")

Haleon plc (NYSE:HLN) is a promising company of personal care products, which means it operates within the consumer staples sector. This ties the company’s operations and health to the consumer’s economic strength. While recent macroeconomic developments raise causes for concern regarding the macroeconomic picture, HLN emerges as a potentially safe bet in the sector due to its seemingly low beta and cheap valuation. Moreover, my valuation model suggests HLN is significantly undervalued, with an upside potential of up to 44.6% and an $11.92 per share price target.

Business Overview

Haleon plc is a consumer health company based in Weybridge, England, with subsidiaries worldwide. HLN is one of the largest healthcare companies in the world, as it operates in North America, Latin America, Europe, the Middle East, and Asia Pacific. HLN was established in 2022 as a spinoff from GSK plc (GSK). HLN’s mission is to deliver better everyday health to humanity, promoting health knowledge and understanding to empower people to take better self-care.

The company works in the research, development, manufacture, and distribution of oral health, vitamins, minerals, supplements, and over-the-counter (OTC) healthcare products. OTC products are usually divided into Pain, Respiratory, Digestive, and Other. HLN’s leading brands include Sensodyne toothpaste, Panadol Advil painkillers, and Centrum vitamins.

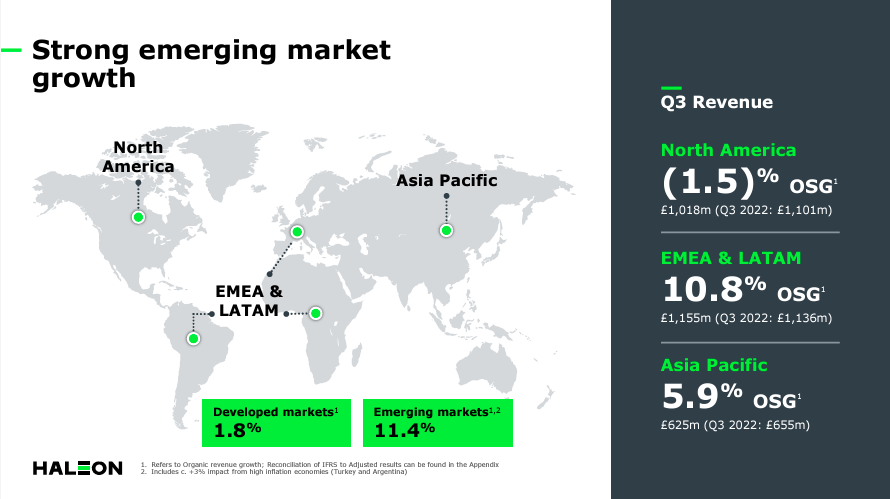

Haleon 2023 Third Quarter Trading Statement

HLN operates in a market with key multinational competitors in the consumer healthcare sector. The biggest competitors are Unilever PLC (UL), Reckitt Benckiser Group Plc (OTCPK:RBGPF), and British companies. And among American companies, the most notable competitor is likely Colgate-Palmolive Company (CL). Nevertheless, I believe the market is large enough to accommodate all, and more importantly, it’s growing at a decent pace (more on this later). So, while the market is undoubtedly competitive, it’s evident that HLN has carved its share of it, and judging by its consistent revenue growth in its segments, it’s reasonable to expect its long-term prospects to remain promising.

Haleon 2023 Third Quarter Trading Statement

In my opinion, it’s also worth noting that HLN’s ownership structure contemplates predominantly Pfizer Inc. (PFE), with a 32% holding, GSK with 7.4% after the last sale of 270 million shares, and 50% are former holders from when Haleon was part of GSK. Interestingly, this means that, for now, the sector appears to be interconnected from a shareholder point of view. This may have advantages, as it ties their interests and likely reduces competitive pressures wherever possible. Still, Pfizer had also announced plans to reduce its stake in HLN. Albert Bourla, Pfizer’s Chief Executive, said the joint venture was “not strategic” for the drugmaker.

Therefore, it seems that GSK and Pfizer consider their holdings in HLN as financial assets outside of core business areas. Thus, by divesting assets like HLN, GSK, and Pfizer, they could have more resources to focus on investing in their projects or reinforcing their balance sheets. But, such divestitures could potentially increase the competitive pressures between these companies, leading to pricing pressure and lower margins. Naturally, it’s difficult to predict the game theory of this. Still, it’s worth considering from an investment perspective because you may want to tailor your exposure to a basket of personal care product companies, not just HLN, after these strategic sales from GSK and Pfizer.

