")

")

Getting One Up On Wall Street

In the interest of continuing to practice and improve as an equity analyst, which I believe to be a lifelong endeavor, I’ve been re-reading Peter Lynch’s One Up On Wall Street recently. For the uninitiated, Mr. Lynch ran Fidelity’s famed Magellan Fund, which still operates to this day. As an illustration of the Magellen Fund’s preeminence in the annals of American equity investing, I recently tuned into CNBC for a bit (extremely rare for me), and the hosts were coincidentally discussing the composition of the $28B Magellan Fund’s holdings.

During Mr. Lynch’s tenure at the helm of the Magellan Fund, he generated 29% annualized returns from 1977 to 1990 when we stepped down from running the fund. $100k invested in the Magellan Fund when he assumed leadership became about $2.7M in just 13 years.

Notably, Mr. Lynch vastly outperformed investing greats like Warren Buffett through this period, and he was consistently in the top 1-2% of fund managers throughout his 13 years at the helm of the Magellan Fund.

With such an incredible track record, I believe it’s certainly worth employing Mr. Lynch’s perspective with respect to equity investing, and throughout my ownership of Chipotle, I have done just this with fantastic results.

Seeking Alpha

In One Up On Wall Street, which I believe you must read if you follow my research, Mr. Lynch recommends purchasing businesses that you, as an ordinary person living life totally detached from the cacophony of sound emanating from Wall Street, understand and with which you interact on a daily or routine basis.

He asserts that ordinary people have an advantage over professional analysts and professional money managers when these ordinary people buy what they know based on their own, unique experiences in their day-to-day lives. From the chemical engineer who can predict the price of a rare metal, and therefore predict the price of businesses selling that rare metal, to the barista who works for a young and rapidly growing coffee shop with lines out the door, Mr. Lynch contends in One Up On Wall Street that those with on the ground knowledge have substantial advantages against analysts and money managers making decisions from their Ivory Towers on Wall Street, where they’re, for the most part, largely detached from the realities of the businesses in which they’re investing or on which they’re opining.

In short, he recommends that, in order to be an exceptional, successful investor, you should take account of your daily life and determine which products and services you value most or which products and services you understand to the highest degree, and invest in those areas.

For instance, if you stood in line to purchase the first iPhone in the late 2000s, you should have also stood in line before the opening bell the next day to purchase shares of Apple (AAPL) stock.

If you currently find yourself on a three-year waitlist to purchase the revolutionary Cybertruck from Tesla, then you should probably be accumulating shares of Tesla (TSLA).

If your team at Smith Dynamics, LLC, which manufactures batteries, runs on a specific software platform; perhaps, Monday.com (MNDY), and it’s the most efficient and wonderful software you’ve ever used, then you should probably be using your brokerage account to purchase shares of Monday by next Monday.

If you shop on Shopee every day and pay with SeaMoney (SE); then get in a Grab (GRAB) to go out for dinner and drinks with your wife or husband or whomever, then these are likely investments you should deeply consider.

While Wall Street will not hesitate to try to sell you its opinion on Apple, Tesla, or Monday (even if you do not pay with cash, you pay with attention, which equals time, which equals cash), Mr. Lynch contended that your firsthand experience with the product or company in question was vastly more valuable than what the team of equity analysts could surmise from their “cells” (excel cells or office cells, you decide) locked away in high rises in Manhattan.

Of course, there’s a financial component to all of this, i.e., all businesses have two essential risks: Going concern risks (i.e., solvency; success of the product; will the company exist in 20 years?) and valuation risk (i.e., overpaying for a very high-quality business can be nearly or as disastrous ultimately as buying a company that goes bankrupt). So that should be noted, but, invariably, you will find exciting and profitable investments by simply surveying your surroundings, from your job to your kids’ favorite activities.

By now, you can likely connect the dots between Chipotle and my investing in it: I’ve been a vocal owner of Chipotle by virtue of my affinity for its food and loyalty to its brand. Excepting periods in which I served overseas with the U.S. army, I’ve eaten Chipotle almost every week for over 10 years. In fact, I ate it today.

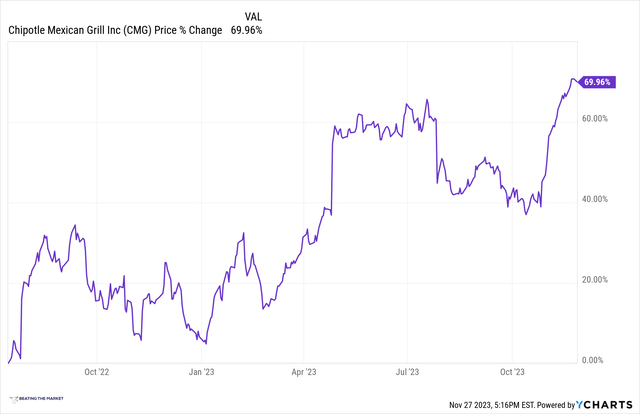

Chipotle’s Returns From Where Beating The Market Increased Its Rating To “10%” Indicating Its Risk/Return Was Highly Attractive In 2022

YCharts

One Up On Wall Street: Chipotle Edition

As you know by now, in One Up On Wall Street, Mr. Lynch advocated for using your firsthand experience to assess a business’ worthiness of your capital.

