")

")

The last time I doubled down on Upstart Holdings, Inc. (NASDAQ:UPST) was in August of this year. I doubled down on the fintech primarily because the earnings multiple compressed greatly after Upstart Holdings reported 2Q-23 earnings.

With Upstart Holding’s stock experiencing yet another crash after 3Q-23 results were released, I have grabbed more shares out of the bargain bin, but this time because the market has received convincing evidence that the rate-hiking cycle is set to come to an end in 2024.

The fintech’s 3Q-23 earnings were under the impression of interest rate headwinds which caused a larger-than-expected loss and impacted the personal loan business negatively. However, with inflation coming down substantially in October, I think investors have gotten the clearest sign yet that interest rates have indeed peaked.

Thus, I think the central bank is poised to slash the key interest rate next year which would be favorable to Upstart Holdings.

Upstart’s 3Q-23 Results Disappointed (But This Shouldn’t Have Been A Surprise)

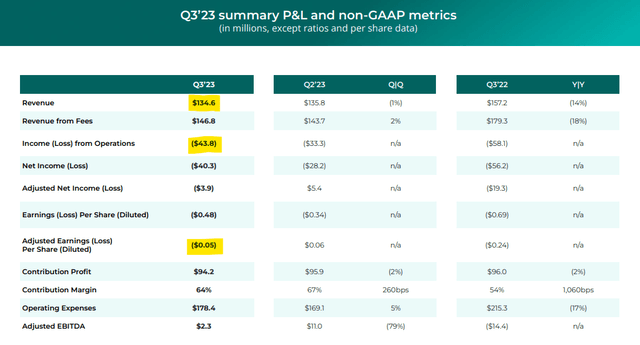

Upstart Holdings’ third quarter earnings yielded a larger-than-expected loss (a loss of $0.02 per share was expected compared to a realized loss of $0.05) which caused the fintech’s stock price to crash (again).

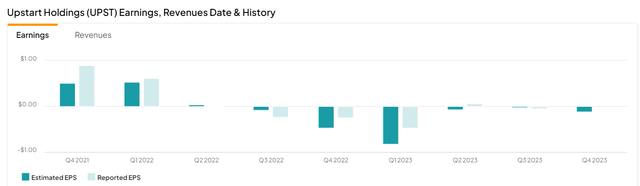

Earnings And Revenue (Upstart Holdings)

Upstart Holdings’ third quarter earnings fell due to muted demand for new loans, in either the personal loan or auto loan origination segment.

Upstart Holdings’ sales declined 14% YoY to $134.6 million while earnings-measures such operating income, net income and income per share were all soundly negative. These losses should have been expected since the fintech didn’t see any change in the macro landscape in the third quarter.

This, however, is going to change as the market just digested its latest inflation report which should work to the benefit of Upstart Holdings’ originations.

Q3-23 Summary Profit And Loss Metrics (Upstart Holdings)

Why I Am Even More Bullish Than Before: Positive Inflation Trend Is A Game Changer

Upstart Holdings is essentially an interest rate play. Loan demand and originations go up when credit is cheap and demand shrinks when credit gets more expensive. As such, Upstart Holdings is a directional bet on interest rates and as soon as the market gets a hunch that interest rates are coming down, the fintech could see changing market forces drastically improve its profit trajectory.

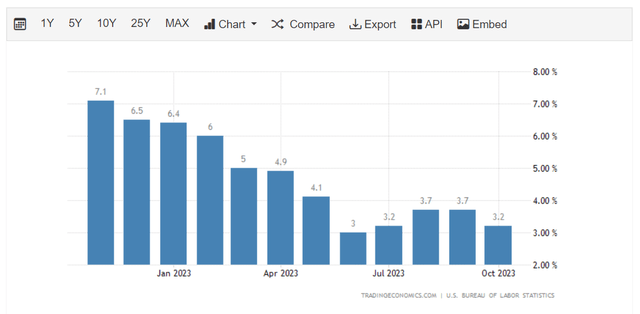

Investors can see that the winds in the industry are soon going to blow from another direction by looking at the inflation numbers for October. Last month, inflation edged up only 3.2% YoY, a rather substantial decline compared to the 3.7% inflation rate in September and the first such decline since June 2023. The cooling of inflation strongly tilts the odds in favor of rate decreases in 2024 which in turn should be a boon for Upstart Holdings’ loan originations.

