(NASDAQ:MU)")

")

")

Dear readers/followers,

It’s a good time to update on some of the Asian companies that I follow and invest in. One of those companies is Canon (OTCPK:CAJPY). It’s a good time to look because while the company had a bout of short-term outperformance since my last article, it has since dropped back down to bare outperformance of the broader S&P500, putting me into a position of probably expanding my position in the business.

I believe that Canon continues to be underestimated by investors. This is a Japanese quality tech company with a credit rating of A and a yield of now over 4%. Even conservatively speaking, the upside here is double digits, and in this article, I’ll try to show you clearly why I consider this to be a main investment into the Japanese market that you can make.

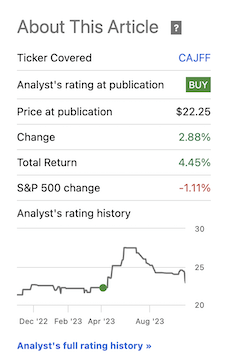

Look at how the company moved since my last bullish article.

Seeking Alpha Canon Article (Seeking Alpha)

This is a fairly interesting trend – and in this article, I’ll show you the results of 2Q23 and where we can go from here.

Canon – 2 good years of growth, let’s look at the third

After troughing in 2020 in conjunction with COVID-19, the company has recovered with a vengeance. The native ticker for Canon is 7751, and this is the one that I invest in. Fundamentally speaking, Canon is one of the most impressive companies on the Japanese market that you can invest your money in. I’m talking about a sub-3% debt ratio for an A-rated, 3.6T yen company. That alone, not even mentioning 4%+ yield, should be enough for the more conservative investors of you to stop and pay attention to this business.

The case for Canon is a fairly straightforward one, at least if we “uncomplicate it”. Canon is a market leader in several relevant markets. On the opposite side, we have geopolitical macro, inflation, supply chain, and other instability issues, which Canon really cannot influence or do anything about. The last quarter, meaning 1Q23 and 2Q23, were absolutely stellar, continuing the streak of outperformance we’ve seen.

How was 3Q23?

As you might expect by share price results, and given that we saw these results less than 3 days ago, the results were…so-so.

We’re talking about a sales and profit increase – in fact, everything was up. But I wasn’t up as much as the company expected. It was the first sign of what we can call comparative weakness in relation to forward expectations.

Why was this?

Because China’s demand softened, as well as some other regions seeing increased competition.

It’s important to note though, that results were in no way bad.

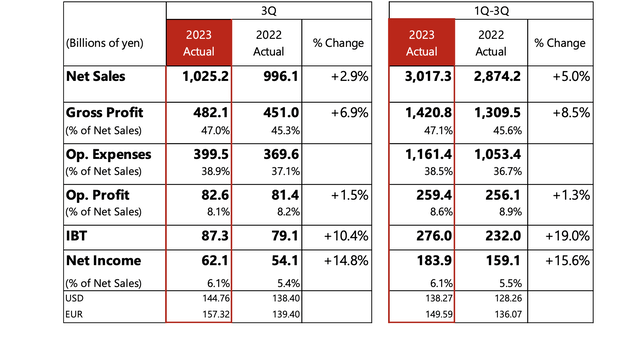

Canon IR (Canon IR)

Aside from China, Canon describes an overall effect from the downturn in real estate, ongoing monetary tightening that’s leading to ongoing weak demand in other regions as well – both for printers and for other products, leading to the company officially not reaching its plan in certain segments.

Not all things were bad though – the company saw growth in network cameras, medical, and other businesses. Also, a tailwind from favorable FX thanks to similar trends seen in virtually all Yen-based companies, resulted in YoY sales growth. However, much like with other Yen-based companies, investors of course understand that the effect here is likely momentary until the FX reverses.

Operating profit, as you see above, actually grew thanks to cost reduction effects, and FX – Canon actually continued to invest heavily in the promotion to increase sales, also incurring D&A due to sensor production startups at a new factory.

Canon IR (Canon IR)

For 9M23, because we’re moving into the end of the fiscal now, the company has posted a 5% increase in total operating profit, but a total net income increase of over 15%.