Throughout my ownership of Chipotle, I have employed this style of analysis to continue to confidently accumulate shares of the business over time.

Specifically, my analysis has considered Chipotle’s “taste-adjusted calorie/$” equation against the “taste-adjusted calorie/$” of its competitors, such as Chick-fil-A or Taco Bell or Burger King.

I’ve asked myself, “If I had to survive on one of these fast food restaurants, which would provide me the optimal quality of life through the lens of “taste-adjusted calorie/$”?”, and every time, I’ve come back with the same answer: Chipotle stands alone.

There is no other option that offers both the volume of nutritionally varied calories and a great taste.

Chick-fil-A tastes great, but I’m eating a bunch of fried food, and really not that much of it for more money than I pay at Chipotle, and the same could be said for Burger King (where I get very little nutritional variety) and Taco Bell.

In conducting this analysis for myself, I determined that human instinct alone would draw people to Chipotle, i.e., most folks wouldn’t even be able to describe why they loved Chipotle’s rice, beans, veggies, and grilled meats more than Wendy’s. They just would like it more. The reality, however, would be that this nutritionally varied, low-cost, high-volume food option was appealing to the very essence of their psyches: the tendency to choose the route or choice that optimizes for survival.

Yes, this may sound esoteric, but it’s hard to argue with Chipotle’s results: At just about 3k locations, it already does $10B in relatively high-margin annualized sales.

To close, this has been the style of analysis that has underpinned my ownership of Chipotle, and it has been entirely inspired by Mr. Lynch’s thinking in One Up On Wall Street.

Let’s now turn to a review of my more Wall Street-esque Chipotle investment thesis.

Four Pillars

Today, I will articulate my Chipotle thesis to you through four pillars:

- We will discuss my thesis for Chipotle as it has pertained to its margin structure.

- We will discuss the economic moats that Chipotle possesses that gave me confidence in the materialization of higher operating and free cash flow margins for Chipotle.

- We will discuss which of our four foundational investment frameworks is applicable to Chipotle.

- And, lastly, we will consider Chipotle’s valuation as of today, at $2,000/share+.

Notably, these are not randomly selected pillars idiosyncratic to Chipotle. They are definitive, repeatable applications of my core tools for investment, which I routinely share with my readers and community members.

There’s much to cover for just the four pillars so let’s begin!

Skating To Where The Puck Is Going; Not Where It Is

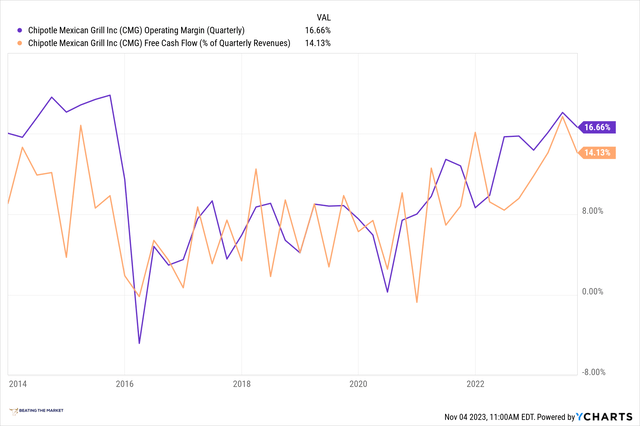

In a recent consideration of Intuitive Surgical, I explored my quantitative thesis for Chipotle over the last half decade or so, which has, to a large extent, revolved around the expansion of Chipotle’s operating and free cash flow margins.

We can see this expansion in the chart below.

Chipotle’s Operating And Free Cash Flow Margin

YCharts

“Skating to where the puck is going,” i.e., predicting the level to which margins will expand or compress, is a fantastic way to create exceptional returns.

However, before we start predicting margin expansion or compression, we must start by considering the company’s economic moats whereby we determine whether the company has the pricing power, unit economics, and business model that would afford it the ability to expand margins sufficiently.

Over the last 8 or so years, following the ecoli scare that caused Chipotle’s margins to totally collapse, investors have endlessly remarked that the business is too expensive. They have looked at the company’s PE ratio or P/FCF or EV/FCF ratio and said, “It’s too expensive for just 10-15% sales growth.” “40x earnings for a burrito shop?!”, they’ve excoriated.

