Last week, I discussed preferred equity and detailed my view that the yield of preferreds was not high enough compared to risk-free assets to warrant their higher risk profiles. Not only preferred, but high demand for other financial products such as covered call strategy funds, junk bonds, and high-yield dividends shows how many investors are interested in income investing today. The sphere of personal investors is highly skewed toward retired people; however, statistically speaking, many are investing more like 30-year-olds by taking on much riskier assets than in the past, particularly regarding high-dividend investments.

When interest rates were at or near zero, it was more reasonable that retired people were looking to riskier bonds and stocks for a 4-6% dividend yield. However, today, the risk-free rate is 5.25%, so there is little benefit in earning a 6-8% yield at ~10-30X the volatility. For example, the iShares 0-3 Month Treasury Bond ETF (NYSEARCA:SGOV) has a 5.2% SEC yield (yield after expenses) and a 0.63% annualized standard deviation, while the junk bond ETF (HYG) has an 8.3% yield at an 8.7% standard deviation and the preferred equity ETF (PFF) having a 7.3% with a 12.5% standard deviation.

Of course, many investors also likely have significant cash positions that may not pay a considerable interest, given large retail banks have been slow to raise rates. Any cash position not earning a 5%+ yield today essentially gives money away to banks or brokers, meaning many investors are foregoing a significant amount of potential risk-free income. T-bill funds like SGOV are technically “risk-free” because the US government can create money to pay its bills, and failing to pay its bills would almost certainly harm T-bills and savings deposits equally.

There are a few reasons why SGOV may not be preferable due to potential changes in interest rates and inflation. That said, I firmly believe most investors would be best off allocating significantly to SGOV or similar money-market ETFs. To me, it appears that many investors have forgotten these funds because they paid virtually no yield for so long, just as many have come to expect that banks will not pay any interest on deposits. The era of “cheap money” passed years ago, and today, particularly in light of asset volatility, cash is almost certainly the most significant “reward for risk” asset class today.

How Long Will Yields Stay This High?

One downside of SGOV vs. other high dividend yield assets like junk bonds or preferreds is its lower maturity. On the one hand, SGOV’s low maturity makes its duration risk negligible, as duration risk has caused the ~50%+ devaluation of 20-year+ Treasury bonds like those in the Vanguard Extended Duration Treasury Index Fund ETF (EDV). Of course, with EDV, an investor can earn a 4-5% dividend for over 20 years on their current investment, while SGOV’s 5.2% dividend will only last as long as the Federal Reserve maintains elevated interest rates.

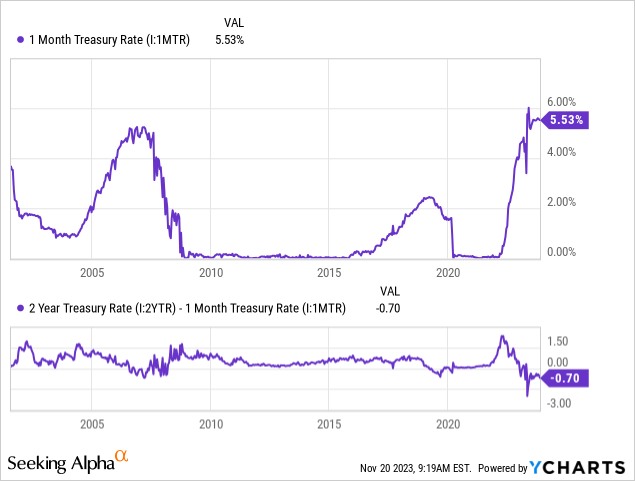

Currently, the discount rate is expected to be reduced by ~70 bps over the next two years, based on the spread between the two-year and one-month Treasury rates. This spread is slightly larger than at the peak discount rate in 2007, indicating a similar or faster rate of Federal Reserve cuts in response to a potentially impending economic slowdown. Still, today’s peak interest rate is much higher than in 2007. See below:

Even two years from today, the bond market is still pricing in a 4.5% discount rate and is never pricing in a rate below 4.25%. Of course, historically, rates still fluctuate more than the yield curve suggests, often falling lower than the curve suggests but occasionally doing the opposite in the event of rebounding inflation like that seen in the 1980s.