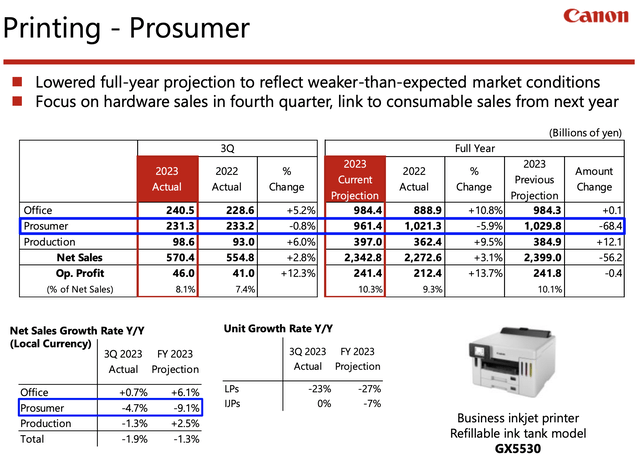

The company, despite the mentioned challenges, still expects a 400B+ Yen operating profit level. This was last achieved before the economies crashed in -08, which can be thought of as being quite foreboding. The company is lowering its projection in sales here, now expecting 4.2T Yen in sales for the full year, compared to around 4.36T Yen during the last set of forecasts.

Housekeeping or fundamentals for a company with A-rated credit and less than 2.9% long-term debt/cap is more of an exercise than in positive numbers than anything else. Canon has an interest coverage ratio of 200x, which might be the best among most A-rated companies out there. The company continues to manage a 46%+ gross profit margin and is stable at between 6-8% net margin. It’s not the greatest, but it’s certainly above average for the sector, the sector, in this case, being hardware.

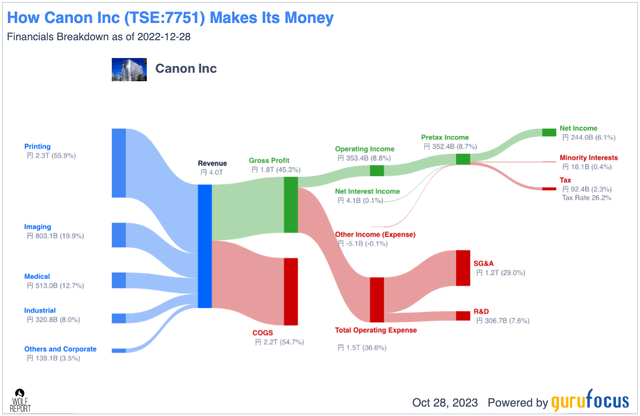

The company’s business model, despite the ongoing macro, is a joy to behold, seeing revenue turn into good amounts of net profit/income without more than 55% COGS and 37% of other operating expenses.

Canon Business Model (GuruFocus)

The company remains inherently impressively profitable. The little amount of debt it has actually wasn’t even there until 2016, and the company has been slowly cutting this back down ever since taking it on.

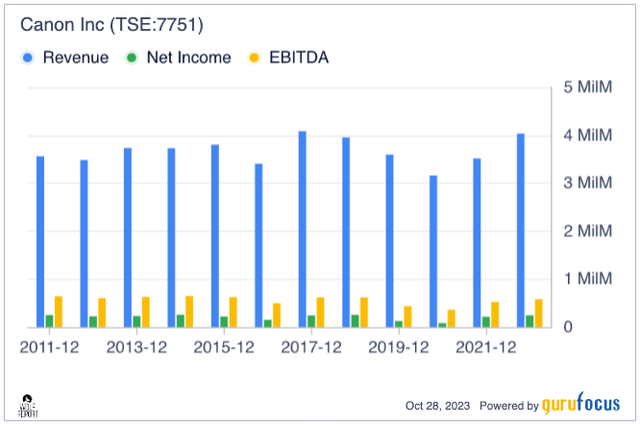

The one thing that can be said about Canon is the same thing that can be said about many Japanese companies for the past decade – a fair bit of stagnation. As investors, we tend to want growth in most fundamental KPIs. The company has not really been able to deliver impressive amounts of it.

Canon revenue/net (GuruFocus)

Since 2017, very little has happened. The company has been buying back fairly impressive amounts of shares, lowering SO, and SE has been rising as a product of this, which is good. Optimization of the company structure and shareholder equity is never a bad thing as such – but straight-line sales and profit growth would of course be better.

