")

Q4 2025 Earnings Call Transcript")

")

Introduction

One company that I have been buying this year is Charles Schwab (NYSE:SCHW). I followed the stock, believing it was an excellent long-term opportunity when I acquired it this year. The company is a leading financial institution, and as a client who enjoys its services, I did a deeper dive before I became an investor. The financial sector is interesting, and Charles Schwab in particular.

The current interest rate benefits banks as the spread between rates on deposits and loans grows. However, some banks also have significant investment businesses. Charles Schwab is one of them, and it may suffer from higher rates and declining markets. Therefore, a deeper analysis is required to determine whether shares are still attractive. I’d seek to find short-term risks with long-term growth opportunities to justify the investment.

Seeking Alpha’s company overview shows that:

The Charles Schwab Corporation and its subsidiaries operate as a savings and loan holding company that provides wealth management, securities brokerage, banking, asset management, custody, and financial advisory services. The company operates in two segments: Investor Services and Advisor Services. It offers brokerage accounts, full-time portfolio management, banking products, and more. It also provides digital retirement calculators, integrated web-, mobile-, and software-based trading platforms, real-time market data, options trading, premium research, and multi-channel access. The Company operates domestically and in the United Kingdom, Hong Kong, and Singapore.

Fundamentals

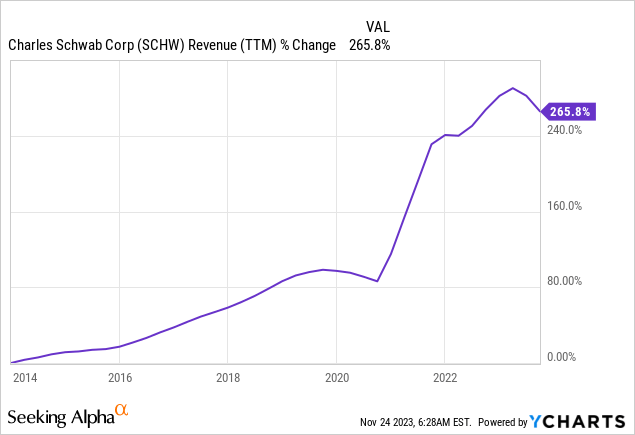

Charles Schwab’s revenues have dramatically increased over the last decade, with a 266% increase. The sales increase can be attributed to a combination of organic growth and acquisitions. Schwab has combined major acquisitions like the TD Ameritrade acquisition for $26B, which increased scales, with smaller acquisitions allowing it to expand and widen its value proposition. In the future, as seen on Seeking Alpha, the analyst consensus expects Charles Schwab to see an 8% decline in sales in 2023, followed by a 10% annual growth rate in 2024 and 2025.

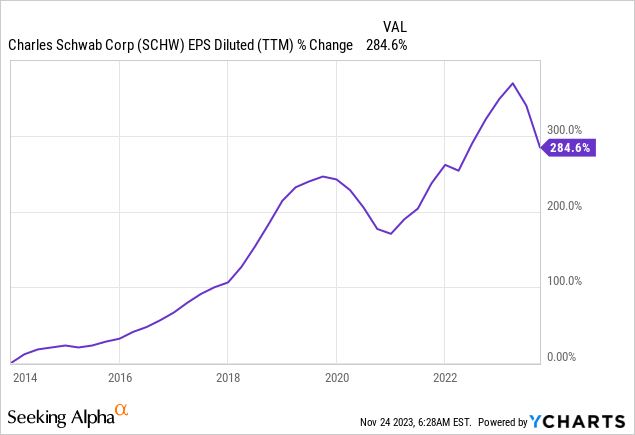

The company’s EPS (earnings per share) increased even faster. The EPS increased 285% over the last decade, and it did it despite an increase in the number of outstanding shares. The reason for that is the improved margins that the company achieved as it increased its scale and kept the expenses in check. As we advance, as seen on Seeking Alpha, the analyst consensus expects Charles Schwab to keep growing EPS at an annual rate of ~20% in 2024 and 2025, following this weak 2023 that is expected to see an 18% EPS decline.