Interest Rates (Tradingeconomics.com)

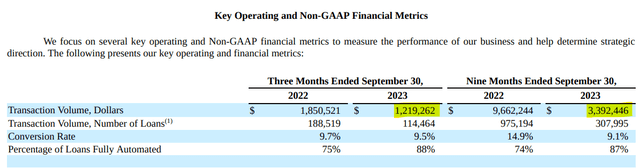

Upstart Holdings’ transaction volumes collapsed in the last year, driven by a decline in originated loans. Due to high interest rates, the fintech’s transaction volume fell 34% YoY in 3Q-23 and 65% YoY in 9M-23. However, with inflation easing, a rate cut is on the horizon and with it a potentially reinvigorated loan business.

Transaction Volumes (Upstart Holdings)

Profitability Is Just Around The Corner

Even though Upstart Holdings’ 3Q-23 earnings got a lot of attention because of the earnings miss and the large sales decline YoY, the fintech is expected to turn a profit next year. This assumption seems to be largely driven by expectations about cyclically-contracting key interest rates next year.

While I agree with such expectations, I think that Upstart Holdings could potentially turn a much bigger profit than the consensus estimate presently indicates, depending on how fast interest rates come down in 2024.

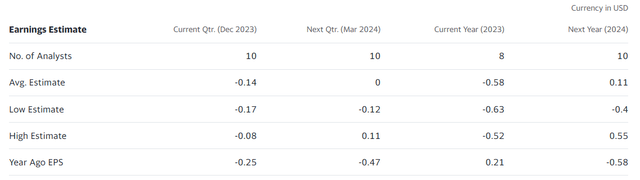

The market presently models a loss of $0.58 per share this year, but the profit situation is poised to improve next year, again, on the assumption that interest rates are coming down. For 2024, the market models $0.11 in profits which would represent a rather drastic swing from one year to the next.

Right now, Upstart Holdings is not profitable, but with inflation trending in the right direction, investor sentiment towards rate-sensitive fintechs like this one here is set to change drastically as well.

Earnings Estimate (Yahoo Finance)

Presently, Upstart Holdings’ stock is selling at a 3.9x sales multiple (based on this year’s sales) while a fintech like PayPal Holdings Inc. (PYPL) is selling at a 2.2x multiple.

Upstart Holdings’ has one major advantage over PayPal which is the possibility of an upswing in loan demand which would benefit the fintech enormously. As such, the market models 26% sales growth for Upstart Holdings in 2024 and only 8% for PayPal.

Why Upstart Holdings May Out-Or Under-Perform

Upstart Holdings is, as I asserted, an interest rate play. Loan demand booms during low-interest rate periods and crashed during high-interest rate periods.

If we saw a new phase of inflation rate acceleration, the central bank would once again have a strong case for additional rate hikes, but this seems increasingly unlikely. The ability to turn a profit would go a long way in helping the fintech achieve stock price gains.

My Conclusion

I am buying more stock when Upstart Holdings crashes, not less, and I am most definitely not selling. The fintech is well-positioned in the market with its artificial intelligence lending platform and though the current sales and profit situation does not look too great, I think that Upstart Holdings should be seen primarily as a directional bet on interest rates.

Lower inflation (and a drop in interest rates) could be a catalyst for the fintech to crush profit expectations next year. The most recent inflation report was really important in this regard, in my view, as it showed that the central bank is no longer under pressure to hike rates.

With rates coming down, I would expect Upstart Holdings to do a whole lot better than it did in the third quarter. With profits also on the horizon (in 2024), I think that UPST is still a buy.

Read the full article here

")

Q4 2025 Earnings Call Transcript")

")

")

")