Where I believe Canon shines is really fundamentals and reversal potential, because this is something I see for the company. I believe that even under non-premiumized forecasts, this company has the potential to outperform the market – and this is always what I look for in many investments.

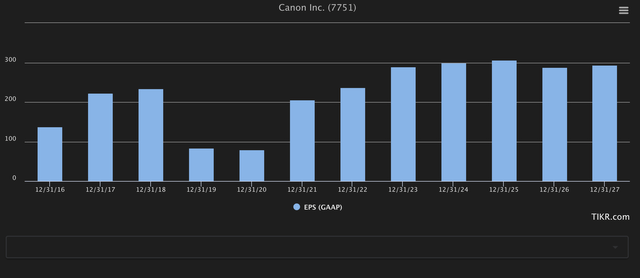

While expectations are for earnings to essentially “peter out” in terms of growth, that’s not yet where we are. In 2023E and 2024E, we still have growth estimates, and if these materialize (which I believe they will), then this company could still offer significant value as an investment.

Canon EPS estimates (TIKR.com)

Canon has a lot to offer those of us who want international diversification and attractive businesses with a good yield – and we can, I believe, still pick this company up at a good value.

Let me show you what I mean.

Canon Valuation – Still a 15%+ annualized upside on a 15x P/E with strong growth estimates.

The company continues to outperform the market, as it has since I started my investment in Canon. I was tempted when the company briefly touched close to the native 3,800 Yen level to divest part of my holding but ultimately decided against it. I do not regret this here (small movements, which is what I see this as being, don’t dictate my investment strategy – but I am never opposed to taking appealing profits if other investment possibilities are available. And today we have a lot of options).

Canon trades at an average P/E of 12.2x normalized here for the native 7751 ticker. This is below its premium of 17x, and it’s below a fair value of 15x given the company’s 4-6% growth rate and the current estimate of a 23% 2023E growth rate with a 291 Yen EPS estimate for the year (Source: S&P Global).

My target is 3,500 Yen, and I’m sticking to this target, meaning that the company is still a “BUY” here. On a forward estimate, meaning for 2025E, I expect it to be entirely possible for the company to reach a 15x P/E even with the current macro, and this would imply somewhere along the line of 4,500 Yen per share if the company’s 2023 and 2024 growth estimates materialize. That would also imply an annualized rate of return of 18.48%, which is above my minimum of 15%.

I view Canon as one of several diversification options for the Japanese market. Some choose to go the NIKKEI ETF route, and some Japan ETFs that focus on a broader diversification. As with all of my investments, I have not gone the ETF route (I do not own a single ETF in my portfolio), but rather choose individual investments that do not come with management fees and where I can “build” my own “fund”.

I believe Canon is safe enough and appealing enough at this price to hold through thick and thin in a market that seems dead-set on being volatile for the near term and possibly longer, given the risk of a serious downturn or a recession in 2024E.

I hold the stance that a soft landing is unlikely to the point of being unrealistic, which is also why I’ve included far more defensive investments and also hold a 10%+ cash allocation at this time, which is very unusual for my approach. I’m usually more than 95% invested at all times.

This isn’t perhaps the most undervalued or the most appealing investment on the entire market. That is not what I am saying. But it is an investment that you can buy, and one that I believe in the long term will outperform a 15% average.

For that reason, I’m at a “BUY” here, and may add more shares now that we’re in decline after 3Q23 results.

Thesis

My thesis for Canon is as follows:

- Canon is one of the premier imaging, camera, and printing companies on the planet. It has a solid foundation as well as excellent growth prospects. At the right valuation, this company goes from being a possible buy to being a very compelling prospect for long-term investing.

- At a conservative 12-13x P/E, I not only consider the company somewhat attractive but a definite “Buy”. I’ve established a starter position – my first position in a native Japanese ticker.

- I follow Canon with a $24.5 ADR price target or 3,500Y for the native Tokyo ticker. It’s closing on my PT, but it’s still a “BUY” here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This company fulfills all of my valuation criteria for investing except being cheap – it’s therefore a “Buy” here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

(NASDAQ:MU)")

")

2026-04-03")

")