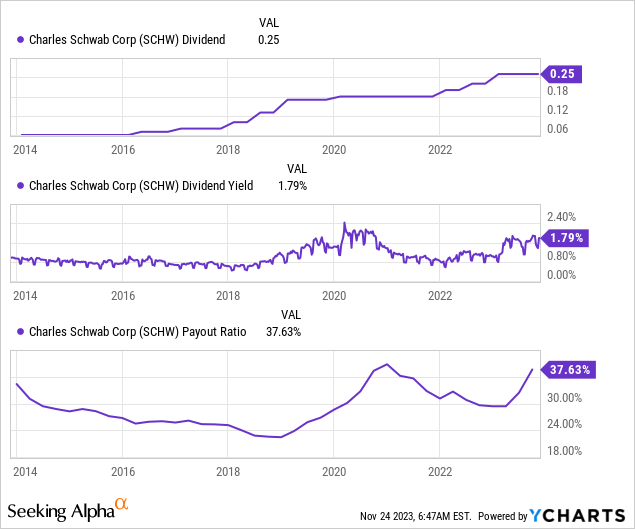

The company is a highly reliable dividend payer. It has not reduced the dividend for more than thirty years, and despite a stagnated dividend during the pandemic, it has shown a long-term commitment to dividend increases. The company offers a 1.8% yield, which is likely safe as the payout ratio stands below 40%.

In the short term, I believe that dividend growth will be maintained at a high-single-digit rate despite higher forecasted EPS growth. I believe that the company needs to see a more stable business environment before increasing the dividend at the EPS increase rate. Moreover, I believe that its regulator, the Federal Reserve, will not allow significant dividend increases until the balance sheet is secured. Higher rates press the value of assets on the balance sheet. Therefore, as interest rates climb, the company should focus on it.

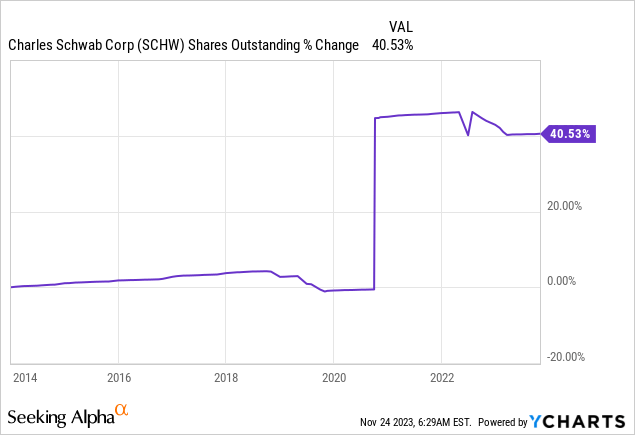

In addition to dividends, companies, including Charles Schwab, return capital to shareholders via buybacks. These buybacks support EPS growth as they reduce the number of shares. Over the last decade, the company has seen a 40% growth in the number of shares. This is the result of the TD Ameritrade acquisition. Since then, the company has announced a $15B buyback plan, and I hope the management will capitalize on the attractive valuation. However, it is uncertain as, in challenging times, banks tend to be forced to maintain high liquidity.

Valuation

The P/E (price to earnings) ratio stands at 17.65 when using the EPS forecasts for 2023. This is almost the lowest valuation we have seen for Schwab over the last twelve months. As interest rates climbed and the expectations changed, it was apparent that the 2023 EPS would decline. Thus, the valuation has also declined. However, the valuation fell significantly from a P/E ratio over 25 to 17.65, which I believe presents a decent entry point. The company is still more expensive than its peers, but its future is also brighter. None of its main peers expect 20%+ EPS growth in 2024 and 2025. Therefore, I believe this premium is justified.

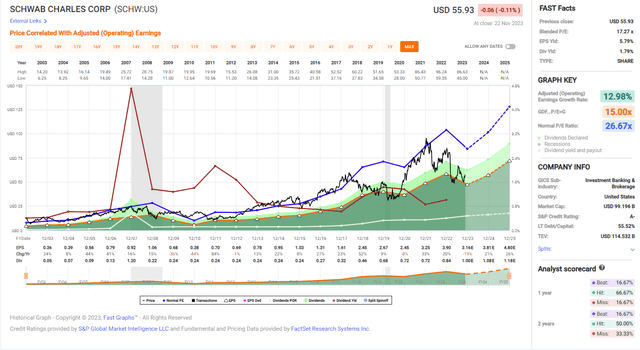

The graph below from FAST Graphs also emphasizes that the shares are attractively valued. The company is trading for a P/E ratio of 17, which is significantly lower than the average P/E ratio over the last two decades, which stood at 26.7. When looking at the growth rate, the picture is even more promising. The company grew at a CAGR of 13% over the last two decades, and following the decline in 2023, which is already priced in the P/E ratio, investors should expect more than a 20% annual growth rate for several years.