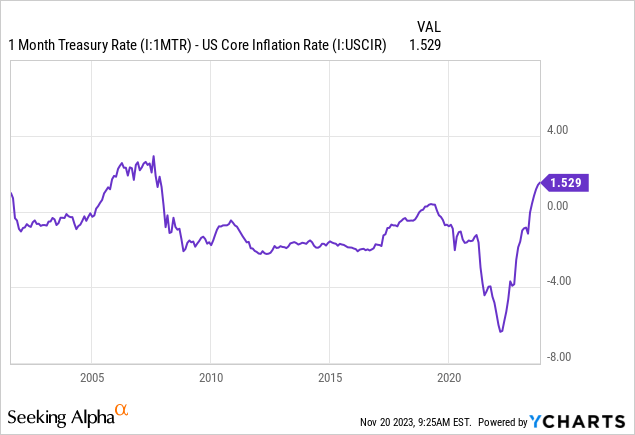

Today, now that core inflation is slipping, the one-month Treasury rate is firmly above core inflation. Previously, investors in SGOV did not earn a positive return after inflation. Today, they can expect to earn a “real yield” of about 1.5% after inflation and more if we assume inflation will continue to slow over the next year. See below:

The “real yield” is a major driver of economic activity. When short-term rates are below inflation, companies and households are highly incentivized to spend money because goods rise faster than short-term borrowing costs. Since about July of this year, the discount rate has been firmly above the core inflation rate, incentivizing saving over spending. Now, households should have the most value by parking money in 5%+, yielding cash that goods are not rising as quickly. This pattern may continue for a year or two, but real yields on short-term borrowings usually average around zero in the long run.

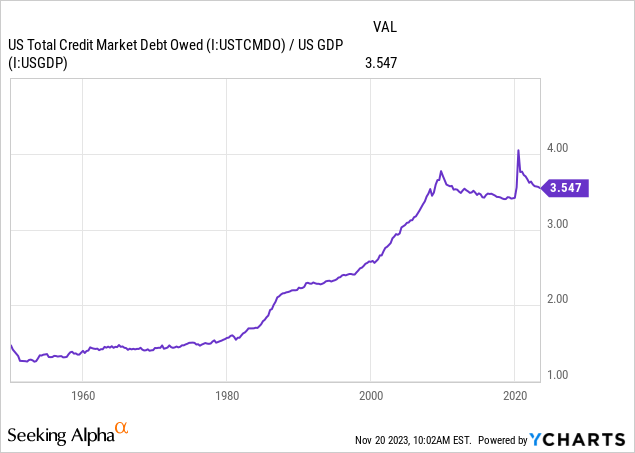

The 2007-2021 period of negative real yields is an anomaly compared to the historical record since the 1960s, with real yields typically being positive from 1980 to 2007 outside of recessionary periods. Accordingly, there is reason to believe real yields on short-term money may remain positive, given efforts to combat inflation may be chronically elevated due to excesses created during the past ~14 years. In other words, because interest rates were so low from 2007-2021 compared to inflation, total US debt growth (public and private) has been too high; thus, rates must remain elevated for an extended period to push the total debt-to-GDP back to more reasonable levels. See below:

This figure represents the US’s total public and private debt, including notable factors such as US Federal debt, mortgages, corporate debt, and all other forms of credit. In my view, this is perhaps the most important chart of all today because it represents the general expansion of US debt since the 1960s relative to income. The ratio has not changed dramatically since the 2008 recession, as the “private debt crisis” was primarily transferred to the government’s balance sheet.

It is unclear how this debt will be reduced, but abnormal inflation will naturally lessen the ratio over time, while higher interest rates will discourage debt growth. Thus, I believe even in a recession, we’re unlikely to see inflation permanently return to “Great Moderation” levels. I think inflation will likely average around 3-4%, with interest rates around 4-5% for most of the next decade. A recession may push those figures lower temporarily, but the fact is that slightly higher inflation and interest rates are the only feasible way out of the long-term debt crisis.

By that logic, SGOV may be an excellent asset to own in the short term, and the long term as cash enters a new era of market support. Of course, if endless debt expansion is allowed to continue through renewed QE or rate cuts, then inflation could rise out of control and cause SGOV to have a negative real yield. In my view, the Federal Reserve has ideally learned its lesson from its 2020 experience and highlighted the pitfalls of extreme stimulus efforts. That said, political pressures may push the US toward a potentially hyperinflationary policy in the event of a severe recession. In other words, US voters may demand extreme government stimulus spending if unemployment rises too fast, which I believe could result in 10%+ inflation, thereby creating more long-term harm than short-term benefits. The Federal Reserve may be reluctant to pursue that course because of the precedent set in 2020 due to political pressures, which, to me, had more significant long-term consequences (inflation crisis) than benefits (large recession avoidance).

