")

Q4 2025 Earnings Call Transcript")

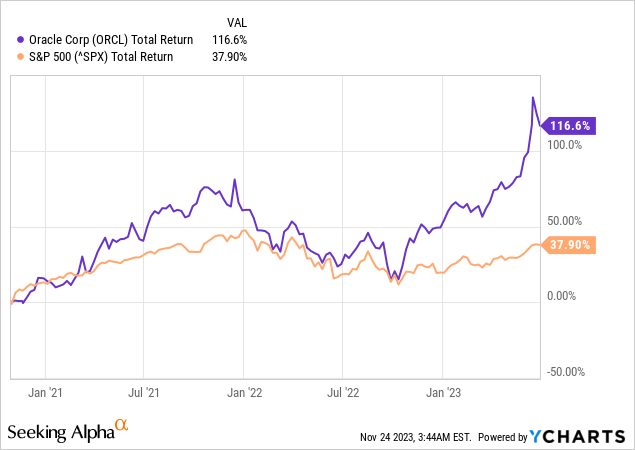

From one of the ugly ducklings in the software and cloud space, Oracle (NYSE:ORCL) has gradually become one of the best success stories in the space.

Not only when it comes to actual business performance, but in terms of shareholder returns as well. Since October of 2020, when I went against the popular opinion and rated the stock as a Buy, ORCL has delivered a total return of 116% when the S&P 500’s total return stood at less than 38%.

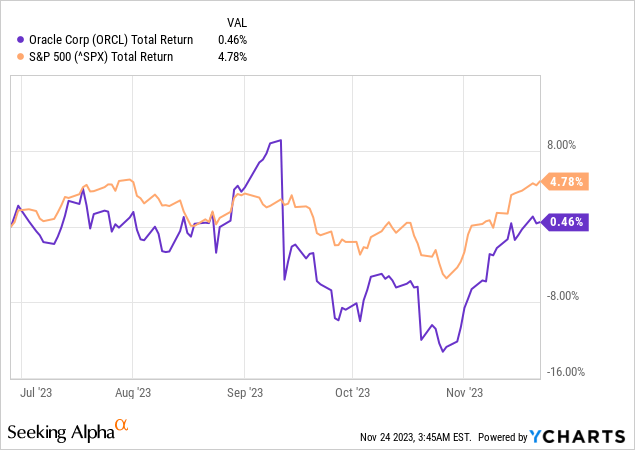

The data above is presented up until the end of June of this year, when I changed my rating on the stock from Buy to Hold as the stock was running ahead of fundamentals. Although it has been only 5 months since then, ORCL’s performance has been far less impressive during this period of time.

This has been partly driven by the excessive optimism around AI and a wave of sell-side analyst upgrades in recent months.

Seeking Alpha

Nevertheless, these short-term movements are not a reason for buy and hold investors to sell, but rather a good opportunity to rebalance existing positions. I covered all that in further detail for my subscribers in June of this year, when I also reduced the share of Oracle within The Roundabout Portfolio – a model portfolio consisting of all of my high conviction ideas.

Now that ORCL stock has literally gone nowhere in the past couple of months and the company is scheduled to report Q2 2024 earnings in about two-weeks’ time, can we expect for Oracle’s stock to finally break away from the current flat-line trend?

A Mixed Picture In The Short Term

Following the Cerner deal, Oracle’s management has resorted to more Non-GAAP metrics as acquisition related costs and the restructuring of the acquired business is ongoing.

I have previously shared my view that the Cerner deal is a very good fit strategically of Oracle, but it would likely take time before the benefits are fully realized. For the time being, Non-GAAP results are encouraging and Oracle remains one of the most highly profitable entities in the sector.

Non-GAAP operating income was $5.1 billion, up 12% from last year. The operating margin was 41%, up from 39% last year. As we continue to benefit from economies of scale in the cloud and drive Cerner profitability to Oracle standards (…)

Source: Oracle Q1 2024 Earnings Transcript

Nevertheless, I have also previously criticized the practice of investors relying too much on Non-GAAP metrics. A perfect example of this has been Salesforce (CRM), which I assigned a Sell rating to back in December of 2020. Having said that I have recently become more optimistic on CRM’s future and will be covering the company more extensively in my investment group.

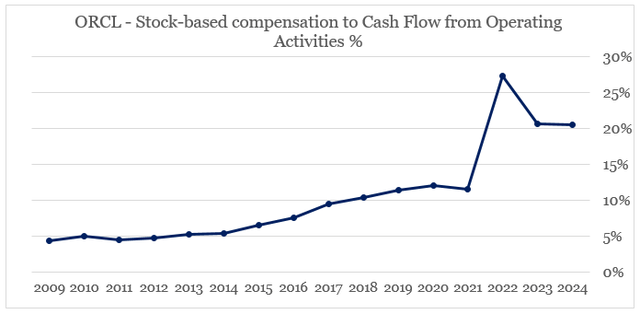

Back to Oracle, the problem that I have with Non-GAAP metrics is not only acquisition-related costs and the ongoing restructuring of Cerner, but rather the excessive use of stock-based compensation in recent years. From share-based compensation standing at around 10% of cash flow, the ratio has nearly doubled in FY 2023 and now stands at more than 20%.

prepared by the author, using data from SEC Filings

This is usually works well during short-periods of time when a stock is trading at attractive levels, but is unsustainable strategy to achieve high profitability over the long-run.

