2026-04-02")

PIMCO recently launched the Multisector Bond Active Exchange-Traded Fund (NYSEARCA:PYLD). PYLD offers investors diversified exposure to bonds and sports a 5.6% SEC yield. Most other PIMCO bond ETFs have slightly outperformed their benchmarks since inception, and PYLD seems likely to do so too. I think the fund is a reasonable investment, but I’m more bullish on shorter-term and variable rate bond funds right now, due to their comparatively higher yields.

PYLD – Basics

- Investment Manager: PIMCO

- Dividend Yield: 5.89%

- Expense Ratio: 0.55%

PYLD – Overview

Diversified Bond Holdings

PYLD is an actively-managed diversified bond ETF. The fund invests in most relevant bond and bond sub-asset classes, including treasuries, MBS, corporate bonds, leveraged loans, and preferreds. The fund currently invests in 442 different bonds. Numbers might rise as the fund gets more established. Asset allocations are as follows.

PYLD

Importantly, PYLD invests in both investment-grade and high-yield bonds, while most bond ETFs focus on one of these. As an example, the largest bond ETF in the market, the iShares Core U.S. Aggregate Bond ETF (AGG), exclusively invests in investment-grade bonds. As such, PYLD is quite a bit more diversified than average, an important benefit for shareholders.

PYLD sometimes uses leverage, see net other short duration instruments above, although I am unsure about their magnitude or other specifics. Some derivatives and MBS are, for accounting purposes, leveraged investments, and I am aware that PIMCO sometimes invests in these. In any case, PYLD’s use of leverage boosts yields, returns, risk and volatility. The net effect is broadly positive, but more risk-averse investors might disagree.

Credit Risk Analysis

PYLD’s underlying holdings have a wide variety of credit ratings, from AAA to B (with nominal investments in CCC). The median rating is A, mode is BBB. Although credit quality seems good, over half the fund’s holdings are not rated, which tends to indicate below-average credit quality (or worse). In this particular case, not rated securities seem to be securitized investments, including MBS, CLOs, and others. Credit quality for these securities vary, but most tend to be of high quality.

PYLD – Table By Author

Ideally, we would compare PYLD’s performance during a recession with other bond ETFs to ascertain its overall credit quality (higher losses would indicate lower quality, and vice versa). As the fund is quite young, this is not feasible.

In my opinion, PYLD’s credit quality is about average, and so the fund should see average losses during downturns. Losses should be higher than those of AGG, but lower than those of, say, the iShares iBoxx $ High Yield Corporate Bond ETF (HYG).

Interest Rate Risk

PYLD has quite a bit of interest rate risk, with a duration of 9 years. Duration is very high on an absolute basis, and moderately higher than average. Duration is also higher than expected for a fund with PYLD’s asset mix, most likely due to a combination of leverage and active management.

Fund Filings – Chart by Author

PYLD’s high duration increases interest rate risk and exposure, boosting portfolio risk and volatility.

In my opinion, the net effect long-term is overwhelmingly negative, due to increased risk.

In the short-term, funds with high duration can outperform if rates decrease, but I do not believe this to be all that likely. Economic conditions do not currently support lower rates, as inflation remains above target and unemployment low. At the same time, the market already expects significant rate cuts, and is pricing bonds accordingly.

As such, and considering the above, I strongly prefer funds with lower duration and rate risk than PYLD right now. I went through some of these here.

Performance Analysis

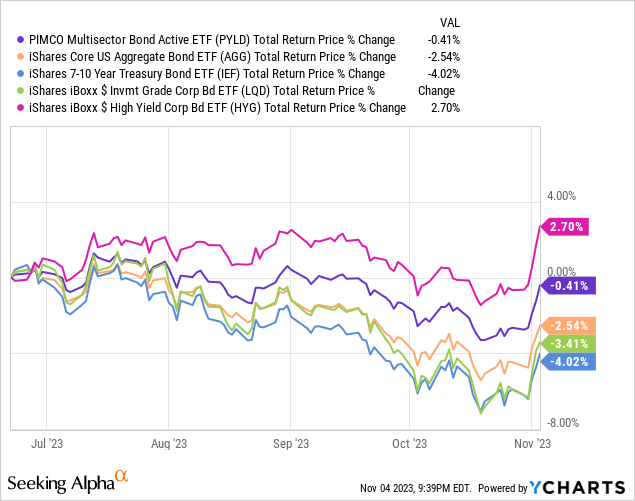

PYLD is a relatively young fund, being created in mid-2023. Due to this, the fund’s performance track-record is very short, and not terribly material to investors. For what it’s worth, PYLD has outperformed most of its peers since inception, with the exception of high-yield bonds.

