")

The Western Asset Diversified Income Fund (NYSE:WDI) is a closed-end fund, or CEF, that specializes in providing a high level of income for its shareholders. The fund certainly does a reasonable job of this task, as its 12.56% current yield is certainly competitive with most other fixed-income funds. In today’s environment, fixed-income closed-end funds tend to have the highest yields available in the market. That is only natural considering how high fixed-income yields are right now.

As regular readers may remember, we last discussed the Western Asset Diversified Income Fund back in February of this year. The fund has delivered a reasonable performance since that time, as it compares rather favorably to other investments and indices. The previous article was published on February 8, 2023. An investor who purchased the fund on that date has realized a 3.43% total return. This is relatively in line with the total return of the SPDR Bloomberg High Yield Bond ETF (JNK) and is much better than the iShares Core U.S. Aggregate Bond ETF (AGG) over the period:

Seeking Alpha

Thus, the fund’s performance seems to compare pretty well with a few of the major fixed-income indices, although this fund’s holdings do not perfectly match either of these indices. This is because the fund invests in a variety of debt securities other than traditional investment-grade or junk bonds. That could be good from a diversification perspective, as some types of debt securities perform very well in a rising interest rate environment. We will discuss this in greater detail later in this article.

The market has recently been anticipating that the Federal Reserve will rapidly cut interest rates, and this belief has proven to be quite positive for the fund’s shares over the past few weeks. However, this scenario seems rather unlikely to occur to the degree that the market expects. Thus, the recent run-up may be unfounded. With that said though, this fund is better positioned than many other bond funds to withstand the market’s disappointment when its expectations appear dashed again. As such, it might make sense to consider this fund on any share price pullback.

About The Fund

According to the fund’s website, the Western Asset Diversified Income Fund has the primary objective of providing its investors with a high level of current income and capital appreciation. The provision of current income makes a lot of sense for a debt fund, as debt securities are by their very nature income securities. As I pointed out in my previous article on this fund:

These securities are generally purchased by those who are seeking income as their potential for capital gains is quite limited. The reason for this is that these securities have no link to the growth and prosperity of the underlying company. After all, a company will not increase the amount that it pays to its creditors just because its profits go up. As such, bonds and fixed-income securities deliver essentially all of their returns through direct payments to their investors.

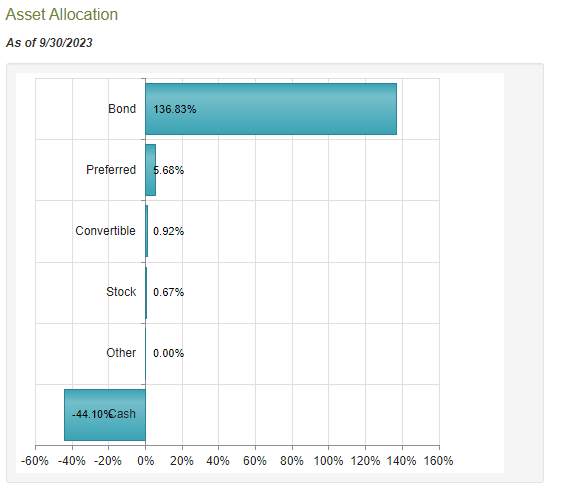

According to CEF Connect, 136.83% of the fund’s net assets are invested in bonds and 5.68% of the fund’s net assets are invested in preferred stock. The remainder of the portfolio is invested in a variety of things in very small proportions:

CEF Connect

The first thing that most readers will immediately notice is that the bond and preferred stock positions combined add up to considerably more than 100% of the fund’s total assets. This is possible because this fund employs leverage as a method of boosting its effective portfolio yield. We will discuss this later in this article. For now, the most important thing to realize is that this is a fixed-income fund.

However, not all of the assets that CEF Connect considers bonds are the ordinary fixed-coupon bonds that most of us picture. The fund’s website states that this fund:

Invests in a wide range of fixed income securities, seeking to go beyond traditional bond benchmarks to access a broad range of opportunities for income and capital appreciation.

That is something that could prove advantageous to the fund in the current market environment. After all, as most people who are reading this are certainly well aware, the traditional bond market has been crushed by the rapid increase of interest rates. Since the start of 2022, the Bloomberg U.S. Aggregate Bond Index has delivered a negative 11.57% total return, and the Bloomberg High Yield Very Liquid Index has delivered a negative 5.55% total return:

Seeking Alpha

The biggest reason for the strength of the junk bonds’ total return compared to the aggregate bond index is that these securities have a much higher yield, which helps to offset some of the price declines.