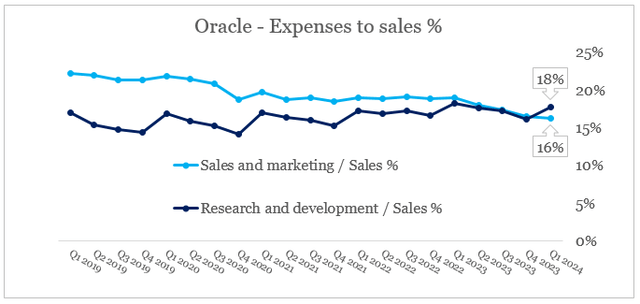

To Oracle’s credit, economies of scale have been significant in recent years and the share of Sales & Marketing Expenses to Total Revenues has continued to decline on a quarterly basis. At the same time, Oracle continues to reinvest heavily into the business in the form or research and development.

prepared by the author, using data from SEC Filings

In combination with the higher revenue growth, this has resulted in a 9% increase in cash flow from operations during the last quarter and in my view will continue to be a tailwind for the foreseeable future.

Operating cash flow for the first quarter was up 9% to $7 billion, while free cash flow was up 21% to $5.7 billion and I expect that we will see a very good result in our free cash flow for the rest of the year.

Source: Oracle Q1 2024 Earnings Transcript

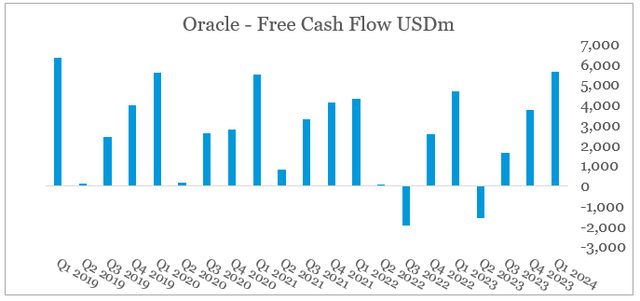

Free cash flow has also improved considerably during the most recent quarter, but at the same time Oracle is still trading at very low yields even on a forward-looking basis.

Seeking Alpha

Even when looking at free cash flow on a quarterly basis since 2019, the trend is hardly anything to get excited about.

prepared by the author, using data from SEC Filings

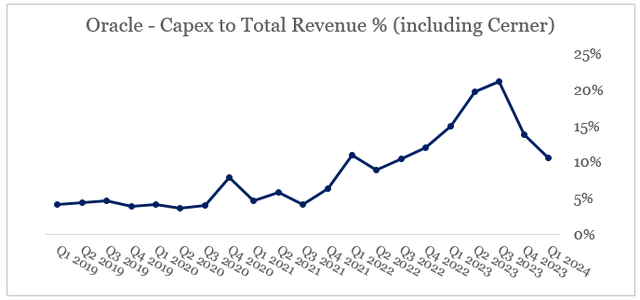

But that’s only above the surface since Oracle has ramped-up its capital expenditure in recent years as demand for its cloud infrastructure business has accelerated and resulted in supply constraints.

prepared by the author, using data from SEC Filings

As we look at the graph above, it appears that Oracle’s Capex is already off from its peak levels and we could finally see a meaningful improvement in free cash flow. But that is unlikely to be the case as Oracle’s management expects capital expenditure to remain constant during fiscal year 2024.

Given the demand we have and see in the pipeline, I expect that fiscal year 2024 CapEx will be similar to this past year’s CapEx.

Source: Oracle Q1 2024 Earnings Transcript

On one hand, this will continue to put pressure of free cash flow during FY 2024, but on the other it is very good news for long-term shareholders as it signals that demand for Oracle’s cloud remains robust.

Strong Momentum And High Expectations

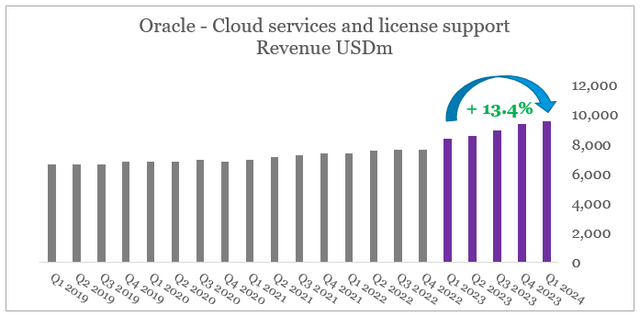

Growth at Oracle’s cloud services and licence support segment is now in the low-teen levels and given the company’s strong competitive positioning and the optimism of Oracle’s management regarding customer demand, I would expect this to be sustained in FY 2024.

prepared by the author, using data from SEC Filings

As OCI continues to narrow-down the gap with the hyperscalers in cloud infrastructure, the company was also recently recognized as the leaders in the emerging space of hybrid cloud infrastructure.