But what these investors failed to realize was that fcf/share growth would be much, much, much higher than top-line sales growth as Chipotle’s operating and free cash flow margins expanded to the level at which they found themselves prior to the health scare in 2015.

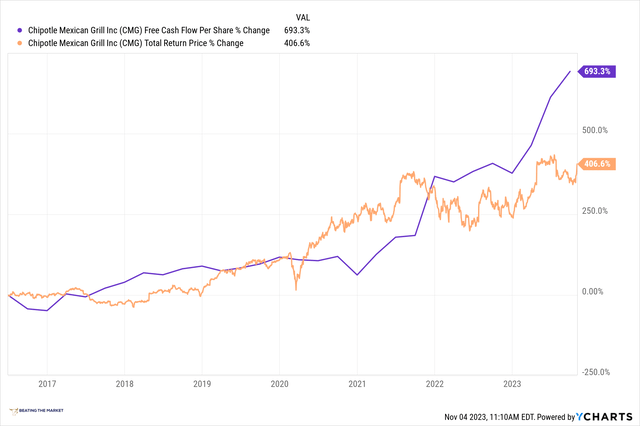

As Chipotle’s margins have expanded, the growth of free cash flow per share has been meteoric: nearly 700% in just the last eight years!

Chipotle’s Free Cash Flow Per Share Grows 693%, Bringing Its Share Price With It

YCharts

Investors that simply looked at Chipotle’s PE multiple and its revenue growth were, in essence, deceived: They couldn’t fully appreciate the rate at which Chipotle’s free cash flow per share was growing, which was something akin to a hypergrowth startup, as opposed to a 25-year-old burrito chain.

I recently articulated the importance of free cash flow per share as the foundational metric atop of which all equity value is built.

As I’ve shared in the past, the value of any business is:

- How much free cash flow per share it generates and how fast that free cash flow per share grows

- The durability, defensibility, and reliability of that free cash flow per share

- When that free cash flow will be received

- And our next best alternative (such as the 10-year treasury yield)

These four variables define the value of any enterprise through a purely quantitative lens.

Examining Axon’s Lucrative Software Business

Chipotle’s Economic Moats: Foundation For Margin Expansion

An economic moat is a distinct advantage a company has over its competitors which allows it to protect its market share and profitability.

[Profitability = free cash flow]

As I noted above, it can be a very lucrative investment strategy to predict the level to which margins will ultimately expand while the market hesitantly waits for the margins to actually expand with a “we will believe it when we see it” attitude.

In order to confidently and successfully identify whether margins will expand and the level to which they will expand, we must start with an analysis of a company’s unit economics and, as importantly, economic moats.

Four of the most prominent and ubiquitous economic moats are:

- Network Effects

- Embedding/Switching Costs

- Brand (arguably the best and most difficult to achieve)

- Economies of Scale

Let’s briefly assess Chipotle through each of these moats whereby we will determine the degree to which the business is competitively advantaged, and by extension the degree to which its cash flow margins are defensible.

- Network effects: Chipotle certainly does not possess network effects moats akin to Facebook (META), in which each additional user of Chipotle restaurants makes the entire network of restaurants more valuable in a profound way and at a massive, global scale. That said, there are light network effects here, which is an idea that is notable, i.e., network effects are not black and white: there are various shades of the moat and various degrees of the moat’s strength in defending and creating cash flows. In the case of Chipotle, there are some light network effects in that, as each additional member of a friend group or family begins to eat at Chipotle routinely, the value of the restaurant to the entire group increases, as now the group or family collectively have a place where they can eat unanimously. The same idea could apply to an office that routinely caters: as more and more employees “join the Chipotle network,” if you will, the value of Chipotle increases because it is a commonly enjoyed catering choice. Admittedly, again, this is not the primary moat for Chipotle.

- Embedding/Switching Costs: Chipotle also has a relatively weak embedding/switching costs moat, though its digital strategy in which users of its app collect rewards points creates some element of embedding/switching costs. Additionally, Chipotle’s presence in a community is, in a sense, an embedding moat.

- Brand: As of today, Chipotle’s brand moat is indisputably its largest moat. Its brand has become synonymous with the category of cuisine it has created. This category is defined by the “fast casual” format that is emblematic of Chipotle restaurants. For instance, CAVA (CAVA) recently went public, and the easy way to describe the restaurant concept has been “The Chipotle of Mediterranean Cuisine.” This illustrates that Chipotle’s brand has become a mainstay of the collective food consciousness in the U.S. Like Kleenex and tissues, Chipotle’s brand has become synonymous with its fast casual dining format.

