")

")

When it comes to residential REITs, one prospect that investors should not pass up looking into is Mid-America Apartment Communities (NYSE:MAA). As its name suggests, the company focuses on acquiring and renting out apartments. Given the large percentage of Americans who rent instead of own, and because of the rising cost of home ownership, you would think that the market would be enthusiastic about a business like this. But since I last wrote about the firm in August of 2021, in an article where I called the company a ‘pricey’ prospect, shares have generated downside of 32.3% at a time when the S&P 500 has increased by 3.2%.

Such a massive return disparity might be chalked up to weak fundamental performance. But the fact of the matter is that management has continued to grow the company’s top and bottom lines at a respectable clip. All of this downside has to do with how pricey the stock has been and the fear that broader economic conditions might eventually bring about weakness for the business. Naturally, I can understand why this might make investors shy away from a firm of this nature. But for those who still want to participate in this space and who want to do it in a ‘safer’ way, buying into the preferred units of the company, known as the 8.50% Series I Cumulative Redeemable Preferred Stock (NYSE:MAA.PR.I), is definitely worth considering.

Check-in on Mid-America Apartment Communities

Before we dive into why investors might prefer the preferred units of Mid-America Apartment Communities, we should first touch on the business as a whole and how it has operated recently. As far as REITs go, Mid-America Apartment Communities has been around for quite a while. The company has been publicly traded for 29 years and, since its founding, it has grown to around 102,000 apartment units spread across 290 apartment communities. This does not include five development communities currently under construction that should have around 1,970 apartment units upon completion.

Geographically speaking, Mid-America Apartment Communities has operations in 16 different States and the District of Columbia. And just like any company, it has a specific set of geographic areas that it specializes most in. Its greatest exposure, for instance, is to Atlanta, Georgia. 12.7% of its NOI (net operating income) comes from that state. This is followed closely by Dallas, Texas at 10%, with Tampa, Florida, coming in at third place at 6.9%. Another way to look at the company is through the lens of where in an economic system it operates. For instance, 48% of its business is located in what’s called the inner loop of a city. This is followed by 40% attributable to suburban areas or small satellite cities near larger ones.

Author – SEC EDGAR Data

Over the past several years, the overall trajectory for the REIT has been positive. Consider, however, the most recent financial performance as an indicator of success. In the first nine months of this year, Mid-America Apartment Communities generated revenue of $1.61 billion. That’s up nicely from the $1.49 billion generated one year earlier. Average effective rent per unit growth of 8.7% more than offset a slight decline in the occupancy rate of its properties, bringing same store segment revenue down to an increase of 7.6% year over year. Recently completed development communities and recently acquired communities also helped to push non same store and other revenue up by 8.3%.

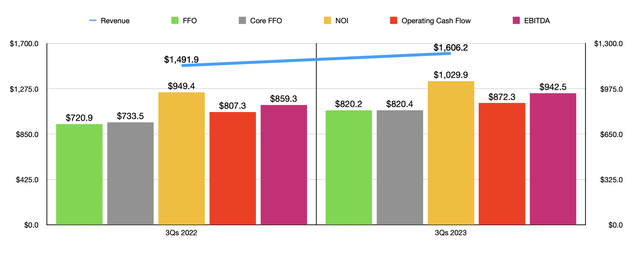

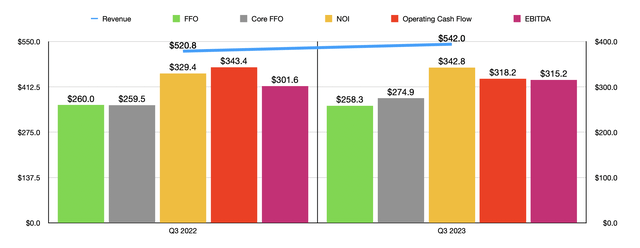

This revenue has brought with it higher levels of profitability as well. FFO, or funds from operations, grew from $720.9 million in the first nine months of last year to $820.2 million the same time this year. Core FFO increased similarly from $733.5 million to $820.4 million. Operating cash flow, which is my favorite profitability metric, jumped from $807.3 million to $872.3 million, while NOI, or net operating income, expanded from $949.4 million to $1.03 billion. And finally, EBITDA for the REIT managed to rise from $859.3 million to $942.5 million. As you can see in the chart below, financial performance for the third quarter on its own was similarly impressive on a year over year basis, though there were some weak spots from a profitability perspective.

Author – SEC EDGAR Data

When it comes to the current fiscal year in its entirety, management has provided a bit of guidance. At the midpoint, they expect NOI to grow by 6%. I assumed that both operating cash flow and EBITDA would grow at the same rate. Both FFO and core FFO have been assumed to grow at a rate that would match midpoint guidance for those, on a per share basis, as management indicated in the third quarter of the 2023 fiscal year.