Economic Headwinds and Legal Challenges

Additionally, in September 2023, it was reported that a panel of FDA advisors agreed that the common nasal decongestant phenylephrine is ineffective when used orally. This ingredient is used in HLN’s cold remedies, Robitussin and Triaminic. These products could be pulled off store shelves nationwide as CVS (CVS) did in October. As a result, there is a risk that multiple lawsuits could be filed against the company. In fact, a class action lawsuit was already brought in New Jersey, accusing them of misleading customers about phenylephrine. As a result, HLN may have to compensate customers deemed to have been harmed. Another legal problem that HLN may have has to do with Zantac, pulled from the market at FDA request because samples of this medicine contained NDMA, considered a probable carcinogen. HLN can inherit this liability from Pfizer and GSK.

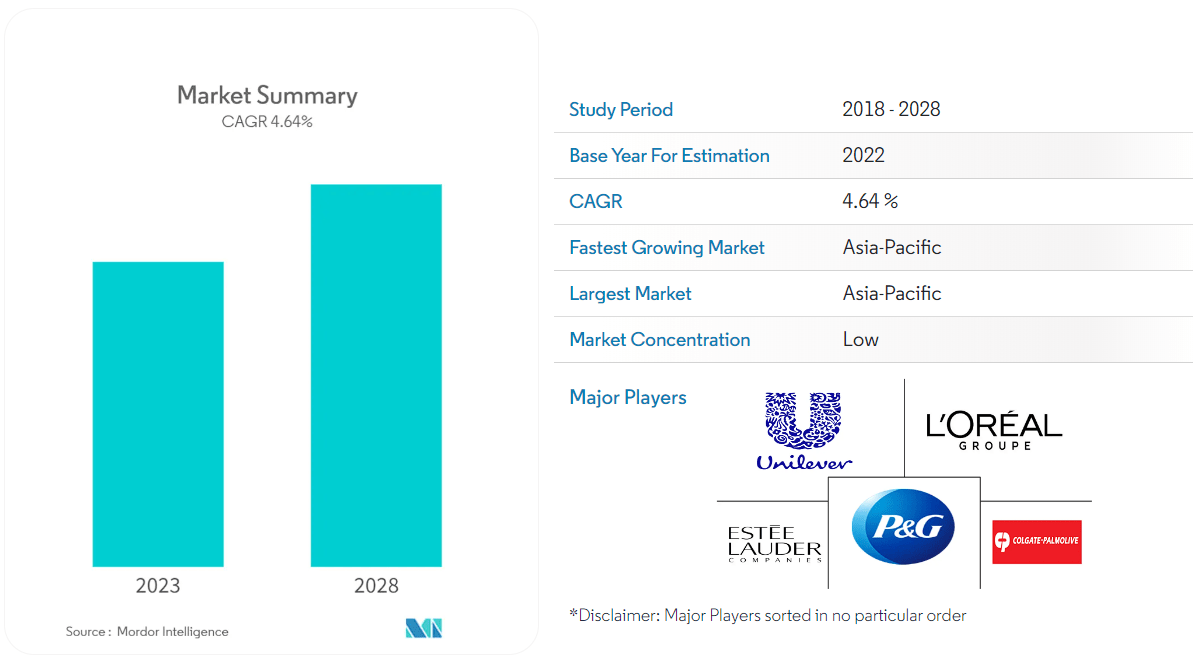

HLN’s Sector is Forecasted to Grow at a Healthy 4.64% CAGR Until 2028. (Mordor Intelligence)

Lastly, HLN’s Q3 2023 slides highlight the company’s strategies. HLN declared its focus on smaller, strategic acquisitions aligned with its overall strategy, offering compelling commercial value. HLN is not expected to announce divestments in the immediate future, but it does seek to reduce its debt to less than three times its net debt/Adjusted EBITDA during 2024. Also, in their last investor presentation, HLN particularly implied their interest in investing in Digitisation, the ordinary dividend itself, and Bold-On M&A. Thus, reducing debt and, by extension, interest payments is a value key driver for HLN in the long run.

Interestingly, the company is evidently looking for new growth alternatives and potential sources for margin improvements across its business. In particular, Digitisation could help streamline its operations related to inventory management, which is a huge business unit for consumer staples. Data-driven decision-making could benefit from such digitization processes because as they record everything, the benefits from big data and data science will come into play, likely in the form of enhanced consumer experiences and potentially even e-commerce. So, this is something that investors may underappreciate regarding HLN. Still, it appears to me they’re on the right track for improving margins consistently over time, not to mention digitization will likely help them with any supply chain management challenges if they come up again, as it happened during the COVID pandemic.