Cash is King in a Recession

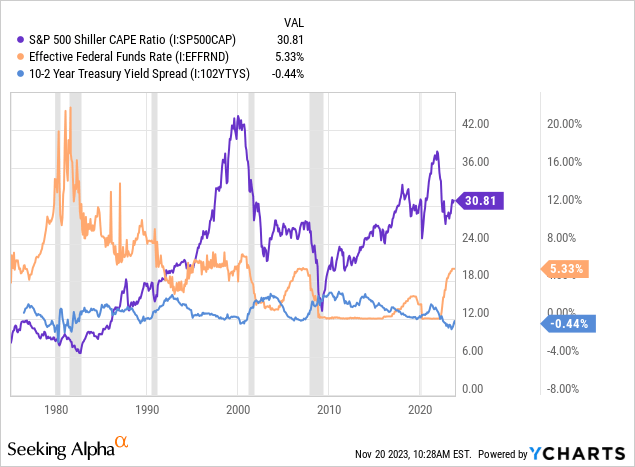

I believe SGOV is a great long-term asset because I do not think the Federal Reserve will maintain rates below inflation over the coming years. That said, even if we assume SGOV’s yield will eventually be cut dramatically, it will likely remain the best asset to own until then. SGOV will not lose value in a recession, although its yield will likely decline as the Federal Reserve reduces rates. However, stocks and other riskier assets are usually sold at “fire sale” discounts when interest rates hit a cyclical bottom. See below:

Over the long run, the S&P 500’s valuation is inversely correlated to interest rates. If the US is in a chronic stagflation period like the 1980s, when inflation was often over 10%, we could eventually see the Fed raise rates to equally high or even higher levels. In that scenario, we can expect the S&P 500’s valuation to fall dramatically, potentially leading to catastrophic losses in all cyclical assets.

That said, it is often a better time to buy stocks when short-term interest rates are low compared to long-term rates, as measured by the “10-2” yield curve. Usually, the yield curve reaches a high level just after a recession, with the curve usually returning to positive territory around the onset of a recession. This is because the yield curve peaks when investors expect an eventual rise in the Fed funds rate. Recessions are always steepening periods, while inverted curves often indicate a recession 1-2 years in advance. Peak yield curve periods, such as 1992, 2003, and 2010, were all followed by years of stable or rising S&P 500 valuations. However, high-inflation periods such as 1977-1985 and 2020 onward can complicate this relationship, adding some uncertainty to my outlook.

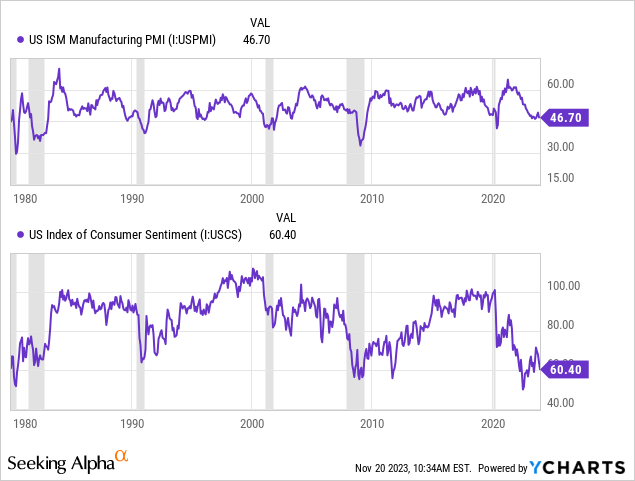

Still, even non-interest rate-driven data tends to indicate an impending recession. This includes the manufacturing PMI (survey data of business activity changes) and consumer sentiment. See below:

Both of these critical measures are very low and statistically point toward a high recession probability. That, combined with the slowly rising inverted yield curve and weakening holiday sales outlooks, corroborates my view.

The Bottom Line

SGOV, or other cash-based funds, are almost certainly the best low-risk asset to own in a recession. They will continue to pay a high yield until the Federal Reserve cuts rates, and I believe they may only cut rates by 1% due to “sticky” inflation and debt growth concerns. Further, once we see significant cuts, it may be an excellent time to move out of cash into riskier cyclical assets like junk bonds and stocks. Conversely, now that we’re looking toward a recession in which stocks and bonds are generally not discounting, I believe it is an inferior time to invest in those more cyclical assets.

Stocks, corporate bonds, and other assets that pay yields over ~6% will usually lose around 10-50%+ of their value in a recession, depending on its severity. To me, that risk, which, based on the data, I believe has a probability over 50% in 2024, far exceeds a small 1-3% spread on such assets above the Federal funds rate. Thus, I am extremely “bullish” on SGOV because it lacks financial risk and pays an excellent yield compared to other assets and even inflation. The only minor risk is a temporary default (as seen earlier this year); however, such would likely create more significant risks for other assets and would almost certainly be short-lived.

Read the full article here

Q4 2025 Earnings Call Transcript")

Q4 2025 Earnings Call Transcript")