s relatively focused on AMX0035, of which Relyvrio is the star product. Fortunately, for AMLX, this drug’s recommended treatment regime is one daily dose for the first three weeks, followed by an ostensibly indefinite two daily doses after that. Such doses can be orally administered via a feeding tube, which makes Relyvrio even more accessible to its patient demographic. Thus, AMLX’s revenue profile should consistently trend higher for the following years as Relyvrio’s acceptance increases and its treatment becomes part of patients’ daily lives with ALS.

Source: AMLX’s website.

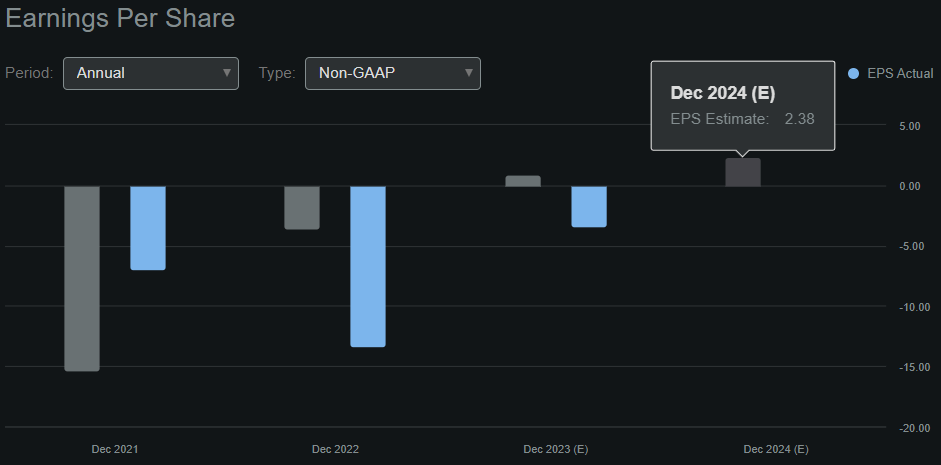

As a result, it’s no surprise that in 2022, AMLX’s revenues were $22.23 million, but by 2024, analysts expect they’ll reach $540.16 million. This implies an outstanding revenue CAGR of 392.94%, which should taper down as time passes. Nevertheless, I think it’s evident that AMLX’s revenue potential is indeed promising, and this doesn’t include the potential revenues from future additional verticals like AMX0014 and variations on AMX0035.

Naturally, as investors, we need to look at the numbers because no matter how good the company is, it’s not worth an infinite price. Therefore, one glaring drawback of AMLX is its current unprofitability despite the spectacular revenue growth it’s shown so far. Still, analysts forecast that by 2024, AMLX should yield roughly $2.38 in full-year EPS. That means the current PPS of $12.71 is trading at a forward P/E ratio of 5.34. This, by itself, is an unbelievably cheap valuation in general. Still, it signals clear undervaluation after layering on top of AMLX’s promising prospects and potential within ALS and related neurodegenerative diseases. For context, the sector’s corresponding median P/E ratio is 18.29, corroborating its largely misappreciated valuation profile.

Seeking Alpha.

Moreover, it’s worth mentioning that on top of its seemingly compelling valuation, AMLX’s balance sheet is also quite liquid. Currently, AMLX holds $355.0 million in cash and just $4.8 million in debt. This means that the company’s net cash position is approximately $350.2 million, so at the current valuation of $853.4 million, roughly 41.0% of the price you pay for AMLX today is cash. Lastly, given its robust cash position, AMLX’s enterprise value is approximately $503.2 million, and using 2024’s projected revenues, that would imply a forward EV/Sales ratio of 0.93, making it inherently cheap. But when you compare that figure to the sector’s forward EV/Sales multiple of 3.22, it becomes clear that AMLX is massively undervalued. I see no logical reason for such a significant undervaluation for AMLX, and hence, I think from a numbers perspective, the stock is a “strong buy.”

Risks to the Investment Thesis

Nevertheless, as optimistic as I am about AMLX, it’s important to note that it’s not without risks. In particular, it’s important to consider that the EMA’s initial rejection of AMX0035 was a significant setback. Moreover, this specific reticence to the company’s research could signal an underlying issue with the treatment, throwing a shadow of doubt over its long-term prospects of wider adoption and revenue growth. Naturally, this embodiment of the quintessential risk related to biotech stocks was undoubtedly brought to the fore due to this notable European rejection.

Additionally, AMLX is dependent on revenues from a single research, Relyvrio. While this is a phenomenal product and can bring many repeat revenues over the coming years, AMLX’s reliance on a single product exposes its business to higher-than-average risks. Furthermore, there are important manufacturing and supply chain risks to ensure the consistent quality and supply of Relyvrio. Given the company’s relatively strong cash reserves and impressive track record, shareholders are in good hands. Yet, it’s a set of risks that we can’t brush aside easily as investors.

Finally, AMLX has historically been over-reliant on shareholder dilution to fund its operations. Notably, since 2019, the weighted average of its diluted shares increased alarmingly fast from 5.9 million to 69.0 million in the latest report. I don’t think this rate of shareholder dilution will continue, and the robust cash reserves support this. Still, it’s nonetheless a trait of biotech companies, particularly one source of financing that AMLX has often frequented in the past.

The current pullback and its promising long-term prospects could prove a rewarding price entry for new shareholders. (TradingView.)

Conclusion

Overall, it’s difficult not to be bullish on AMLX’s prospects. Its product pipeline is undoubtedly promising and trades at a glaring misjudged valuation. Furthermore, I rate its revenues as high quality and likely yield relatively consistent income for shareholders over the coming years. This, coupled with AMLX’s strong cash reserves, positions the company perfectly for success or potential M&A transactions that can quickly unlock shareholder value. While it’s true that the latest earnings report came below expectations, AMLX remains, as a whole, on track to deliver compelling returns and trades at a low price. Hence, I believe it’s worth a “strong-buy” rating at this level, and I remain optimistic about its long-term future.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")