Q2 2026 Earnings Call Transcript")

")

Enerpac Tool Group (NYSE:EPAC) reported its latest Q4 earnings which came in ahead of previously announced guidance. The report was good enough for shares to rally by nearly 9% to their highest level in nearly 5 years. The global leader of high-pressure hydraulic and controlled force products has been able to push aside broader macro concerns with otherwise impressive operational and financial execution.

Indeed, that was the theme of our last article earlier this year highlighting how Enerpac was benefiting from its strategy initiatives known as “ASCEND Transformation” to streamline the business and boost profits.

Our update today looks at the latest developments while paring back some of our previous bullish optimism. Enerpac is a great company with overall solid fundamentals but we sense that the current valuation may limit the upside over the near term. We expect shares to face some volatility going forward.

EPAC Fiscal Q4 2023 Earnings Recap

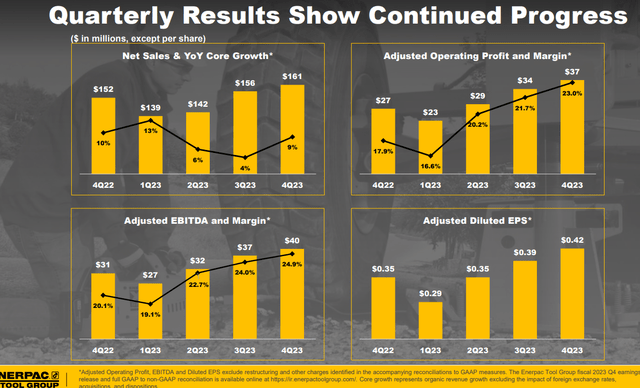

EPAC Q4 net sales reached $161 million, up 6% year-over-year, or stronger 9% as a “core” measure excluding the impact of divestitures. Net earnings of $23 million or an EPS of $0.42 was up from $0.35 in Q4 2022.

The story here is the sharply higher operating margin that reached 23% compared to 17.9% in the period last year. Similarly, the adjusted EBITDA margin at 24.9% was up sequentially from 24% in Q3. A large part of those gains have been based on the effort to improve operational efficiency and reduce costs.

Overall, the trends here cap off a record year that ultimately exceeded initial targets established in late 2022. Full-year adjusted EBITDA at $136 million increased by 65% y/y while free cash flow at $70 million was up by 57%.

source: company IR

Within the core business, the growth by region in Q4 picked up compared to a softer start of the year. For those not familiar with Enerpac, the company manufactures specialized hydraulic tools-based equipment with applications across industrial markets, construction, oil & gas, mining, and other types of areas with heavy operations.

Asia Pacific has been a strong point with growth in the “high teens” with Australia in particular balancing some softer trends in China. The Americas region is also contributing “high single-digit” growth with management citing strength in infrastructure and wind markets. On the other hand, the Middle East, North Africa, and Caspian region “MANAC” has been weaker in capturing the timing and exit of certain large-scale projects.

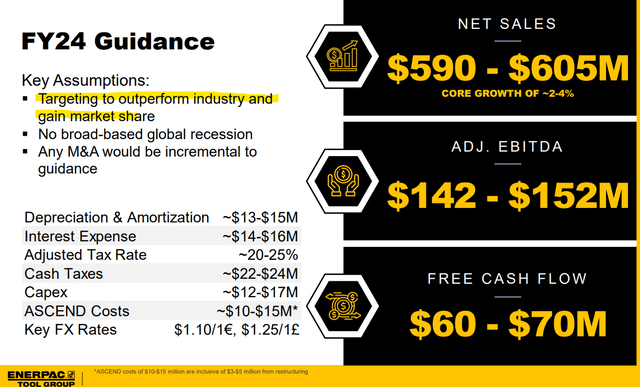

Overall, the expectation is for growth to continue into 2024 with Enerpac operating under the key assumption that there is no broad-based global recession. With that, official 2024 targets including net sales between $590 and $605 million representing a modest core revenue growth between 2-4%, while adjusted EBITDA between $142 and $152 million, if confirmed, would be around 8.5% higher than 2023.

Finally, we can mention that EPAC maintains a solid balance sheet, ending the fiscal year with $154 million in cash against $214 million in debt. A net leverage ratio of 0.6x is down from 0.9x at the end of 2022.

source: company IR

What’s Next for EPAC

There’s a lot to like about Enerpac as a high-quality industrial small-cap checking off all the boxes we believe makes for a worthy investment candidate. The company has a leadership position in its market, steady growth, recurring profitability, underlying free cash flow, and an unlevered balance sheet.