Not all debt securities have performed so poorly, however. The iShares Floating Rate Bond ETF (FLOT), which tracks the BBG Floating Rate Notes 5 Yrs. And Less Index has actually delivered its investors a 7.10% total return over the period. This is because that index contains floating-rate debt securities, which do not usually change very much with interest rates. This is because their floating coupons ensure that the bond always delivers a competitive yield with respect to the market interest rate. I explained this in a previous article.

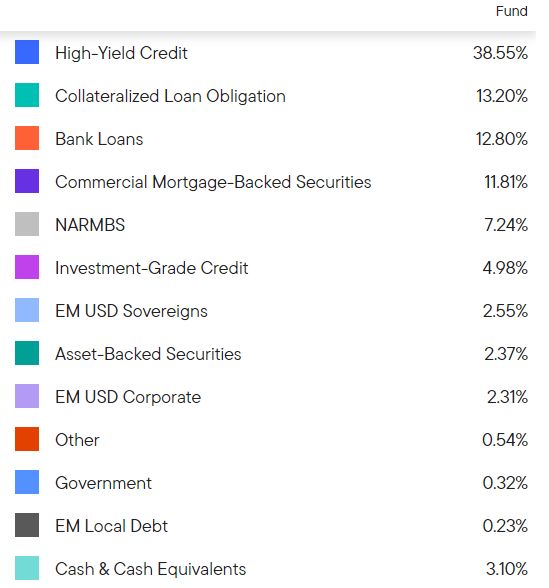

The Western Asset Diversified Income Fund invests in a portfolio of assets that consists of both traditional bonds and floating-rate securities. Unfortunately, the fund does not state what proportion of its assets are invested in floating-rate securities compared to traditional bonds. It does say on the webpage that 32.16% of the fund’s assets are invested in loans. Loans are usually floating-rate securities as opposed to bonds, which are fixed-rate. The website also includes this breakdown of the fund’s assets by type:

Franklin Templeton

Collateralized loan obligations and bank loans are usually floating rate securities. Those two positions together only account for 26.00% of the fund’s assets though, so there must be some other things in the portfolio that have floating coupons in order for the fund’s own statement that 32.16% are loans in order for that statement to be correct. Then again, perhaps some of its loans are actually fixed-rate loans. The fact sheet, for its part, does not state anything about a fixed-rate versus a floating-rate proportion across the portfolio.

Thus, a reasonable assumption is that somewhere between 25% and a third of the assets in this fund’s portfolio are floating-rate debt securities. The remainder of the fund’s debt assets would therefore be fixed-rate securities. However, we do not know this for certain.

That would be a much lower allocation to floating-rate securities than a fund such as the Apollo Tactical Income Fund (AIF) or the Ares Dynamic Credit Allocation Fund (ARDC). The Apollo fund currently has 76.7% of its assets invested in floating-rate loans and the Ares fund has 31.5% of its assets in bank loans along with a 30.8% allocation to a combination of collateralized loan obligation debt and equity. As such, both of these comparable funds have a much higher allocation to floating-rate debt than the Western Asset Diversified Income Fund.

As such, either the Apollo or the Ares funds would be better holdings than the Western Asset Diversified Income Fund if you expect that interest rates will continue to rise from their current levels. However, the Western Asset Diversified Income Fund appears to be a better choice if interest rates decline. This comes from the fact that traditional fixed-rate bonds outperform floating-rate debt when interest rates go down.

Direction Of Interest Rates

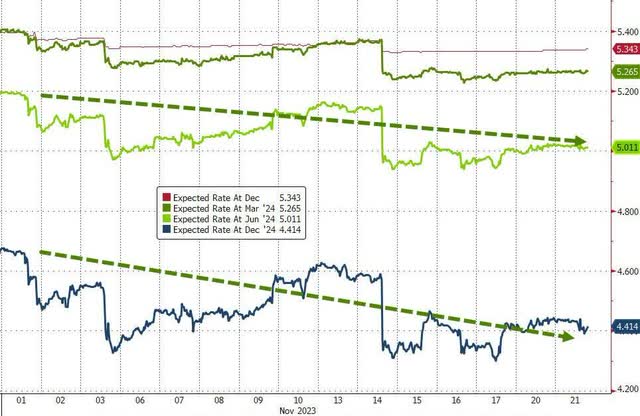

As I pointed out in a few previous articles, the market is currently expecting that the Federal Reserve will very shortly start to cut interest rates. As of right now, the fed funds futures market is pricing for a 4.414% federal funds rate at the end of 2024:

Zero Hedge

The stock market and bond market are similarly priced. This is the reason why the share price of the Western Asset Diversified Income Fund is up 6.11% since the start of this month.

