")

Much of the reporting on the health of real estate comes from the lens of transactions. Sentiment on real estate is often related to volume of transactions rather than operations. Presently, transaction volume is very low which is resulting in equally low sentiment on real estate.

I want to make a distinction between real estate transactions and real estate ownership.

The 2 categories are different entities and have different drivers yet because they are lumped together in the way they are reported it forms an overall sentiment on real estate. We will discuss this concept in greater detail below, but the crux of the thesis is this:

Low sentiment from transactional weakness is overshadowing ownership strength

This concept can be illustrated with a look at the housing market.

Here is the title of a report from GeekWire.

geekwire

If one is not considering the distinction between transactions and ownership, this might appear like housing is weak. Terms like “slumping real estate market” actively conflate the two.

Reading the report, the data it is referencing is about transactions specifically.

“Redfin and Zillow Group‘s second-quarter earnings reports point to more pain in the real estate market as limited housing supply and climbing mortgage rates throttle transaction volume.”

Redfin (RDFN) and Zillow (Z) make their money through transaction volume.

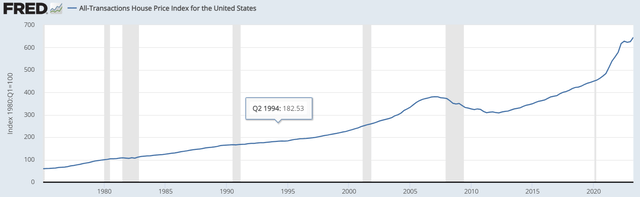

Ownership, however, is having a great time. Housing prices are at an all-time high.

FRED

It has been a great time to own a house. Homeowners experienced massive appreciation. A homeowner does not care about transaction activity. They get to live in their house and now have more home equity than ever before.

Very low sentiment on real estate coming from transactional bias in reporting

A large portion of those who work in real estate derive their income from transactional volume.

- Realtors

- Brokers

- Banks

- Underwriters.

These are the people who are often brought on to news programs as real estate (“RE”) experts to discuss the health of real estate. They have had a fairly gloomy tone as of late, and I can’t blame them because their core business is transactions, which are terrible.

GlobeSt.com reports that:

globestreet

RE transactions have fallen off a cliff because there is a mismatch between buyers and sellers. Cap rates have remained low because property operating income is expected to increase. Nobody wants to sell at an 8% cap rate if they think NOI is going to rise by 20%. So, they bake that growth into the cap rate and only want to sell at 6.5% or lower.

At the same time, buyers are dealing with expensive capital which makes cap rates below 8% not feasible in the near term.

Thus, people just don’t transact unless they have to.

Since so much of real estate reporting comes from the perspective of those who care about transactional activity, sentiment for real estate has fallen along with transactions. This sentiment gets reflected in stock prices.

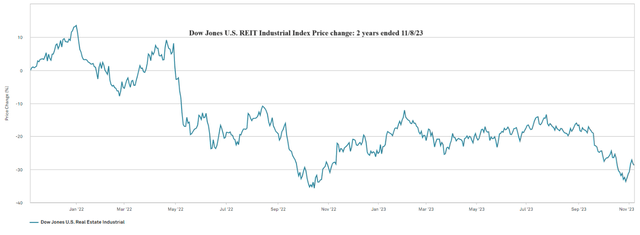

For example, we can look at the industrial real estate investment trust, or REIT, sector down nearly 30% in the last 2 years.

S&P Global Market Intelligence

It so happens that this corresponds to the transaction volumes of industrial. Another GlobeSt.com report shows that Industrial transactions were down 24% year over year as of March 2023. Industrial transactions continued dropping with the June GlobeSt.com report (linked earlier) showing volume down 69% year-over-year.

It is worth noting that this transactional activity is in this instance the polar opposite of what property owners experienced.

NOI is straight up for just about the entire industrial REIT sector. New leases are being signed anywhere from 25% to 100% above expiring leases.

THAT is what owners are experiencing.

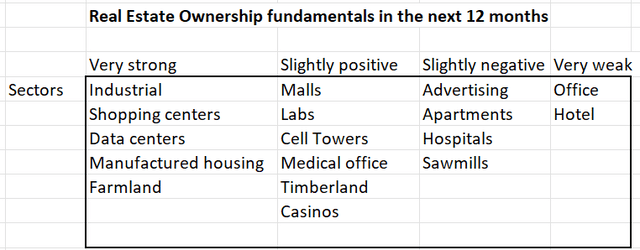

Varies by sector

While transactional activity is down across basically every real estate sector, owners are experiencing the full spectrum of results. Here is a quick and dirty table of the near-term fundamental strength of the various property sectors.

2MC

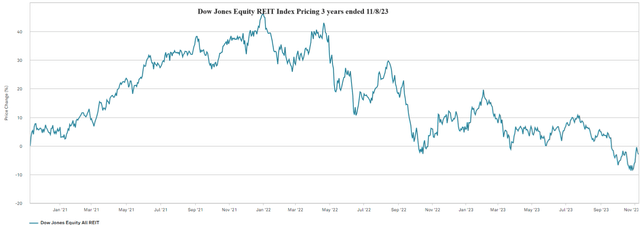

The distinction between transactions and ownership is a source of opportunity right now. The entire REIT market has fallen due to the low sentiment caused by the low transaction volume. Transactions peaked roughly at the end of 2021. So did REIT stock prices.

S&P Global Market Intelligence

The crash has been undiscerning. Bad REITs fell hard. Good REITs fell hard.

The opportunity

Since so much of the price correction seems to be related to transactional volume as opposed to fundamental strength, there are many opportunities to pick up strong REITs at the now reduced prices.

Equity REITs are overwhelmingly property owners as opposed to transactors. Buying or selling properties is merely an arrow in their quivers. It is the fundamental value of the properties that makes or breaks returns.

Here are the key ingredients of what makes an opportunistic REIT right now.

- Net Operating Income – up

- Stock price – down

- Forward AFFO/share growth

- Low AFFO (adjusted funds from operations) multiple.

You might be surprised how many REITs fit this description. Happy Hunting!

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")