Author – SEC EDGAR Data

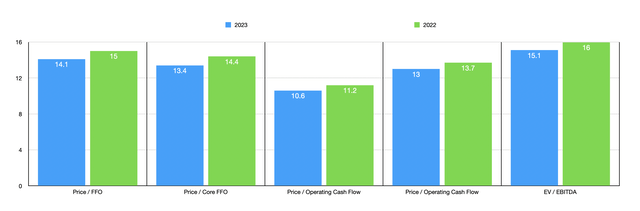

Using these figures, I was then able to create the chart above. In it, you can see how the stock is priced on a forward basis and how it is priced using the data from 2022. I definitely would not call the stock expensive given how far shares have fallen. To put this in perspective, consider how shares were priced when I last wrote about the company. On a forward basis, the price to operating cash flow multiple stood at 26.8. Meanwhile, the EV to EBITDA multiple came in at 28. The numbers we have today are around half of that. So if anything, the stock looks affordable.

A look at the preferred units

To some investors, the fact that shares fell so much already might be a deal breaker. Further concerns about the economy might also make this a hard firm to convince investors to be optimistic about. But if you have something with a different risk profile, that picture could change rather markedly. And here’s where the preferred stock comes into play. At present, shares are trading at $54.15. It’s also important to note that they have some interesting traits about them. For starters, the units are cumulative. This means that if management were to ever cut the distribution, that the preferred holders get paid before the common and that they get paid as though the distribution had never been cut. As an example, the preferred units pay out $4.25 in distributions per year. If the company were to stop paying on the preferred for two years, not only would it need to stop paying on the common, it would also have to pay $8.50 in ketchup payments to cover those two missed years before common holders could get a single red cent.

To many investors, this is a huge benefit. But honestly, I don’t see any reason for investors in this particular firm to value this trait. After all, Mid-America Apartment Communities should generate around $1.12 billion in operating cash flow this year. And given the 867,846 shares of preferred units outstanding, it should only pay around $3.69 million toward preferred distributions. In the grand scheme of things, this is a rounding error for the enterprise. The other interesting trade about these particular units is that they are redeemable. Specifics can vary from one type of preferred unit to another. But according to the data available, on or after October 1st of 2026, the management team at Mid-America Apartment Communities has the option to buy back the preferred units in exchange for cash at the liquidation value of $50 per unit.

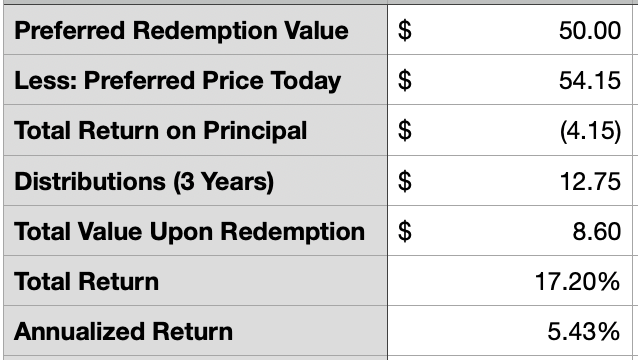

What this means is that, even though shares are trading at $54.15 right now, the decision by management, if enacted, will result in principal loss of $4.15 per unit. It may seem crazy to buy a security that is almost guaranteed to go down in value at some point. And in the event that interest rates do plunge, it would become much more appealing for management to redeem those units when the time does come. The reason why somebody would hold the preferred units is because of the $4.25 they pay out each year between now and then. There should be exactly three years’ worth of payments, which would translate to $12.75. After factoring in the haircut on the principal, investors should get $8.60 per share in the form of a return should management ultimately redeem the stock on the date that they can.

Author – SEC EDGAR Data

When you run the math, you end up with a total return of 17.2%. That’s about 5.43% per annum. While that’s not bad, it’s not all that much higher than the 5.24% yield to maturity on 12 month US Treasuries or the 4.90% on the two year ones. Common units of Mid-America Apartment Communities have a current yield of 4.57%. And unlike the preferred units, the common units not only can get additional upside in the form of additional distribution hikes, they also get the benefit of additional upside from capital appreciation if all goes according to plan.

Takeaway

Fundamentally speaking, Mid-America Apartment Communities is doing a fine job. To some investors, the common units might still be considered expensive. But in all honesty, they are starting to look appealing. I still have that stock rated a ‘hold’ in my head at this time. But in the event the prices pull back another 10% or so, I don’t think I will be able to resist a more bullish rating. Those who want to generate cash flow because of this industry might want to consider looking at Mid-America Apartment Communities. There are certain traits about it that might appeal to certain investors. But I would imagine that group to be quite narrow in scope. For those focused on long term upside, the preferred units definitely look interesting. But I would argue that the common still would be the better way to go.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")