As such, we can assume that the market will punish anyone purchasing the fund’s shares right now if this scenario does not play out. There are reasons to believe that rates will not drop as quickly as the market is predicting.

One major reason for this is that the minutes from the Federal Open Market Committee meeting, which were released earlier today show that the members of the committee do not believe that inflation is sufficiently beaten to justify a rate cut. From the minutes:

The staff continued to view the uncertainty around the baseline projection as considerable. Risks around the inflation forecast were seen as skewed to the upside, given the possibility that inflation could prove to be more persistent than expected or that further adverse shocks to supply conditions might occur.

Should these upside inflation risks materialize, the response of monetary policy could, if coupled with an adverse reaction in financial markets, tilt the risks around the forecast for economic activity to the downside.

All officials who were present at the meeting unanimously agreed that right now is not an appropriate time to cut interest rates.

Bloomberg’s macro strategist, Simon White, states that the Federal Reserve will need to see strong signs of a recession in the very short term to cut rates to anywhere near the degree that the market is currently anticipating. Please note that “very short term” means within the next three to six months. Furthermore, Peter Schiff states in his most recent podcast that such a recession is almost certainly going to be worse than any recession that has been seen in the United States since the Great Depression. From Peter Schiff:

Peter said it’s difficult to understand why people think the Fed can raise rates from 0% to over 5% and get away without plunging the economy into a recession.

“Why would that be if you look at the recent experiences with the Fed having rates too low and then raising them? Go back to the late 1990s and the decline we had in the economy, the recession, the stock market in 2000-2001. Look at the experience in 2008. And look at what happened even before COVID in 2018 when the Fed tried to raise rates from a low level and abort it very quickly when the wheels started falling off the bus in the fourth quarter of that year.”

History makes it clear that the Federal Reserve has a hard time normalizing rates. In fact, the attempt to bring rates from 1% to around 5% in 2007 led to the greatest recession since the Great Depression.

“So why would anyone believe that the Fed can normalize rates now and not have a similar consequence? Because, after all, the rate hikes expose all of the malinvestments and the misallocation of resources that take place when rates are artificially low.”

While many readers might perceive Peter Schiff as being something of a doomsayer and a permabear, he does make a very good point. It is hard to believe that the Federal Reserve could raise rates from 0% to 5.5% without breaking something in the economy. After all, the last time that this happened, we ended up with the Great Financial Crisis and the worst recession in modern history. In this case, the increase in rates was much larger than in 2007 and 2008 and rates were kept at artificially low levels for a lot more than just a few years.

On the positive side, the market may certainly get the rate cuts that it expects if we do get such a terrible recession. That is basically what Mr. White directly states. It also seems to be the goal of the Federal Reserve, as the most recent committee meeting’s minutes seem to suggest that economic data is far too strong to justify rate cuts.

As such, it may not make sense to purchase shares of the Western Asset Diversified Income Fund unless you expect that a massive recession will occur in the short term. If the Federal Reserve does not cut rates by around 100 basis points next year, the shares of the fund are likely to get punished at least to the degree that the shares benefited from the run-up so far this month. Those rate cuts seem unlikely to occur unless a severe recession occurs, and in the event of a recession, the shares of the fund might still get sold off as investors panic sell and go to cash.

Leverage

As stated earlier in this article, the Western Asset Diversified Income Fund employs leverage as a means of boosting the effective yield of its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to buy bonds and preferred stock. As long as the purchased assets carry a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. As the fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage above a third as a percentage of its assets for this reason.

As of the time of writing, the Western Asset Diversified Income Fund has leveraged assets comprising 32.94% of its portfolio. This is only slightly higher than the 32.77% leverage that the fund had the last time that we discussed it. This is quite reasonable, as it is lower than most other fixed-income funds and it is below the one-third level that I would ordinarily consider to represent a decent balance between the risk and the reward. Overall, we probably do not need to worry about the fund’s leverage too much, but we also should watch it to make sure that it does not keep climbing.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Western Asset Diversified Income Fund is to provide its investors with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio consisting of various forms of debt securities that are designed to allow the fund to maximize its returns based on the expected direction of interest rates or the broader economy. These securities deliver the majority of their total returns in the form of direct payments to their investors, or in this case to the fund. The fund collects all of the money that it receives from these securities and even applies a layer of leverage to control and collect income from even more debt securities than it could by relying solely on its own net assets. The fund then pays out all of the money that it collects from these activities to its shareholders, net of any of its own expenses. As the fact sheet states that the average coupon of the securities in its portfolio is 12.15%, we can expect that the fund will be able to pay out a remarkably high distribution yield to its own investors.