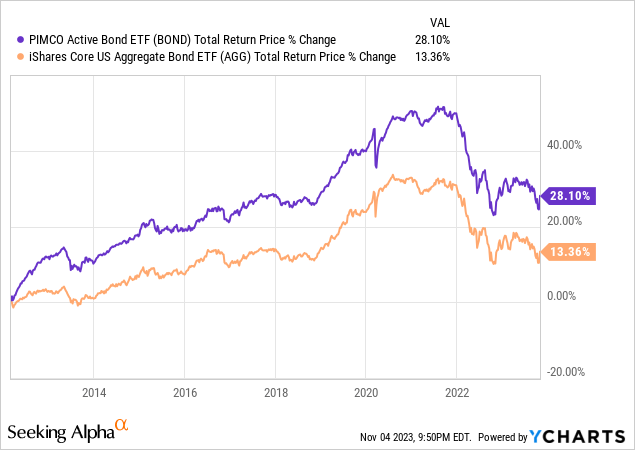

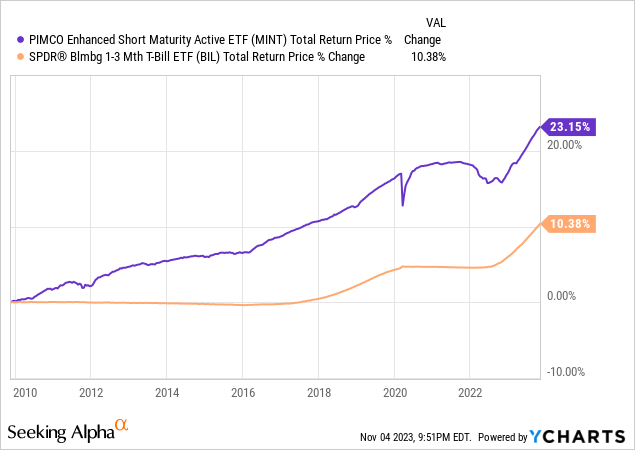

PYLD is managed by PIMCO, an investment management firm with a decades-long track-record of successful fixed-income investment and management. Bill Gross’s run was legendary, and although returns for most of the company’s funds have softened since, these remain reasonably good. Most of PIMCO’s actively-managed bond ETFs have outperformed their benchmarks, including the company’s most broad bond ETF:

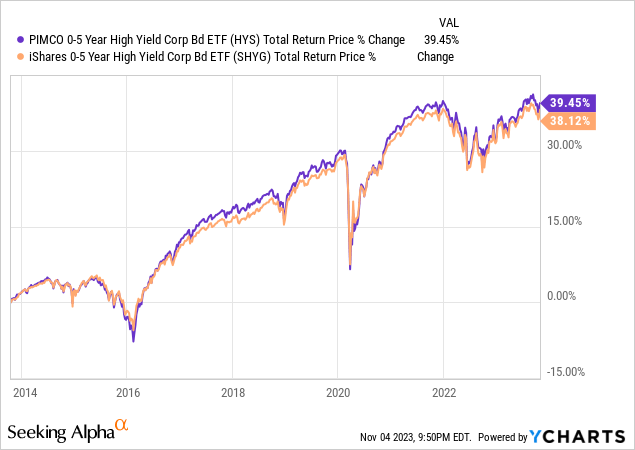

as has PIMCO’s short-term high-yield bond ETF:

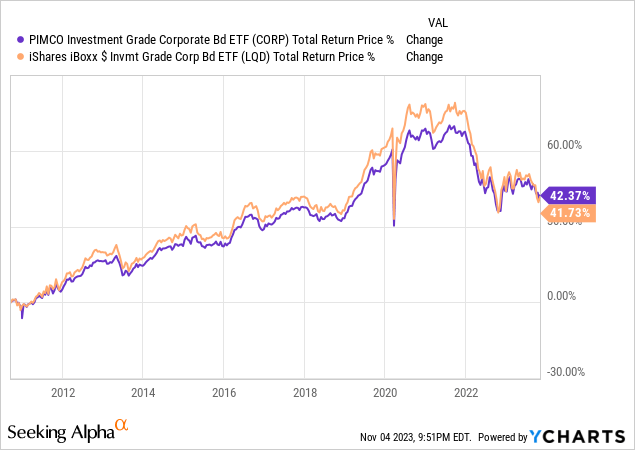

as has PIMCO’s investment-grade bond ETF:

as has PIMCO’s ultra low duration bond ETF:

Outperformance is rarely significant, but it is generally consistent and material. In practice, most of the excess gains get captured by PIMCO through (higher) fees, but investors do get some of these.