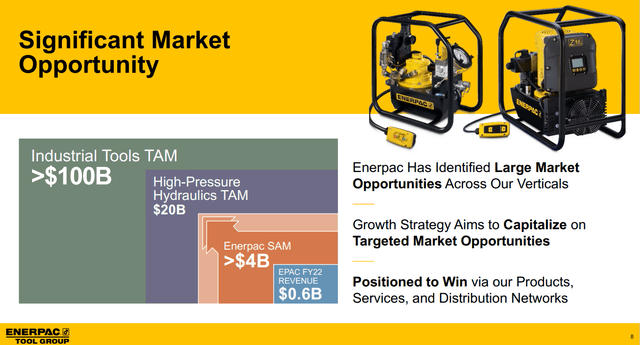

The company believes it operates in a $4 billion serviceable addressable midmarket (SAM) within a broader opportunity at up to $20 billion in the high-pressure hydraulics market. The effort here is to gain market share by expanding across industry verticals while leaving the door open for future strategic M&A opportunities.

source: company IR

That being said, the main headwind for the company remains the volatile macro environment. The combination of record interest rates, a strong U.S. Dollar, and soft industrial production indicators globally are not necessarily the best operating backdrop heading into the new year. If anything, the risks are tilted to the downside as it relates to the 2024 financial targets.

We also say that much of the benefits from the strategic initiatives and ASCEND Transformation have already been captured meaning it will become incrementally more difficult for margins to climb much higher.

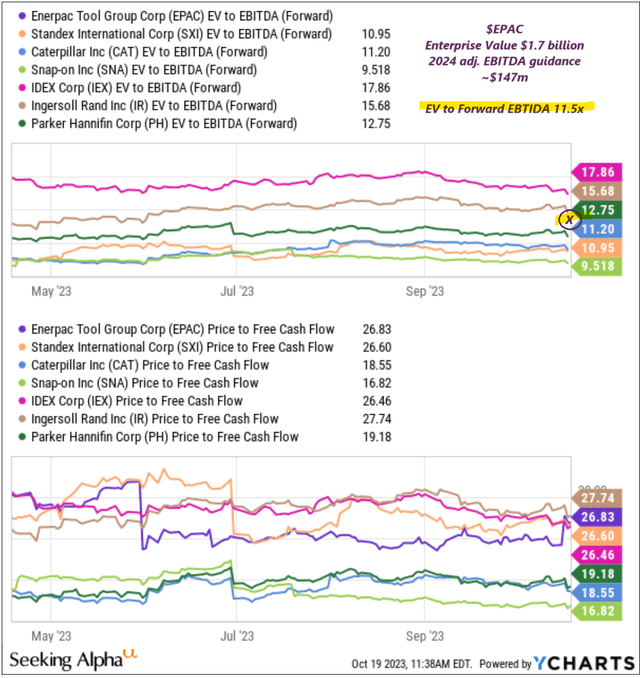

We bring this up because as good as the numbers looked for this last quarter, EPAC does not stand out as a bargain within the industrial sector. With shares trading at an EV to forward EBITDA multiple around 11.5x, this level is just average next to a peer group that we include names like Standex International Corp (SXI), Caterpillar Inc. (CAT), Snap-on Inc. (SNA), Ingersoll Rand Inc. (IR), and Parker-Hannifin Corp (PH).

Separately, we can point to EPAC trading at a price-to-free cash flow multiple of 27x which is at a premium to the group. Recognizing that each of these companies has its differences and focus on various markets, keep in mind that Enerpac management expects core growth in the low-single-digit range for 2024 which is hardly exceptional.

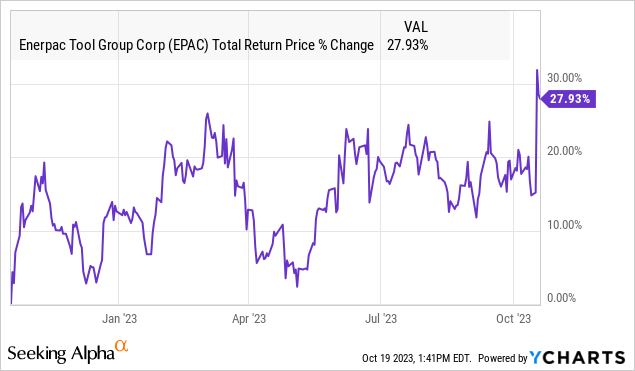

source: yCharts

Final Thoughts

There is no big hero call on our part other than to say we believe EPAC is near fair value around $30.00 justifying a “hold” rating. To the upside, we’d want to see evidence of growth accelerating as a catalyst for shares to run significantly higher and justify a larger valuation premium.

On the downside, the company would not be immune to a deteriorating economic environment as pressuring demand for its core products. Weaker-than-expected results over the next few quarters could open the door for a deeper selloff in the stock. Monitoring points into 2024 include the trends in operating margin as well as the growth by region.

Seeking Alpha

Read the full article here

Q2 2026 Earnings Call Transcript")

")

(NASDAQ:MU)")

")