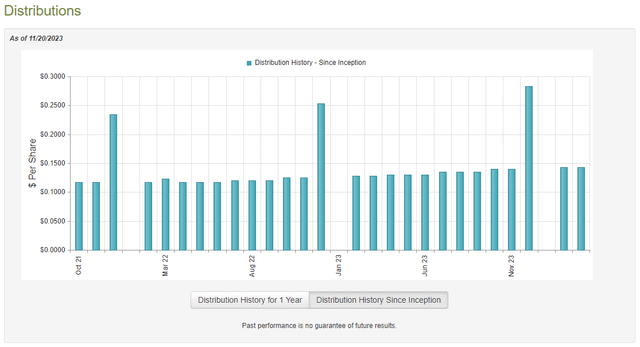

That is certainly the case, as the fund currently pays a monthly distribution of $0.1430 per share ($1.716 per share annually), which gives it an attractive 12.56% distribution yield at the current price. This fund’s distribution has varied a bit over its lifetime, but for the most part, it has been somewhat more reliable than many other debt funds:

CEF Connect

As we can see above, the Western Asset Diversified Income Fund is one of the few debt-focused closed-end funds that has managed to increase its distributions over the past year. This is probably due to the influence of the floating-rate securities that are found in the fund’s portfolio, as both the Apollo and the Ares closed-end funds that were mentioned earlier in this article have managed to accomplish the same feat. This is something that will undoubtedly be attractive to investors for two reasons. The first of these is that the rising distribution helps to offset some of the financial pain that we have all been feeling in today’s inflationary climate. After all, the fact that the fund is paying us more money helps to ensure that we can buy roughly the same things that we could too years ago. The growing distribution also gives us some confidence that the fund probably can afford its distribution, which has been a problem for most fixed-income funds over the past two years.

It is not necessarily the case that a rising distribution means that the payout is sustainable. There have been cases where a fund raised its distribution in an attempt to get investors to bid up the shares, after all. As such, we should still have a look at the fund’s financial statements in order to determine how sustainable its distribution payout is likely to be.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is obviously a much more recent report than the one that we had available to us the last time that we discussed this fund. This is good because the first half of this year was characterized by a considerable amount of optimism and even euphoria in the market, as investors widely believed that the Federal Reserve would shortly begin to cut interest rates. Investors bid up both stocks and fixed-income securities in anticipation of that event. While the market was obviously wrong, it may have provided this fund with an opportunity to sell appreciated bonds in a wildly optimistic market and generate some capital gains in the process. This report will give us a good idea of how successful the fund was at this task.

During the six-month period, the Western Asset Diversified Income Fund received $61,308,355 in interest and $852,153 in dividends from the securities in its portfolio. We subtract the fund’s withholding taxes that it had to pay to foreign governments in order to get a total investment income of $62,149,248 during the period. The fund paid its expenses out of this amount, which gives it a net investment income of $44,400,551 over the course of six months. That was actually more than enough to cover the $40,446,592 that the fund paid out in distributions with money left over that could be used for other purposes.

For the most part, everything looks fine here. For the full-year 2022 period, the fund’s net investment income was also higher than its distributions. It therefore appears that this fund is simply paying out its net investment income right now, which is exactly what we want to see. The fund’s distribution should be reasonably safe as long as the fund can keep its net investment income at the current level. That will probably be the case for as long as interest rates stay at today’s levels.

Valuation

As of November 20, 2023 (the most recent date for which data is available), the Western Asset Diversified Income Fund has a net asset value of $14.87 per share but the shares currently trade for $13.24 each. This gives the fund’s shares a 10.96% discount on net asset value at the current price. That is a very reasonable discount, although it is far less attractive than the 13.39% discount that the shares have had on average over the past year. As such, it might make sense to wait for the market to offer a more attractive entry point, but realistically a double-digit discount like we have today is generally a reasonable price to pay for any fund.

Conclusion

In conclusion, most things about the Western Asset Diversified Income Fund look pretty good. This is one of the few debt funds that is actually covering its distribution fully and consistently while still boasting a remarkably high yield and an attractive valuation.

My only concern here has nothing to do with this fund. The market has bid up Western Asset Diversified Income Fund shares substantially in the hopes that the Federal Reserve will rapidly cut interest rates next year. That seems to be very unlikely unless a severe recession occurs within the next three months. If the Federal Reserve does not cut interest rates rapidly, shares of the fund will probably be sold off and cause pain for anyone who purchases shares of the fund today. The fund itself looks great, but it may not be the best idea to buy it today because of that risk.

Read the full article here

Q4 2025 Earnings Call Transcript")

Q4 2025 Earnings Call Transcript")