Regardless, one of HLN’s main challenges is facing a negative macroeconomic environment with high inflation that affects its costs. Naturally, this is a broad economic risk. Yet, it affects HLN specifically because it’s directly tied to how strong the consumer is, and its products are slightly more premium and the bare necessities. Thus, HLN’s product portfolio might be at a higher risk during an economic contraction, particularly if the US consumer weakens significantly. The reason for this is twofold for HLN: On the one hand, it could see a weakening demand, but on the other hand, even the supply side is challenged due to supply chain and inflation headwinds. Yet, interestingly, HLN’s low beta of 0.3 would imply it’s rather safer than the average (assuming we associate volatility with risk), which is especially puzzling due to HLN’s seemingly levered balance sheet. So it’s worth noting that the market seems to asses that HLN’s overall risk profile is on the safer side, despite its strong connection to the economic strength of the weakening US consumer and high sensitivity to it.

Valuation Analysis

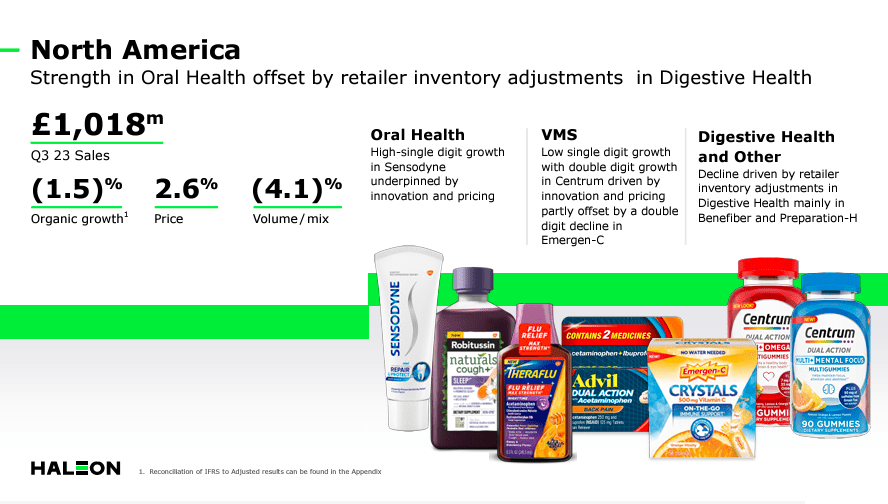

First, it was notable that the 6.6% price increment produced HLN’s 5% organic revenue growth despite a 1.6% decrease in sales volume. The Q3 2023 report also highlighted the inventory issues of digestive health products in the US that led to a slight decline in this market. Again, I think digitization and potentially M&A could improve these inventory issues, so I remain positive as these issues should clear up over time.