FAST Graphs

Opportunities

Charles Schwab’s successful integration of TD Ameritrade presents a significant growth opportunity. The combination of two leading brokerages emphasizes the meticulous “best of both” integration approach, leading to high client satisfaction. The company now has an extensive value proposition offering attractive prices, vast data and research, and excellent customer support. The completion of three out of five transition groups with a remarkable speed of service, averaging less than one minute to answer client phone calls, showcases the efficiency of the integration. The company is enjoying a high retention level from former Ameritrade retail clients, even better than expected.

“Former Ameritrade retail clients are rewarding us with levels of loyalty and retention that are far better than we anticipated when we announced the acquisition back in 2019.”

(Walter Bettinger, Co-Chairman and CEO, October 2023)

Another growth opportunity is the growing demand for wealth management services, particularly in the advisory space. Schwab’s strategic focus on providing advice has led to record highs in managed investing flows, with Schwab Wealth Advisory experiencing a record $9.2 billion in net flows year-to-date. The company sees a “bull market for advice.” It emphasizes the potential benefits of direct indexing, which has seen a record $4.5 billion in net flows year-to-date for the Wasmer Schroeder.

“With the investments we’ve made and continue to make, more and more of our retail clients are turning to us for wealth management as they move into a life phase where they need advice.”

(Rick Wurster, President, October 2023)

The Workplace business, catering to individuals investing through their employers, offers a strategic growth avenue. The company highlights its role in introducing millions of participants to Schwab, with 1 in 3 new-to-firm households originating through the Workplace business. The focus on upgrading digital experiences and technology investments in this area aims to fuel net new asset growth for Schwab into the future, presenting a straightforward “grow, retain, and extend” approach. Schwab will benefit from the growth of their retirement account and the individual account that will follow, and hopefully, it will be upgraded to an advisory account.

“With Workplace, we can fuel net new assets growth for Schwab into the future through our grow, retain, and extend approach.”

(Rick Wurster, President, October 2023)

Risks

Schwab acknowledges the challenges posed by the Federal Reserve’s actions, impacting financial markets and investors. The rise in short-term and longer-term interest rates during the third quarter led to investor sentiment decline, with a shift towards cash investments. The potential negative impact on bond prices and market volatility presents a risk. Investors began to feel this pain as equity and fixed-income markets suffered, hurting the returns in Q3. Moreover, some investors were concerned about the health of Schwab itself as investors feared outflows.

“These actions are slowing the rate of inflation, but at a significant cost to the markets, consumers, investors, and firms like Schwab.”

(Walter Bettinger, Co-Chairman and CEO, October 2023)

Moreover, the company faces short-term financial performance challenges, with the third quarter showing a decline in revenue compared to the previous year. The company and analysis covering it see a decrease in sales in 2023. While successful, the ongoing integration efforts with TD Ameritrade may still pose challenges for clients during the adjustment period. The company expects to see a stabilization of revenue and a return of transactional cash growth in 2024 but acknowledges the influence of trading volumes and market levels.

“The more tactical balance sheet metrics have also trended in a positive direction. And we believe we are well on our way towards those indicators returning to more normal levels.”

(Peter Crawford, Managing Director and CFO, October 2023)

Lastly, the company has to deal with the challenge of expense management and the impact of the economic cycle. While Schwab expects to reduce expenses through the integration process and operational streamlining, there are uncertainties related to ongoing expense actions. The environment’s challenging nature is acknowledged, and expenses are expected to be roughly flat year-over-year, reflecting the need for disciplined cost management amidst ongoing investments. With fewer assets to manage due to possible market decline and struggle to lower costs, cost-cutting may take longer as the company waits for the business environment to be less foggy.

“Now admittedly, that powerful combination has been obscured recently by some of the fog as Walt described it back in July, but this fog continues to clear…”

(Peter Crawford, Managing Director and CFO, October 2023)

Conclusions

Charles Schwab is a well-managed blue-chip company and a solid financial institution. The company grows sales and EPS and delivers significant dividend increases and buybacks. The acquisitions and the organic growth allow the company to offer a comprehensive value proposition to a wide range of clients and grow in these verticals.

There are risks to the investment thesis as we are in a volatile business environment, and the market is still looking for direction. However, these are mainly short-term risks, and the company is well-positioned for long-term growth. Therefore, at the current valuation, I believe that the shares of Charles Schwab are a BUY.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")