Oracle Website

In the meantime, sell-side analysts will be expecting very strong results from Oracle’s second quarter of this fiscal year as the management provided an optimistic guidance and is continuing to attract large OCI customers.

Total cloud revenue excluding Cerner, again, I give you these numbers, so you can see the mainline business, is expected to grow from 27% to 29% in constant currency and is expected to grow 29% to 31% in USD. (…)

We have now signed several deals for OCI greater than $1 billion in total value. In the first week of Q2, we booked an additional $1.5 billion in business, which isn’t even included in the Q1 numbers.

Source: Oracle Q1 2024 Earnings Transcript

On the Software-as-a-Service side, Oracle’s business is also firing on all-cylinders with strong double-digit topline growth during the latest quarter and a number of new large scale customers.

Oracle Q1 2024 Earnings Release

And I’m now able to announce that all nine utility companies owned by Berkshire Hathaway are in the process of replacing all their existing ERP systems, and standardizing on Oracle’s Fusion Cloud applications.

Source: Oracle Q1 2024 Earnings Transcript

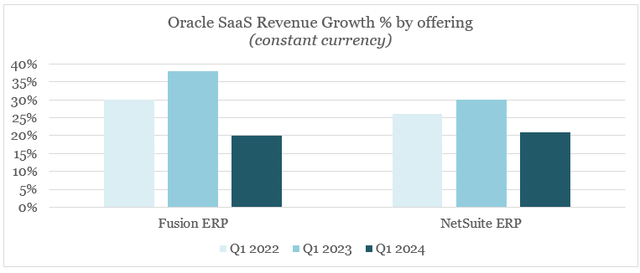

However, the Fusion and NetSuite ERP offerings saw a meaningful drop in their quarterly revenue growth dates during the last 3-month period. This is hardly an unexpected event as larger scale takes its toll on quarterly growth rates.

prepared by the author, using data from Earnings Releases

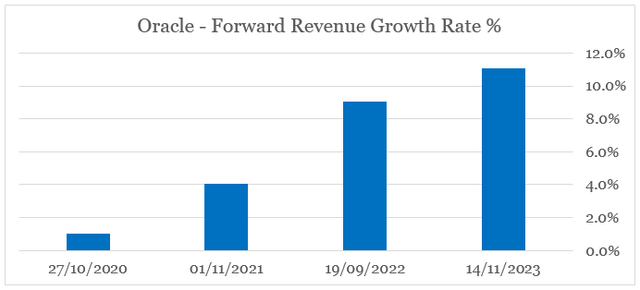

Overall, FY 2024 would be another strong year for Oracle which is likely to attract more growth-oriented investors. When it comes to share price returns, however, the currently expected revenue growth rate by sell-side analysts of around 11% would be a hard target to beat given the quarterly guidance for Q2 2023.

(…) total revenues including Cerner are expected to grow from 3% to 5% in constant currency, and are expected to grow 5% to 7% in USD at today’s rates. Total revenue excluding Cerner are expected to grow from 6% to 8% in constant currency and expected to grow 8% to 10% in USD.

Source: Oracle Q1 2024 Earnings Transcript

This is in stark contrast to 2020-21 period, when much lower expectations were priced-in Oracle’s share price as far as topline growth was concerned.

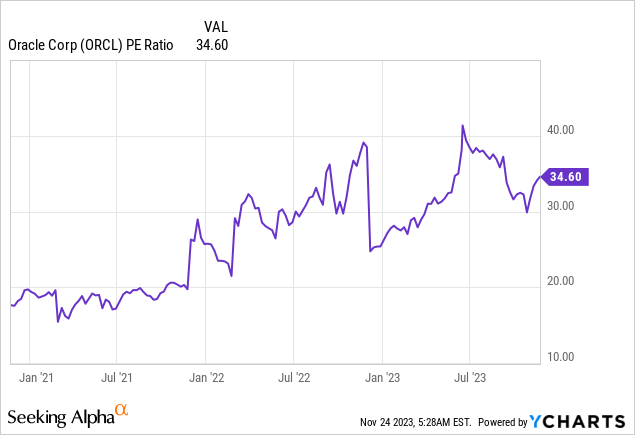

prepared by the author, using data from Seeking Alpha

Although a higher earnings multiple is now justified based on the accelerated revenue growth, short-term share price performance is largely limited at a P/E multiple of almost 35 and a management team that is focused on long-term competitive positioning of the business as opposed to meeting quarterly earnings estimates.

Conclusion

After delivering outstanding shareholder returns over the past few years, Oracle remains as one of my top picks within the large cap software space. The company has significant competitive advantages in the SaaS space and is slowly closing the gap with the current leaders in infrastructure. Having said that, FY 2024 will be yet another year that will require higher-than-usual reinvestments into the business and ongoing restructuring at Cerner. At the same time, sell-side analysts have become too optimistic on short-term business performance and this will continue to put pressure on share price returns.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")