")

")

Shares of Nordstrom (NYSE:JWN) have been a poor performer over the past year, losing about 30% of their value as the company has battled through excess inventory, stagnating consumer demand, and an exit from its Canadian operations. Ultimately, the company is still lagging behind its peers on inventory improvement, and so I see better opportunities elsewhere.

Seeking Alpha

In the company’s third quarter, JWN earned $0.25, which beat consensus by $0.12, even as revenue fell by 6.5% to $3.3 billion. Inventories were down an even sharper 9% as the company has worked to right-size levels given the weaker sales environment. This has enabled the company to be less promotional, which is why earnings were higher than last year’s $0.22.

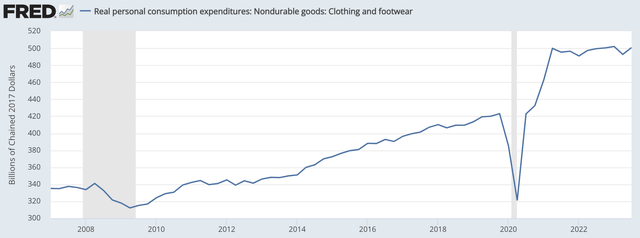

Gross margins were up 180bp from last year to 35%. This is a definite positive. There is no doubt that the company is in a better inventory position than it used to be. Like many other retailers, JWN was overstocked in late 2021 and 2022. As you can see below, apparel consumption surged after COVID as consumers spent down excess savings. As inflation rose and these savings shrank, sales have since stagnated. With inventories building up but sales flatlining, retailers like Nordstrom had to resort to excessive discounting to move products.

St. Louis Federal Reserve

On the bright side, because sales have stagnated for so long, apparel spending levels no longer look so stretched relative to trends. Apparel spending has now risen 4% per annum since 2019, which is above the ~3% pre-COVID trend, but no longer egregiously so. Absent a recession, I do expect that apparel spending can return to real growth next year.

The question for retail sector investors needs to not just be “have inventories fallen” but “have they fallen enough.” Yes, Nordstrom’s inventories are down 2% more than sales, but if they were more than 2% overstocked, this relative decline would not be enough. I fear that is where Nordstrom sits. At the end of Q3 2019, JWN carried $2.54 billion of inventories while sales were $3.6 billion. Inventories are $2.63 billion today while sales are $3.3 billion. Inventories are 3.5% higher even as sales are 8% lower than pre-COVID. Yes, inventory is more productive than the terrible 2022 levels, but this is still 11.5% degradation from pre-COVID relative inventory levels. By comparison, Macy’s has 17% lower inventories today than in 2019.

To me, it seems that Nordstrom is less over-stocked, but that it is still over-stocked. In a sector already facing secular pressure from e-commerce and filled with companies trading below 10x earnings, value investors have the ability and necessity to be choosy in what shares they buy, using stringent criteria. Strong inventory control is one of those, given the importance of maximizing margins in a world where sales growth is sluggish.

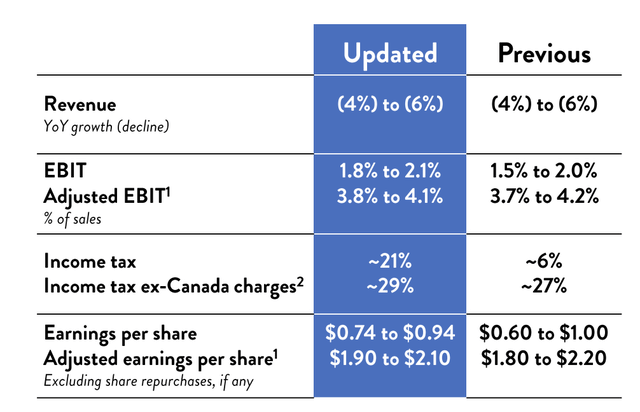

Given this level of inventories relative to 2019, JWN is going to need a very strong holiday season to move sufficient products and avoid having excess stock after Christmas that it needs to mark down. I am not certain that will occur, and management’s updated guidance does not seem to point to it either. If the company raised guidance, that would imply a stronger Q4, which could potentially justify inventory levels. Instead, it left revenue unchanged and simply narrowed adjusted EBIT margin and EPS ranges while leaving their midpoint unchanged. This does not point to a brighter year-end.

Nordstrom

Moreover, apparel-centric retailers like Nordstrom always add inventories through the first nine months of the year because Christmas is such a critical quarter. Sales rose about 20% sequentially from Q3 to Q4 last year. However given inventories started the year bloated and that management has prioritized inventory optimization this year, I would expect inventories to have risen more slowly. That has not occurred. Inventories are up $687 million so far this year vs $550 million last year. I simply do not see the level of inventory discipline necessary to make me confident JWN will not have to return to promotions and shed gross margins if this holiday season proves to be a bit softer.

Within its two brands, Nordstrom’s revenue was down 9%, or 4.9% adjusting for its exit from Canada. Rack was down 2%. Management said it is seeing sequential improvement in activewear, beauty, and accessories. Given lower income consumers are facing more pressure, given inflation and exhausted excess savings, the underperformance of its main brand to its off-label brand is surprising and adds to my concern Nordstrom has lost relevance to its target customer, which will make it even more difficult to maintain pricing and grow sales.

Elsewhere, SG&A spending was down by 7%, roughly in line with sales. Net interest expense of $24 million was down from $32 million last year as it is earning more interest on its cash balances, which are up by $82 million to $375 million. I would note its share count is up over 2% from last year due to share-based compensation. While JWN has $438 million of buyback capacity, it is focusing on its balance sheet, targeting 2.5x debt to EBITDA leverage.

JWN carries $2.9 billion of debt; $250 million matures within the next year. It has generated $749 million of EBITDA this year, excluding the Canada winddown costs. Given a stronger Q4 seasonally, leverage will be about 2.6x this year, so its balance sheet is getting closer to acceptable levels, assuming EBITDA does not degrade in 2024, though refinancing maturities in this environment likely will increase interest costs.

I also would caution investors about being too concerned about the fact-free cash flow is -$269 million so far this year. As noted, it builds inventory in the first nine months and then sells it down in Q4, causing seasonal working capital moves. Excluding working capital, free cash flow has been ~$175 million and should finish the year over $275 million. This does provide scope to continue paying a $0.19 dividend.

At about 7.5x earnings and 8-9x free cash flow, JWN is not an expensive stock. However, with sales still declining and inventories elevated, it is not clear this company is yet through with excess promotions. Shares may be cheap for a reason, in other words.

Some of the problems that have plagued shares for 2023 may continue into 2024, further pushing off potential, meaningful buybacks, and increasing my concern that JWN proves to be a value trap. With companies like Macy’s far better positioned on inventory and more likely to have seen their business trough, I would invest elsewhere and expect Nordstrom shares to continue to underperform.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")