In my opinion, and considering the above, PYLD is likelier than not to outperform moving forward. Reasonable to invest in the fund based on such assumption, in my opinion.

Dividend Analysis

PYLD’s dividends are reasonably good, and above-average.

The fund currently sports a 5.9% dividend yield, from annualizing its latest monthly dividend payment.

It sports a 5.9% SEC yield, indicative of the income generated by the fund’s underlying holdings the last month. Same as its dividend yield, as expected for an ETF.

It sports a 7.3% yield to maturity, indicative of the returns the fund can expect from holding its bonds until maturity. This figure is quite a bit higher than the other two, as many of the fund’s bonds have seen their prices decrease due to higher interest rates. Prices should recover as bonds mature, leading to excess returns.

PYLD’s 7.3% yield to maturity is a forward-looking metric, and more indicative of the returns and dividends that investors should expect moving forward.

Dividend yields for PYLD and its peers are as follows.

Fund Filings – Chart by Author

Tying It All Together

PYLD is an actively-managed diversified bond ETF by PIMCO. In my opinion, the fund’s most important benefit is its investment manager, and the expertise and expected outperformance said manager brings. PIMCO bond ETFs tend to outperform their benchmark, and I think that will be the case for PYLD moving forward as well.

PYLD versus Short-Term and Variable Rate Funds

In my opinion, PYLD is a slightly stronger investment than the average bond and most of the larger bond sub-asset classes, with the exception of short-term and variable rate securities. There are many of these securities, although most are quite niche. I’ll do a quick comparison between PYLD and some of the more relevant, in my opinion, of these.

PYLD has much higher duration and interest rate risk than these other securities, boosting portfolio risk and volatility, and quite likely leading to underperformance if rates remain higher for longer.

Fund Filings – Chart by Author

PYLD’s dividends are somewhat lower, with the exception of t-bills.

Fund Filings – Chart by Author

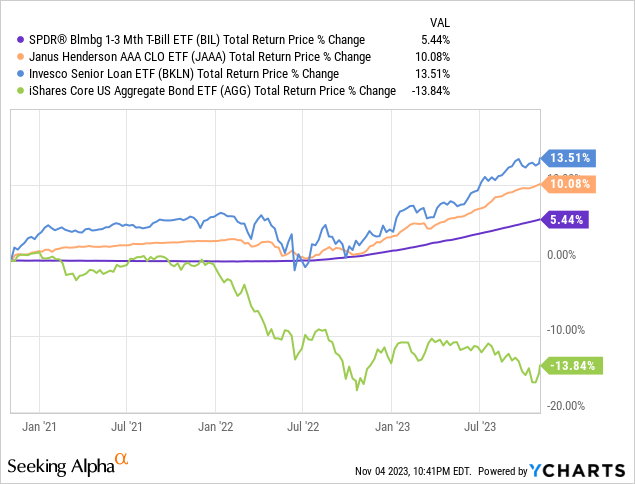

Credit risk varies, but several funds have higher credit quality than PYLD. These include the SPDR Bloomberg 1-3 Month T-Bill ETF (BIL) and the Janus Henderson AAA CLO ETF (JAAA).

Several short-term and variable rate funds have longer, and stronger, performance track-records than PYLD. As an example, the three funds above have all significantly outperformed broad-based bond indexes for the past three years or so. JBBB has outperformed since inception, close to two years ago.

PYLD seems like a good bond fund, but the four funds above seem better.

Conclusion

PYLD offers investors diversified exposure to bonds and sports a 5.6% SEC yield. It is managed by PIMCO, one of the strongest fixed-income investment managers in the world. I think the fund is a reasonable investment, but I’m more bullish on shorter-term and variable rate bond funds right now, due to their comparatively higher yields.

Read the full article here

2026-04-02")

")

")