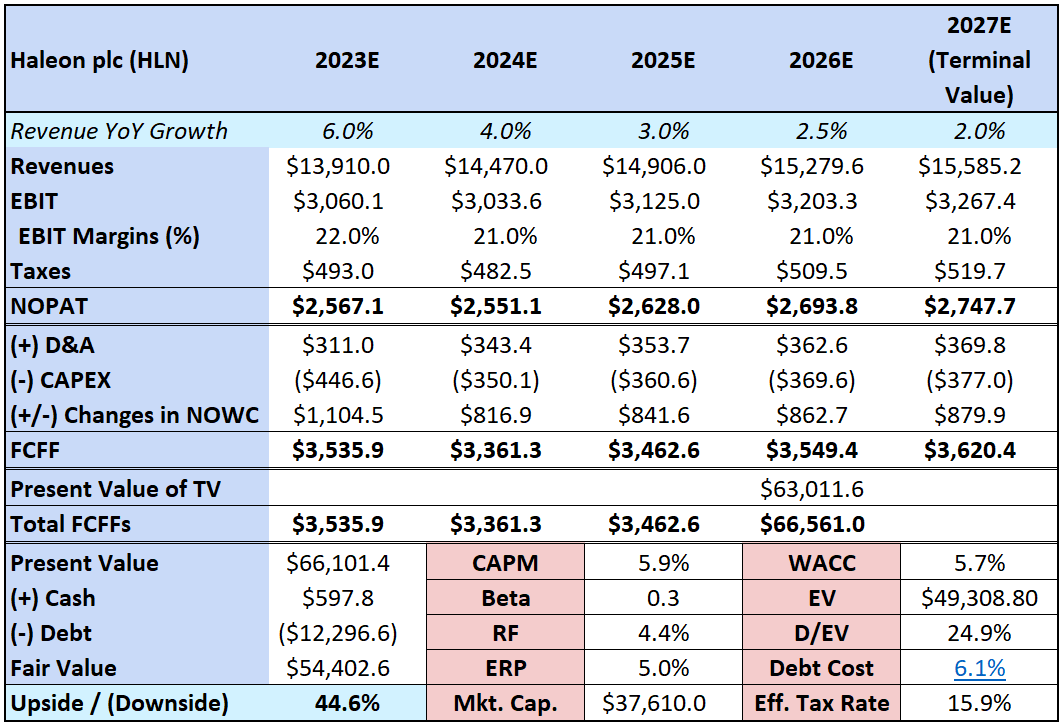

Nevertheless, from a valuation perspective, HLN can be quickly priced through a simple DCF analysis. It’s first worth noting that the company’s EBIT margins have historically been stable, around 19% to 22%. Revenue-wise, the CAGR since 2019 has been 5.3%. In particular, since HLN’s revenue CAGR has been slightly higher than its sector’s CAGR of 4.64%, it’s also implied that HLN is gaming some market share. All of these factors are promising, and when you put these dynamics together, you see a picture of steady capital compounding over time, which is generally a favorable dynamic for long-term investors.

Author’s Elaboration

Furthermore, we can use historical data to infer a run rate for the D&A, CAPEX, and NOWC margins and its effective tax rate. But for the most part, one striking feature of HLN is its relatively stable growth over time with consistent EBIT margins that have been improving slightly over the years. I’ve assumed a tapering revenue growth into 2027 for my valuation model after using the analyst estimates for 2023 and 2024 revenues. You can see the figures below.

Author’s Elaboration

As you can see, my valuation model suggests that the company is undervalued, implying a 44.6% upside potential at the current levels. Notably, most of this value comes from my model’s seemingly low CAPM and cost of debt inputs. The CAPM is low mostly due to its beta of 0.3, significantly reducing HLN’s risk profile from a valuation perspective. Likewise, I’ve used the company’s latest Moody’s credit rating and the corresponding bond yields to infer its cost of debt going forward. The picture is mostly a story of sound capital structure, stable business economics, and growing revenues with marginally improving EBIT margins. This model gives us a “buy” rating for HLN, with a price target of $11.92 per share.

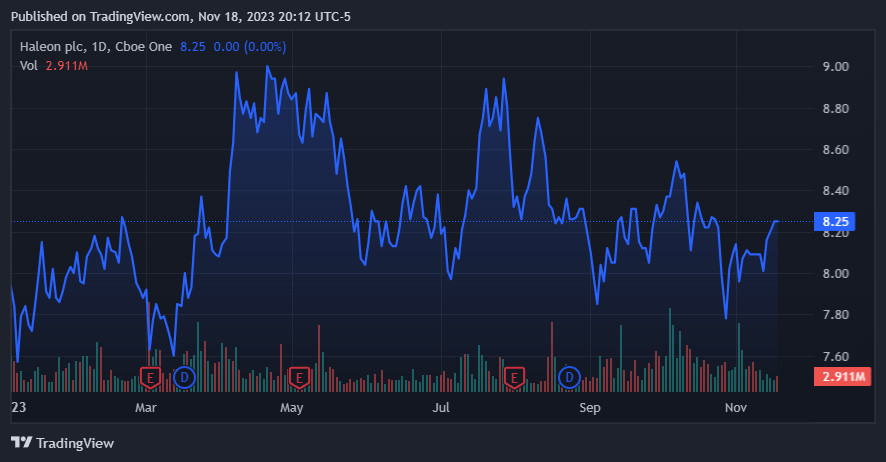

HLN has been Treading Water Since 2023, but its Intrinsic Value has Grown. The current levels seem like a good entry price for new investors. (TradingView)

Investment Thesis Risks

Haleon, as a company in the consumer healthcare market, faces risks inherent to this sector. HLN is subject to strict regulatory requirements that can change or be difficult to comply with. Additionally, the company can face legal lawsuits and financial liabilities for the product’s adverse effects or misleading claims, as it is the issue with the nasal decongestant phenylephrine that the FDA ruled as not effective when used in oral form. Also, disruptions in the supply chain may produce inventory problems and lead to lost revenue, as was the case of the digestive health products in the US in the last quarter. Lastly, the consumer healthcare industry is very competitive. Therefore, HLN must invest heavily in R&D to keep its market share.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")