- Economies of Scale: In addition to the brand, this is likely Chipotle’s strongest moat, in that Chipotle’s scale and operational expertise give it an advantage over its rivals. Chipotle leverages its scale to source high-quality ingredients at low costs, which allows it to offer its differentiated “taste adjusted calorie/$” value. Furthermore, Chipotle leverages its operational expertise, created through scale, to ensure competitors cannot reach the price point at which they’d begin genuinely competing against Chipotle. There’s a catch-22 for new competition: in order to compete against Chipotle’s nutritionally diverse, calorically dense, desirable offering at a “value-menu price,” they must achieve a certain level of scale and throughput, but this takes years to achieve, making it very difficult for competitors to sustainably compete against the value of Chipotle’s offering; hence, it essentially has no true, national competitors today, except perhaps, in a remote sense, CAVA, which is still only at about 300 restaurants, though we’re hoping it achieves thousands over time.

In short, Chipotle’s two strongest moats are its brand and economies of scale moats, and they have created a highly defensible franchise that has both pricing power and robust cash flow production, which we can confidently project into the future for the sake of modeling projected returns.

Employing Our Four Foundational Investment Frameworks

Chipotle fits perfectly into our second foundational investment framework, a description of which you may read below:

Businesses that will execute a leveraged recapitalization in the coming years or are extremely disciplined with capital allocation via routine, robust share repurchase programs: These are often fairly simple businesses that have fielded one or two products, which possess defensible moats that defend their stable cash flows as they gradually expand over a multi-decade period. The stable cash flows are not employed in the purchase of value accretive acquisitions; instead, they are channeled into capital return programs for shareholders, such as free cash flow per share accelerating share repurchase programs. Notably, the capital return programs act as disciplinary forces that ensure management operates as efficiently as possible and does not engage in empire building [Examples here include Chipotle, Meta, and, in the past, Google or Apple.]

With $1.9B in cash, no debt, ~15% free cash flow margins, one competitively advantaged offering, and a long runway for growth domestically and internationally, I believe Chipotle is the perfect “second foundational investment framework business.”

Over time, it can gradually expand its unit count at about 10% per year, creating sales growth of about 15% per year (including same store sales growth as more and more folks discover Chipotle’s unique offering compared to legacy fast food), and it can reduce its share count by about 1-2% per year as it embarks on a decade of robust free cash flow generation and sustained share buybacks.

Our balance sheet remains strong as we ended the quarter with over $1.9 billion in cash, restricted cash and investments with no debt. During the third quarter, we repurchased $226 million of our stock at an average price of $1,914, more than 2.5x our Q2 purchases as we were optimistic as the market softened. At the end of the quarter, we had $368 million remaining under our share authorization program.

Jack Hartung, CFO, Q3 2023 Chipotle Earnings Call

Concluding Thoughts: Valuation

I will say that the huge outperformance from Chipotle is likely behind us because its free cash flow margin has now reached the ~15% level at which I believe it’s prudent to model the company.

Chipotle’s EV/FCF, Quarterly Sales Growth, And The 10 Year Treasury Yield

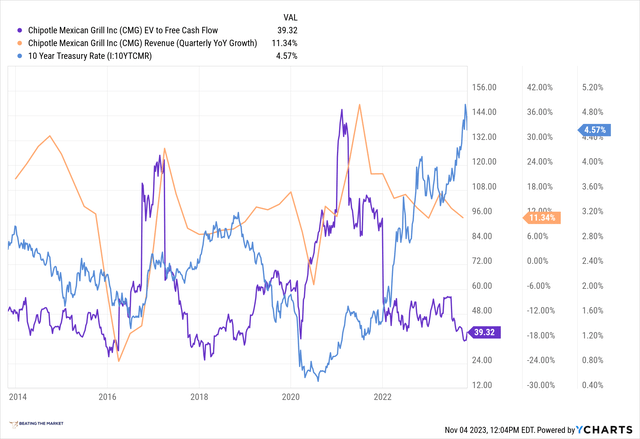

YCharts

As we can see, Chipotle offers an ~2.6% fcf yield, with sales growth of about 11%. I am confident that Chipotle has a long runway for growth domestically and internationally, so I believe this sales growth of 10%+ will be sustained for years to come. And the 10-year treasury bond offers a 4.57% yield as of today.

Taken together, I think Chipotle is modestly attractive today, though I’ve not been buying it lately.

Candidly, I was hoping that the stock would fall following its most recent earnings report, whereby I could once again resume buying and Chipotle’s CFO could buy back even more shares, but it ran following its recent earnings, so I will once again be patient with Chipotle.

Thank you for reading, and have a great day.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")